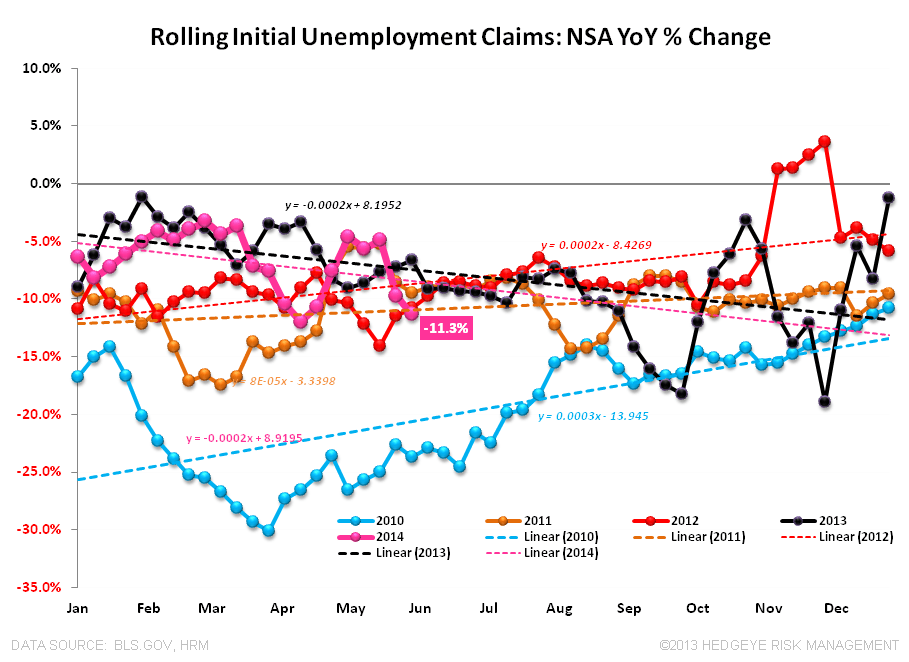

INITIAL CLAIMS: BACK AT BEST LEVELS YTD

- The Data: Headline claims increased +8K WoW to 312K with the 4-wk rolling average declining another -3K sequentially to +310K. Non-seasonally adjusted claims, which we consider a more accurate representation of the underlying labor market trend, came in at -10.8% YoY (vs. –13.8% prior) with the 4-wk rolling average improving 160bps sequentially to -11.3% YoY.

- Context: The rate of change in year-over-year, rolling non-seasonally adjusted claims improved to its best level in seven weeks and is near its best level YTD while rolling SA claims hit their lowest level since June 1st 2007. As a reminder, we typically look at the slope of improvement as our indicator on the prevailing trend in the labor market. Historically, however, the 300K level has served as the lower bound in seasonally adjusted claims during expansionary periods. At this weeks reading of +310K we continue to converge towards that frictional lower bound and expect the rate of year-over-year improvement to slowly converge towards 0% as well.

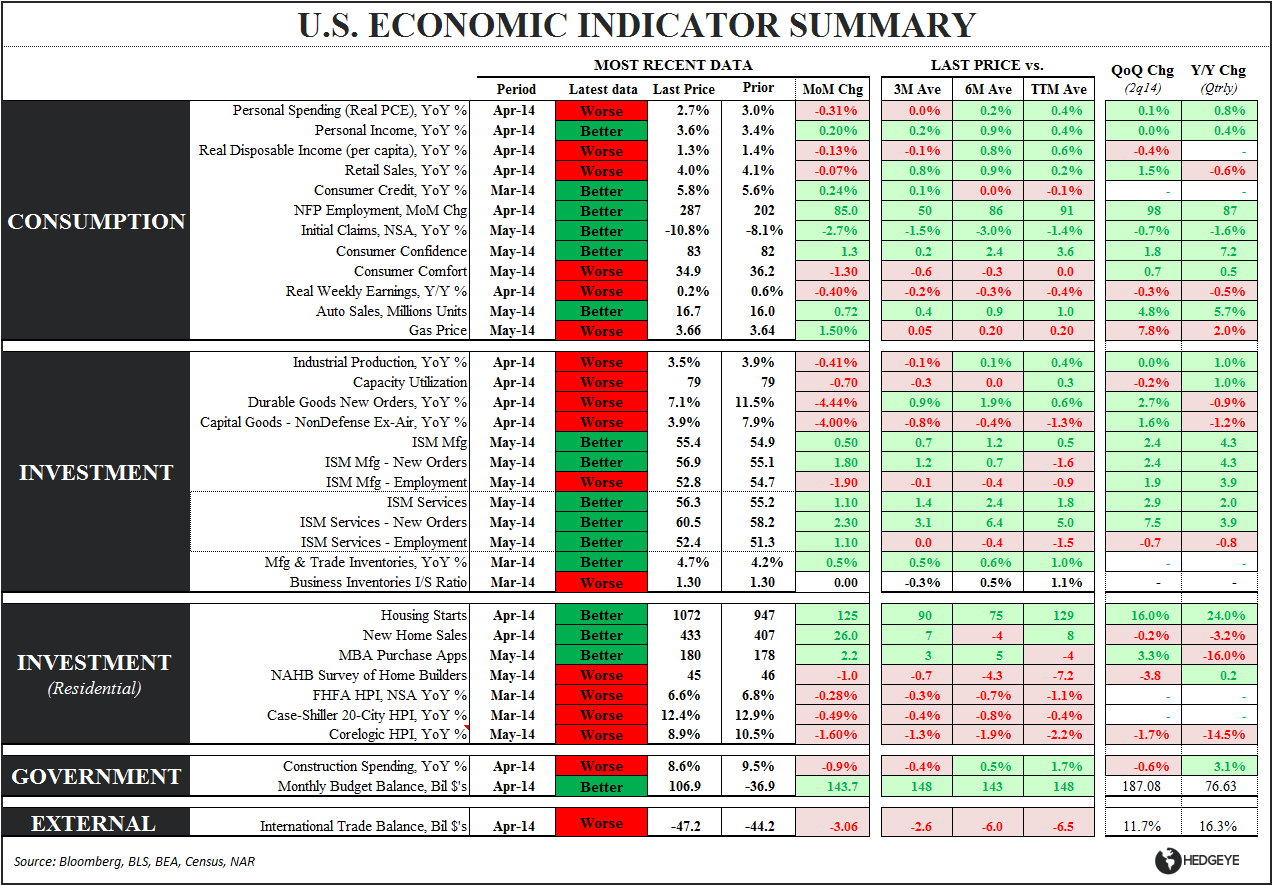

On balance. the domestic macro data has been better sequentially QoQ, but outside of the discrete ramp in Auto Sales in May (more on that below), there hasn’t been much evidence of material deferred demand from 1Q coming back in 2Q.

The national and regional manufacturing surveys have been ‘good’ and the labor market data (ADP was soft but the trend in claims remains positive) has been stable-to-better.

However, April retail sales were weak, consumer spending in April was particularly soft (see: #GRAVITY: April Consumer Spending), the trade balance for April was worse than estimates (with March revised lower, taking 1Q GDP further negative), and the housing data remains in conspicuous deceleration (see yesterday’s note: Housing: 4th consecutive week of decline in demand).

From a policy read-through perspective, the positive momentum in the labor market along with the broader, sequential improvement in the domestic macro data off the 1Q14 weather distortion suggests the inertia is still with continuing on the present policy course (June FOMC meeting is June 18th).

The improvement in claims also bodes well for the May employment report. While SA claims reported during the BLS survey period (conducted during the pay period including the 12th of the month) were less good than the most recent two weeks, on balance, the May claims data is supportive of a good NFP print.

A Quick Note On Auto Sales:

Total vehicle sales jumped to 16.7M in May (vs. 16.1M est. and 15.98M prior) and auto financing remains one of the only consumer loan categories showing positive growth. However, ongoing loan growth in combination with loosening of credit standards and increasingly aggressive financing options places auto financing (& those levered to it) near the top of the prospective bubble list.

Jeff Williams, CFO of America’s Car-Mart, aptly captured the reality of today’s auto lending dynamics in his comments on 5/27:

“We believe that our customers have never been more stressed financially and, at the same time, have never been presented with more aggressive financing options for their vehicle"

…keep the ongoing auto credit munificence somewhere on your monitoring list.

Enjoy tomorrow mornings manic employment release myopia, May edition.

Christian B. Drake

@HedgeyeUSA