TODAY’S S&P 500 SET-UP – June 12, 2014

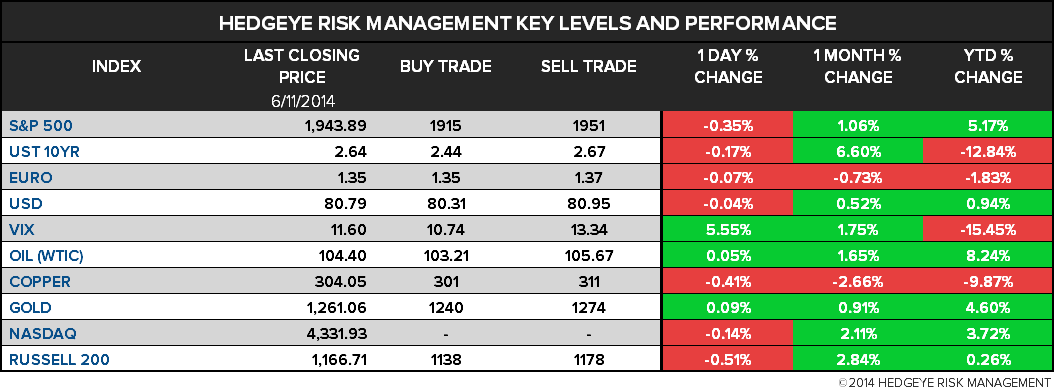

As we look at today's setup for the S&P 500, the range is 36 points or 1.49% downside to 1915 and 0.37% upside to 1951.

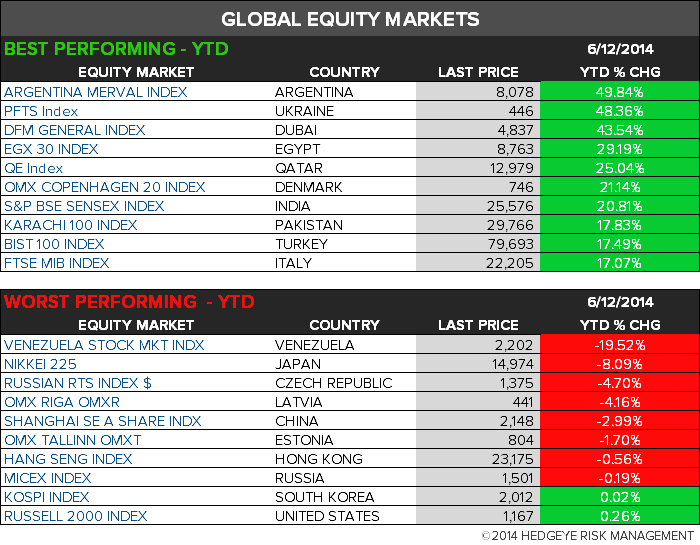

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.21 from 2.21

- VIX closed at 11.6 1 day percent change of 5.55%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Retail Sales, May, est. 0.6% (prior 0.1%)

- 8:30am: Import Price Index, May, est. 0.2% m/m (prior -0.4%)

- 8:30am: Initial Jobless Claims, June 7, est. 310k (prior 312k)

- 8:45am: Bloomberg June U.S. Economic Survey

- 9:45am: Bloomberg Consumer Comfort, June 8 (prior 35.1)

- 10am: Business Inventories, April, est. 0.4% (prior 0.4%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- President Obama meets with Australia PM Tony Abbott

- House, Senate in session

- Senate Approps Cmte to mark up HHS, Education, Labor, legislative branch spending bills

- FTC Commissioner Maureen Ohlhause, House Intelligence Chairman Mike Rogers discuss future of cybersecurity at AEI

- Senate to vote on confirmation of Stanley Fischer as Fed vice chairman, Jerome Powell for second term on Fed Board, and Lael Brainard as member of Fed Board

- 7:30am: Abbott remarks at U.S. Chamber of Commerce breakfast

- 9am: Defense Dept hearing of Guantanamo Periodic Review Board for for Faez Mohammed Ahmed Al-Kandari

- 10am: Supreme Court to issue decisions

- 11am: CFPB Director Richard Cordray to speak at mobile fin. services field hearing in New Orleans

- 12pm: Sens. Heidi Heitkamp, D-N.D.; John Barrasso, R-Wyo.; speak at Natural Gas Roundtable

- 12:30pm: SEC Commissioner Stein joins Peterson Institute discussion on systemic risk

- U.S. ELECTION WRAP: Democrats Seek Edge Amid GOP Splintering

WHAT TO WATCH:

- Bank of America sways judge to reconsider SEC mortgage case

- French govt examining all bids for Alstom energy: official

- Intel loses EU court bid to cut record EU1.06b antitrust fine

- Euronext delays open of cash markets on connectivity fault

- Airbus pitches A380 jumbo jet in New York after Emirates snub

- GM ignition-switch defect response probed by eight states

- Amazon’s new music service said to hit snags with Universal

- Musk plans Tesla patent move after hint of sharing with rivals

- Mickelson not subject of Clorox trade probe, NYT reports

- Dianping said to appoint advisers for U.S. IPO

- LG Household still reviewing making bid for Elizabeth Arden

- Senate plans Fed nominee confirmation votes on Fischer, Powell, Brainard

- China money supply unexpectedly rises as new loans jump

- E-cigarettes gain potential benefit in FDA focus on nicotine

- Islamists extend military gains in Iraq; U.S. asked for help

EARNINGS:

- Lululemon Athletica (LULU) 7:15am, $0.32

- Dollarama (DOL CN) 7:30am, C$0.77

- Finisar (FNSR) 4pm, $0.38

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Trades as High as $105.24/Bbl, Highest Since Sept. 20

- Copper Trades Near June Low as Chinese Probe Might Curb Demand

- Strike Curbs Palladium Supply as Auto Demand Surges: Commodities

- Palladium Below 13-Year High as Strike Union to Meet Members

- EU May Decide on Carbon Reform in 1st Half of 2015, Delbeke Says

- Wheat Rises as Traders Weigh U.S. Outlook Against World Supply

- Cocoa in London Climbs to Highest Since Aug. 2011 as Sugar Falls

- Iron Ore Price Forecast Cut by Morgan Stanley as Supply Expands

- Iran’s Increasing Oil Exports Challenge Obama Nuclear Sanctions

- China’s State Reserve Said to Check Copper Purchases Amid Probe

- California Warns of Oil-by-Rail While Keeping Data Under Wraps

- Ghana’s Smaller Cocoa Crop Seen at Risk of Damage From Poor Rain

- Limited Crude Oil Spare Capacity Supports Oil Price: Bull Case

- EU Gas Traders Ignore Ukraine Offer Rejection as Talks Continue

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

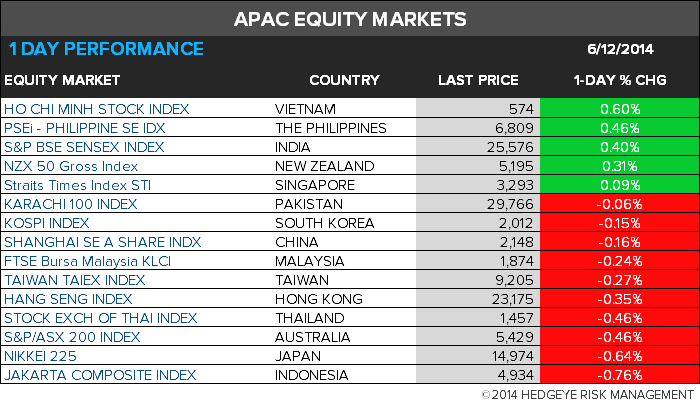

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team