The consensus sell-side call: buy the stocks of the Macau gaming operators on weakness due to strong mass growth. What happens when mass decelerates?

CALL TO ACTION

While the sell-side has caught up to the VIP slowing thesis, the analysts remain mostly positive on the Macau gaming stocks due to “continued strength in the mass segment”. Well friends, we again send up the warning flare – this time we call attention to the imminent deceleration in the mass segment. It’s mostly the math and the lapping of a significant rise in table minimums but also, VIP and mass revenue have historically shared a correlation coefficient of 0.56. Moreover, if recent reports are correct, premium mass may be susceptible to the upcoming smoking ban (VIP rooms will be exempt). While certainly a contrarian call, could the on the margin strategy be to stay away from the Mass centric stocks (LVS, Sands China, SJM, MPEL)?

the SET-UP

As early as March 10, we pivoted to the sidelines when we removed LVS from our Best Ideas list, see our note “LVS: REMOVING FROM INVESTING IDEAS” and shortly thereafter warned investors about junket issues, the Dept of State request to lower the threshold for reportable financial transactions, UnionPay, money laundering scrutiny, as well as the extreme sentiment indicator with the massive “buy” rating skew on MGM, LVS, WYNN, and MPEL. (see chart below).

We were incorrect in thinking May GGR growth would be the last positive catalyst for the Macau stocks over the intermediate term. Obviously, that catalyst failed to materialize and May growth disappointed. But looking ahead, we still only see negative catalysts: continued weak VIP driving monthly GGR growth into single digits, the smoking ban impact on premium mass, and potentially most important, decelerating Mass growth.

Long-term, exposure to the mass segment will be advantageous but relative to sentiment, it may be where the risk lies over the near/intermediate term. The following table details mass revenue as a percentage of total GGR on a trailing twelve month basis as of the end of May 2014. Sands China (LVS) is the most exposed to the mass segment with more than 44% of revenues, followed by SJM with 35%, MPEL with more than 31% and Galaxy with almost 26%. The least exposed to mass is Wynn Macau (WYNN) with 22.1% and MGM China (MGM) at 23.1%. Our point here is that with all the investor concern surrounding VIP, stocks may have adjusted already for those issues, but maybe not for the upcoming mass deceleration.

The sell-side continues to reaffirm their conviction in the Macau gaming stocks based on continued growth in the Mass segment. Last week, one sell-side analyst wrote, “We believe mass market growth can continue to pace around 30% this year.” Another firm wrote, “We maintain a positive outlook on the sector, as mass, which is the key driver for EBITDA growth, remains robust.”

We believe in bold, intellectual honesty and insightful research with a focus on timing. As such we are compelled to enlighten our subscribers that growth in the Mass segment has probably peaked and the second derivative is about to go negative!

WHAT WE THINK WE KNOW

During Q1 2014 earnings conference calls, we heard a lot of talk from gaming operators regarding “yielding up” the mass segment. While visitation has increased, we believe the largest driver of the growth in the mass segment has been rising revenue per visitor. The big increase in table minimum bets and the changing mix toward tables with higher than minimum bets helped push that metric upward.

As an example, if a casino operated 500 mass tables but 400 tables had a HK$25 minimum bet while 100 tables had a HK$250 minimum bet, the effective yielded minimum was HK$70. Fast forward, this casino now “yields up” (increases minimum bets) so that the casino floor is now 250 mass tables with a HK$300 minimum bet and 250 mass tables with a HK$500 minimum bet, the effective yielded minimum is now HK$400.

So, while not increasing the number of visitors nor the speed of play, the casino has now effectively increased volume by 5.7x assuming the same number of hands played at the same speed. Thus, the growth in the mass segment could in fact be driven entirely on “yielding up” rather than increased visitation. Obviously, casinos cannot do this forever.

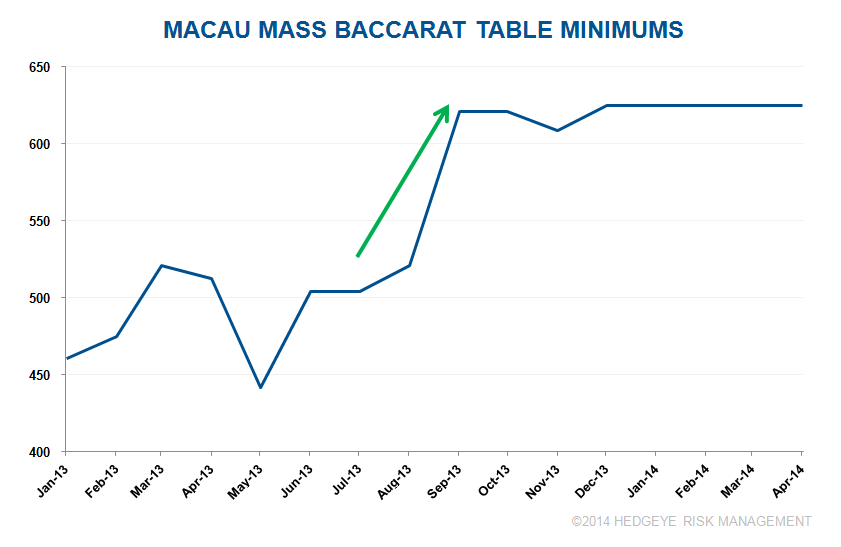

When we review mass segment baccarat table minimums, we notice a significant increase (or yielding up) occurred during July and August of last year. Said differently, the mass segment is about to anniversary more difficult average table minimums, thus making year-over-year growth more difficult.

THE FORECAST

When we put all our quantitative and qualitative analysis together, we forecast a slowing of the mass segment on a market basis – from >35% growth to 19-20% by the end of the year. We don’t believe investors fully appreciate the impact of yielding up, more difficult comps, and the resulting slowing second derivative of the mass segment. As a result, we see additional negative earnings revision and valuation risk to the Macau gaming operators – beyond what is currently expected in the market.

conclusion

We remain very constructive regarding the long-term outlook for Macau operators, particularly those with a well defined mass strategy and mass exposure. However, with all the focus - and rightly so - currently on the VIP issues and overwhelmingly bullish sentiment surrounding mass, we caution investors that mass deceleration is likely and could further pressure the stocks.