While we don’t have a crystal ball on how the ECB will act tomorrow, we do know that the Bank has historically surprised (when the ECB last cut the benchmark interest rate in November 2013, from 0.50% to 0.25%, it was widely unexpected by consensus). Frankly, we wouldn’t be surprised if Draghi underwhelms the market’s lofty expectations this time around, and we’re setting ourselves up to buy the EUR/USD (etf FXE) on weakness as we think 1) the sell-off is largely priced in following weeks of rumors about the ECB’s intent to act, and 2) the predictable dovish monetary response by the Federal Reserve as growth surprises to the downside should continue to aid our bearish call on the USD. (Here we look forward to the FOMC statement on the 18th for confirmation.)

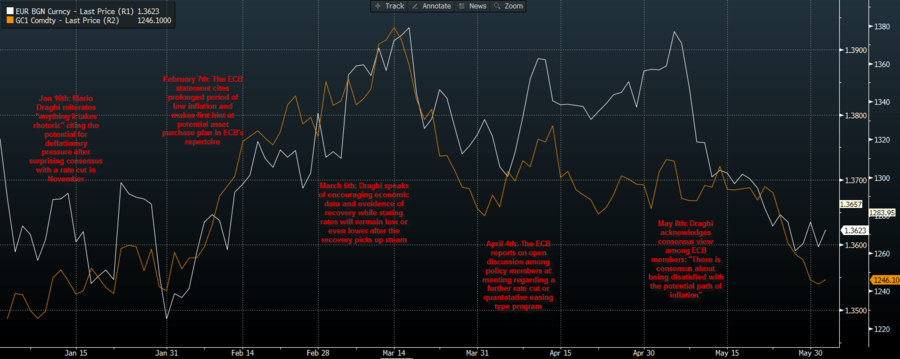

The headline CPI estimate in the Eurozone came in lighter than expectations yesterday, increasing at an annual rate of +0.5% for the month of May while consensus expected +0.6%. Today’s preliminary Q1 Eurozone GDP release printed in-line with expectations at +0.9% year-over-year. With the Euro coming off -2.0% from the March 18th high of $1.3934 and Gold (priced in USD) decreasing -4.5% over the last month, the market expects something from the ECB tomorrow. Draghi’s “whatever it takes rhetoric” about fighting what he has labeled a “Japanese” style deflation risk in recent weeks has successfully strengthened the market’s expectation of a dovish policy move at 7:45 a.m. EST tomorrow morning. In a survey of economists released by Bloomberg, 44 of 50 expect the ECB to implement a negative deposit rate. In a separate survey, 56 of 58 expect a cut in the benchmark interest rate. Consensus estimates expect the ECB to cut its deposit facility rate from 0.0% to -0.10% with the benchmark interest rate being cut from 0.25% to 0.10%.

We believe Gold is a hedge against future dollar devaluation and the price activity in both the Euro and Gold have legitimized this view. We added Gold (etf GLD) on the long-side to Hedgeye's investing ideas list on May 22nd:

The Euro-Gold correlations have trended much stronger relative to historical interaction since the ECB’s first mention of an asset purchase plan back in February:

Gold has historically held a meaningful negative correlation to the arithmetic mean of the U.S. Dollar and ten-year treasury yields. As growth surprises to the downside, the expectation for future dollar devaluation in response to Fed policy response increases. Judging by the move in Gold and currency markets into the meeting, anything short of a significant move from the European central bank is widely unexpected.

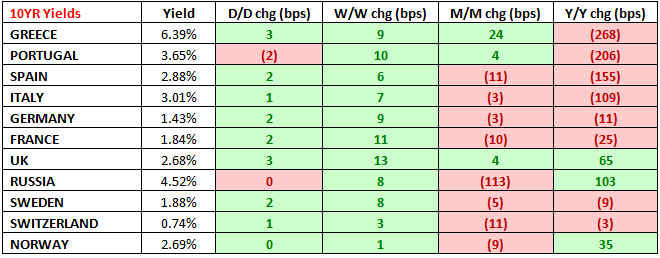

Also, the anticipation of even easier policy from the ECB moving forward has pushed sovereign debt yields across the Eurozone to historically low levels. Ten-year yields have come in significantly over the last year:

After receiving a $125Bn IMF aid package just two years ago, Spanish yields now hover approximately 30bps over ten-year treasuries. Portugal, which just exited its IMF bailout program in March, borrows at ~100 bps over treasuries. A Bloomberg article published yesterday noted just how drastic this shift has been:

“Bond yields in Germany and its predecessors haven’t been this low since at least the early 1800s, when French forces under Napoleon Bonaparte fought wars throughout the European continent.”

The Federal Reserve is up next on June 18th, and we expect a dovish statement after a horrendous revised Q1 GDP print last week.

We continue to play the sector variances in the market as growth slows and inflation accelerates in the U.S. by remaining long of utilities (XLU +12.6% YTD), REITs (+15% YTD), and commodities (CRB +9.0% YTD; GLD +8.7% YTD). We remain short of consumption-driven sectors that negatively diverge as the consumer is squeezed with inflation: XLY (-1.2% YTD) and IWM (-2.6% YTD). As the prospect for future dollar devaluation increases, we like leaning long of inflation in Gold terms as consensus GDP comps for 2H14 become merely impossible. Despite the slowdown, our non-consensus call into Q2 of 2014 remains just that: NON-CONSENSUS. JPMorgan recently cited that its clients have not been as short of treasuries since 2006. Bullish bets on Gold peaked in Mid-March, right before the Euro began selling off from its YTD highs.

Macro Team