Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

*Note - to maintain cross-metric comparability, the purchase applications index shown in the table below represents the monthly average as opposed to the most recent weekly data point.

Today's Focus: MBA Mortgage Applications

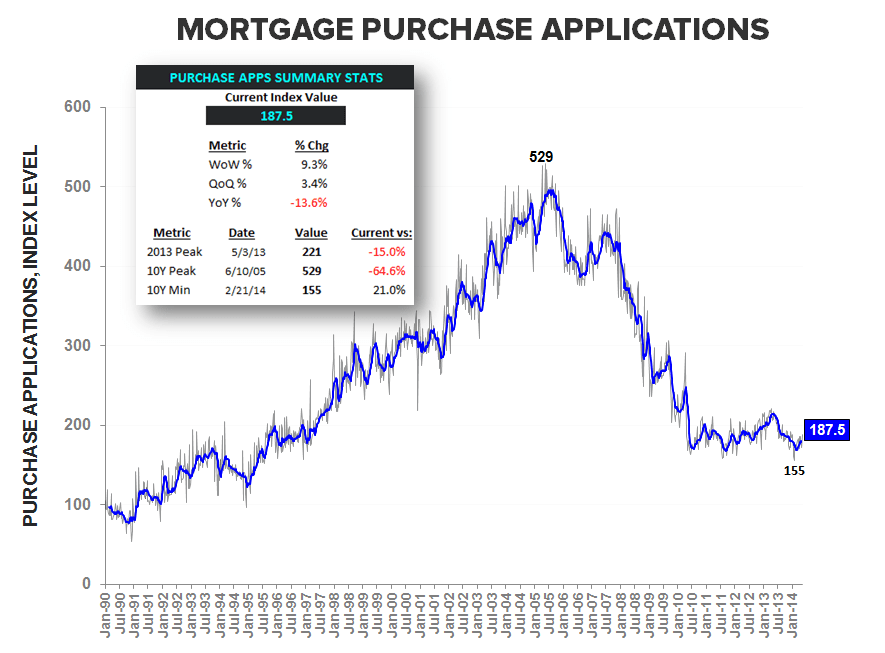

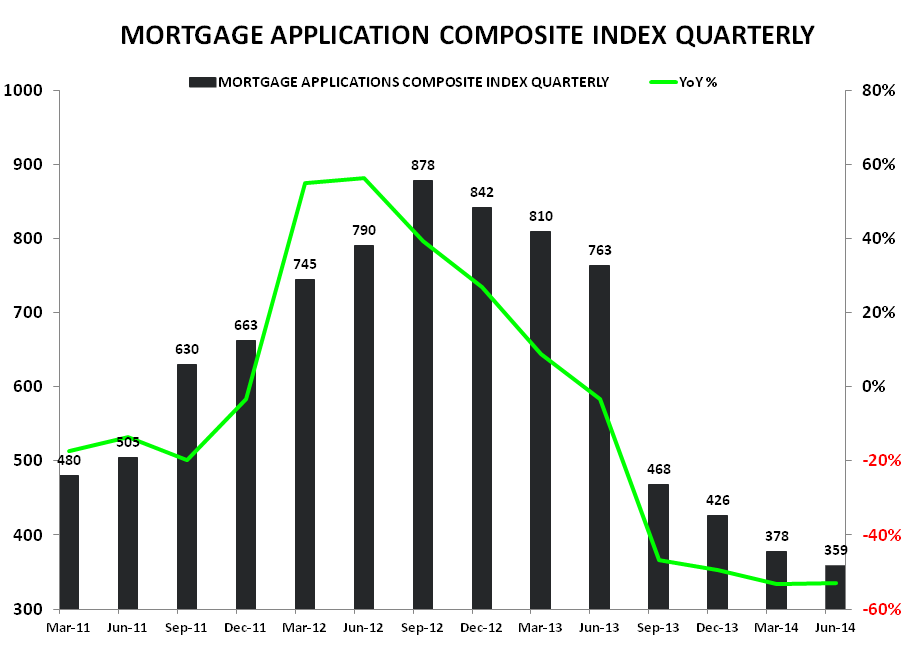

The Mortgage Bankers Association today released its weekly mortgage applications survey data for the week ended June 6. Mortgage purchase application volume rose +9.3% week-over-week, which improved the series to -13.6% YoY vs -17.2% YoY in the week prior. The QoQ is currently running at +3.4%.

Prior to last week, the purchase index had declined for four consecutive weeks. The Memorial Day holiday week was the week that preceded last week so it's possible/likely that there was demand that was time shifted.

As a general rule of thumb, anytime there is a holiday involved we tend not to get overly excited by sharp turns in the data in either direction. Next week should be a better indicator of the underlying trend in demand.

Activity heated up on the refi side as well. Consistent with lower rates - current 30Y FRM contract = 4.34%, up from 4.26% prior but still at best levels in a year - refi application volume rose +11.0% W/W, reversing the trend of the prior two weeks.

We're more interested in the mortgage purchase volume data as it's the better leading indicator of the direction of housing's momentum, while the refi data is largely a reflection of rates on a coincident basis.

Our expectation remains that as we enter the back half of this year and the first half of 2015 we should see growing downward pressure on the rate of home price appreciation.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake