Investment Ideas

The table below lists our Investment Ideas as well as our Watch List – a list of potential ideas that we are in the process of evaluating. We intend to update this table regularly and will provide detail on any material changes.

Recent Notes

06/09/14 Monday Mashup: DFRG, CAKE, PNRA

06/09/14 MCD: Time For A Change

06/12/14 New Best Idea: Short DFRG (Replay)

06/13/14 BOBE: Reiterating Best Idea Long

Events This Week

06/17/14 KKD Annual General Meeting

06/17/14 Deutsche Bank Global Consumer Conference: BAGL

06/17/14 Jefferies Global Consumer Conference: CHUY

06/17/14 BOBE earnings release 4:00pm EST

06/18/14 Jefferies Global Consumer Conference: BBRG, DNKN, FRGI, FRSH, JACK, NDLS, RUTH, ZOES

06/18/14 BOBE earnings call 10:00am EST

06/20/14 DRI earnings release BMO, earnings call 8:30am EST

Chart of the Day

Recent News Flow

Monday, June 9th

- EAT Chili’s announced the completion of its nationwide rollout of tabletop tablets in the U.S., which included the installation of 45,000+ Ziosk tablets in 823 company-owned restaurants.

Tuesday, June 10th

- DPZ initiated buy at Jefferies with an $85 PT.

- BJRI officially launched a mobile ordering/payment app for its restaurants. The new app allows customers to use their mobile devices to order ahead for dine-in and takeout, move ahead in line for a table and pay at their own convenience.

- WEN was downgraded to hold from buy at Argus Research based on “uncertainty” around the company’s remodeling initiatives.

- GMCR announced an initiative to expand its presence at SUBWAY, by bringing Keurig single serve brewers to thousands of restaurants.

- DNKN announced the locations of its first traditional restaurants in CA. They are currently planned for Downey, Long Beach, Modesto, Santa Monica and Whittier. Construction is planned to begin later in June, earlier than expected.

- PZZA Papa John’s announced the appointment of former AIG Executive Chairman, Laurette Koellner, to its Board of Directors.

Wednesday, June 11th

- No major news.

Thursday, June 12th

- PNRA closed on a $100 million term loan from BoA, Wells Fargo and TD Bank. Proceeds from the loan will primarily be used for general corporate purposes.

Friday, June 13th

- No major news.

Sector Performance

The XLY (-1.7%) underperformed the SPX (-0.7%) last week. Casual dining stocks underperformed the narrower XLY index, while quick service stocks outperformed.

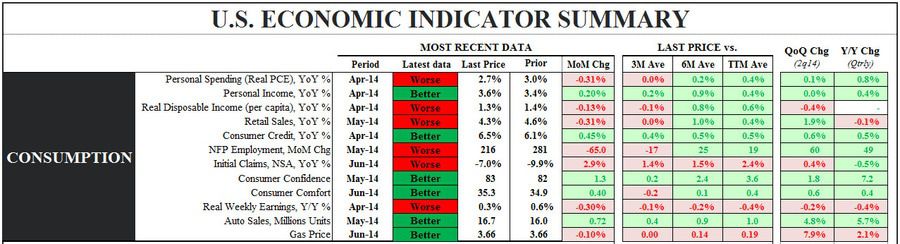

U.S. Macro Consumption

The Hedgeye U.S. Consumption Model continues to signal bearish, flashing red on 7 out of 12 metrics.

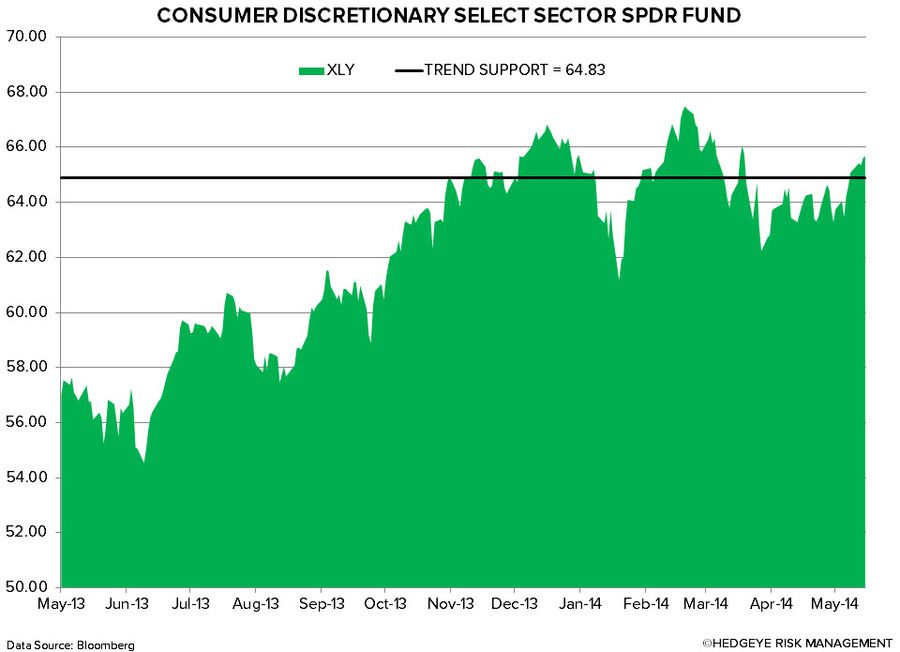

XLY Quantitative Setup

From a quantitative perspective, the sector remains bullish on an intermediate-term TREND duration.

Casual Dining Restaurants

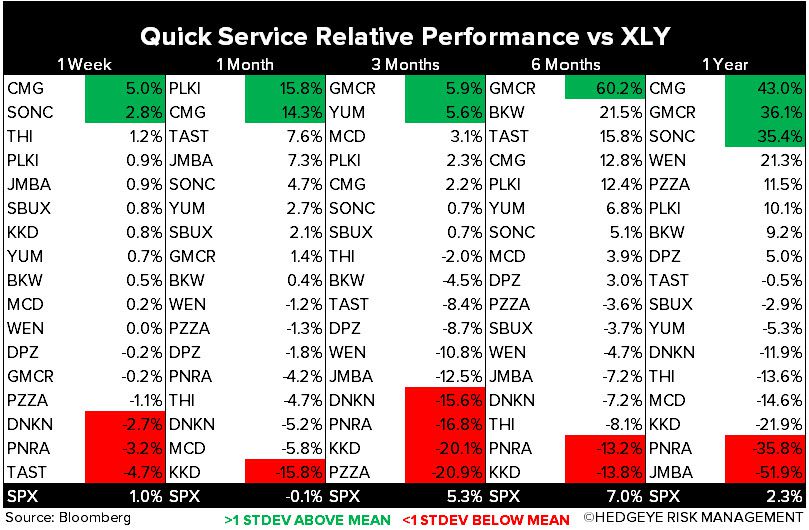

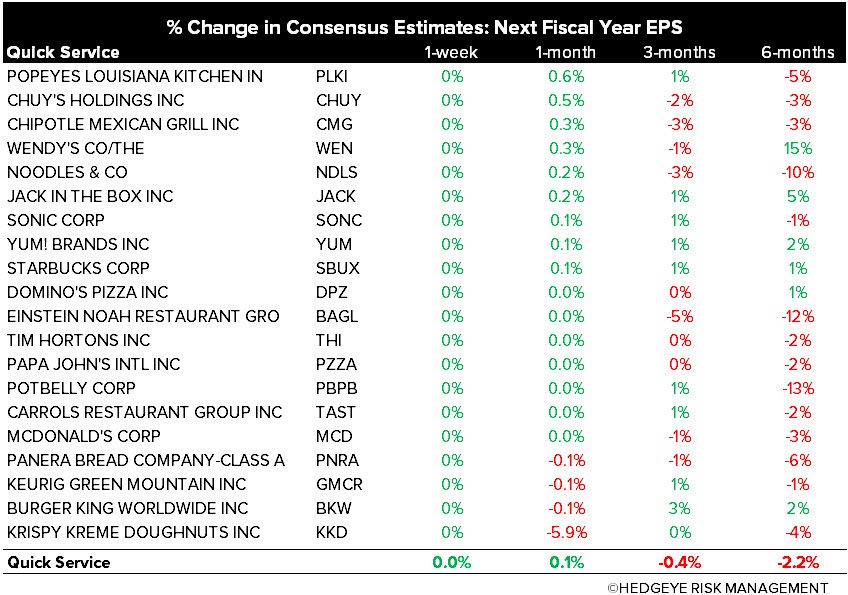

Quick Service Restaurants

Howard Penney

Managing Director

Fred Masotta

Analyst