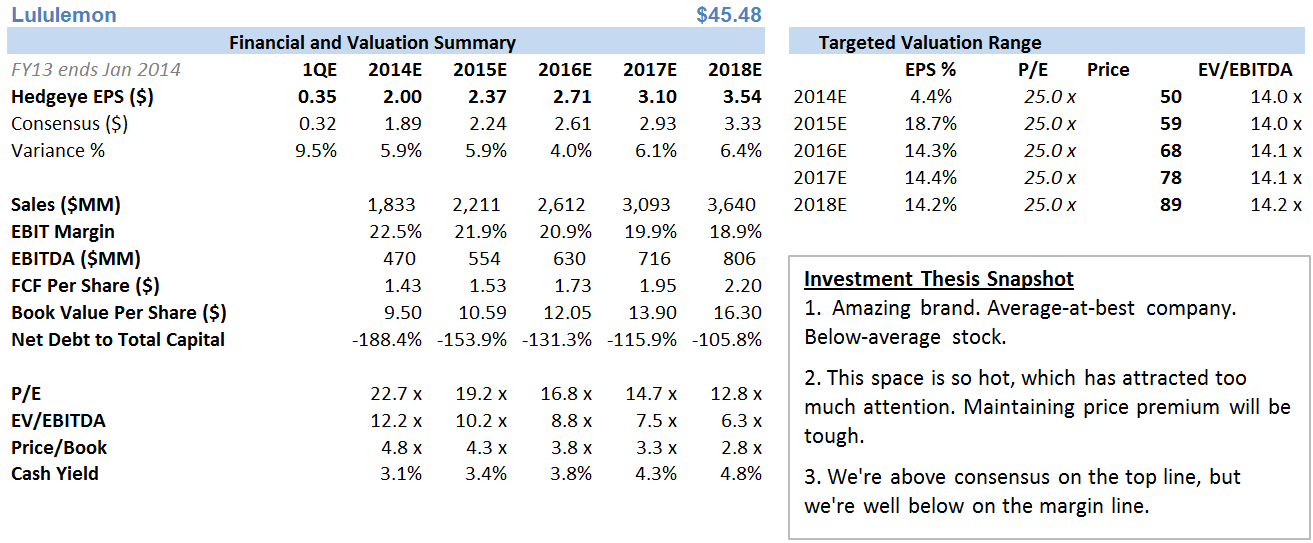

Conclusion: The equity value destruction and erosion in sentiment since LULU’s ‘new CEO party’ in April served as a massive ‘show me’ invitation from Wall Street to LULU management. This is a superb brand that is backed by a sub-par company and lackluster management. A good quarter on Thursday might buy the CEO time before he has to actually articulate a growth plan. But a miss, from where we sit, should trigger more management changes. No change in how this company operates, will likely result in another new CEO six months down the road. For now, we’re actually positively biased on the print. If LULU misses, we’ll likely go all-in. Yes, there are competitive margin pressures. At $75 that was a problem – at $45, not so much. There’s $3.50 in earnings power, and a call option on getting acquired. A sell-off means higher likelihood of change in the C-Suite. The risk/reward here is starting to look really attractive.

DETAILS

To say that this is a critical quarter for Lululemon is an understatement. We wonder if management even knows. The Street is clearly betting against the company, as the stock is down 16% since the analyst meeting, and short interest (24% of the float) is nearly on par with levels (25%) that we saw last Spring when the ‘see thru’ Luon fiasco broke out. Laurent Potdevin has been CEO for a good six months, and although it’s too short a window for even a good manager to be a factor of change, it is certainly soon enough for the company to be articulating its go-forward growth plan. That was the biggest miss back at the analyst event. No strategy. If Potdevin didn’t get the message with how the stock has since reacted, then he shouldn’t be CEO. If he got the message and does not do anything about it, then he shouldn’t be CEO. Shareholders deserve better. It’s pretty simple, actually. Accountability 101.

So…we’ll see on June 12th whether or not Mr. Potdevin ‘gets it’. But the punchline, we think, is that this is one of those situations where, for the most part, ‘good is good, and bad will ultimately lead to good’. Our point is that the company either…

a) meets or beats the quarter, and buys itself more time before it has to show that it has a firm grasp on the long term growth strategy and the capital needed to achieve those plans. = Good Stock Event

b) meets or beats the quarter AND outlines crisp long term growth strategy. = Great Stock Event

c) Misses the quarter and outlines crisp strategy = Neutral Stock Event, depending on the size of the miss

d) Misses the quarter and still comes across as a deer in the headlights as it relates to Strategic Plan. Initial event will be very negative. The Board will have to answer to this – either because an activist says so, or the value destruction is so obvious. = Negative Stock Event leading to a potentially very positive event/change

We’re obviously getting a bit too cute with the outcomes here. But if we see an event that is negative enough for the stock to sell-off in spite of the 26mm shares held short, then we’ll likely go all-in on this one. The reality is that LULU is a great brand, is in a high-growth industry with global appeal and acceptance. Yes, there’s fierce competition and we think that margin expectations are way too high. At $75 that was a problem – at $45, not so much. The growth is there, and those kind of brands don’t come around too often. Even at a 19% EBIT margin (vs 24% last year) we get to $3.50 in earnings power with a call option on being acquired. The issue here is that it is a great brand backed by a sub-par company. That can be fixed.

What change? We still don’t think that the Board’s hiring process for Potdevin was anywhere near as rigorous as it should have been for a company the size of LULU. That said, we don’t think that his perceived failures to date are entirely his fault. He has extremely poor support in the C-Suite, particularly his CFO. In our opinion, John Currie was a great CFO when LULU was sub $500mm in sales 5-years ago. But he’s not the guy to be building a world class finance organization for a company that is $1.5bn in revenue that should have a plan to get to $5bn. It’s not his fault, per se, but the fact of the matter is that things like Finance, Strat Planning, and building the organizational depth of a world class company were never a priority at LULU. That’s common for many early cycle companies. But it needs to become a priority here. If Currie can’t do it, then Potdevin will be on the hook for things that are not within his skill set. Ultimately, LULU needs to turbocharge how it plans its business and match what is a limited capital budget to an unlimited number of growth opportunities. Potdevin has what is likely another six months to get this right. If not, we wouldn’t be surprised to see another new CEO.