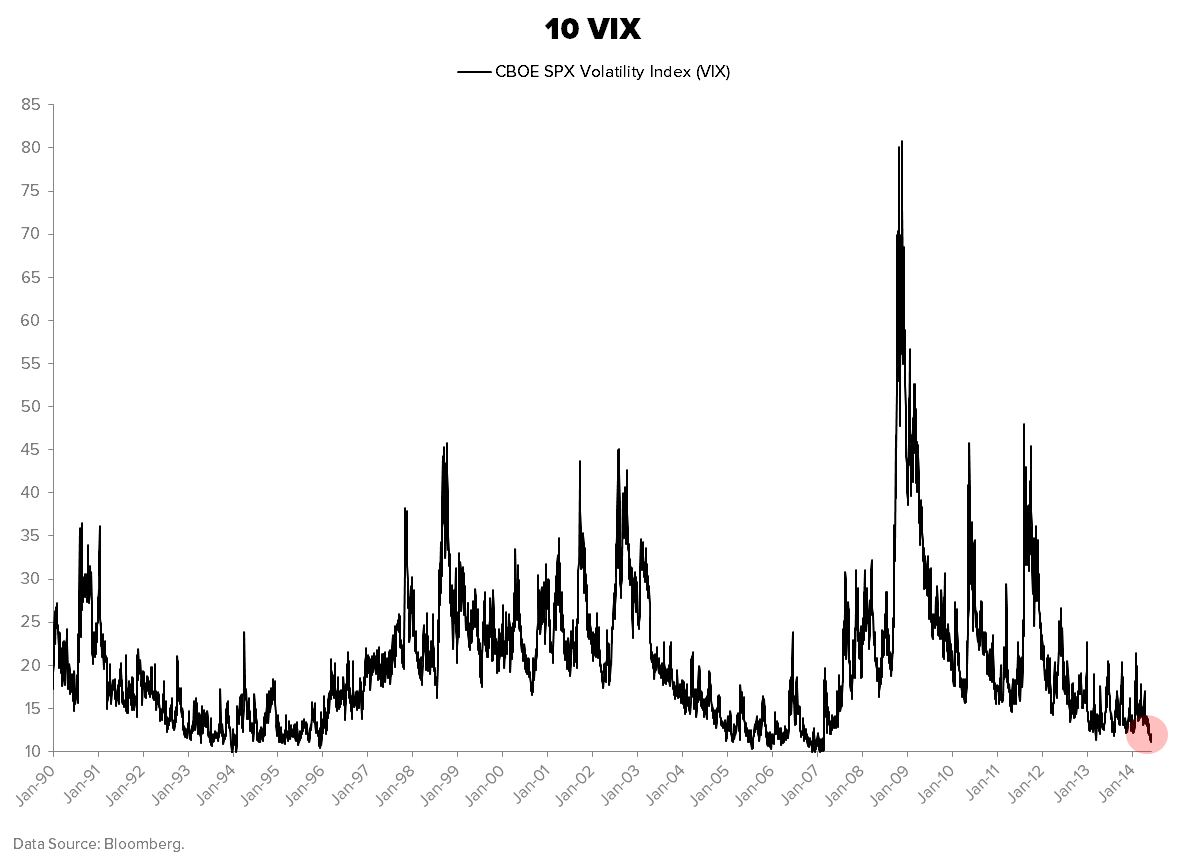

Takeaway: Front-month VIX officially crashed last wk (-21.7% year-to-date) .

Takeaway: Front-month VIX officially crashed last wk (-21.7% year-to-date) .

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.