This note was originally published at 8am on May 19, 2014 for Hedgeye subscribers.

“Some questions have no answers to find.”

-Niels Bohr

This weekend I changed things up a bit and started re-reading a play called Copenhagen which is based on a meeting of the physics minds of Niels Bohr and Werner Heisenberg in 1941.

The timing of the play opening on Broadway (April of 2000 at the top in the US stock market) is interesting. I was a newbie on Wall Street back then. I didn’t know much more than I know now about why this time the bubble is “different.”

Copenhagen’s opening scene starts with four questions exchanged between Bohr and his wife, Margrethe:

Margrethe: “But why?”

Bohr: “You’re still thinking about it?”

Margarethe: “Why did he come to Copenhagen?”

Bohr: “Does it matter, my love? Now we’re all three of us dead and gone”

Back to the Global Macro Grind…

But why do bond yields keep going down? Why is Old Wall consensus still expecting 3.32% for the 10yr US Treasury yield for 2014 when it’s currently trading at 2.51? Why did consensus come into 2014 expecting US Growth to accelerate, and inflation to fall? Does it matter, my friends?

These questions obviously have obvious answers – unless you are paid to anchor on estimates that are dead wrong, that is. As #InflationAccelerating slows real US growth expectations for 2014, some serious questions remain as to why Wall Street and Washington have not yet come to agree with gravity.

This is, of course, the upshot of Copenhagen – Heisenberg (not the Breaking Bad dude, but Walter White was named after him):

“No one understands my trip to Copenhagen. Time and time again I’ve explained it. To interrogators and intelligence officers, to journalists and historians. The more I’ve explained, the deeper the uncertainty has become…”

“So” embrace the uncertainty associated with how an unprecedented level of un-elected central planning is affecting the rate of change in both growth and inflation in the US economy. There is nothing linear about this.

In addition to US Bond Yields getting hammered last week, here’s what Mr. Macro Market had to say about US growth:

- Growth Stocks (Russell 2000) down another -0.4% last week to -5.2% for 2014 YTD (down -8.8% since March)

- Yield Spread (10yr yield of 2.51% minus the 2yr yield of 0.36%) compressed another 8 basis points on the week (-48 basis points YTD)

- Financials (XLF) were the worst performing sub-sector of the SP500 at -0.8% on the week to -0.5% YTD

In other words, as the long-end of the curve (10yr yield) dropped -10 basis points on the week (-51 basis points YTD), not only is that a leading indicator for US #GrowthSlowing, but it’s as good a proxy as any for bank earnings (net interest margin tracks the Yield Spread).

But why?

Everyone who has followed market history knows why. There isn’t a person in this profession who can tell you with a straight face that growth stocks, financials, and bond yields all declining at the same time is a bullish growth signal.

Neither can they tell you that food and oil prices accelerating is a consumer tax cut. Here’s the update on that:

- Oil price up another +2.3% last week (breaking out above @Hedgeye TAIL risk lines of resistance)

- Cattle prices up another +1% last week to +13.5% YTD

- REITS up another +0.4% last week to +14.6% YTD

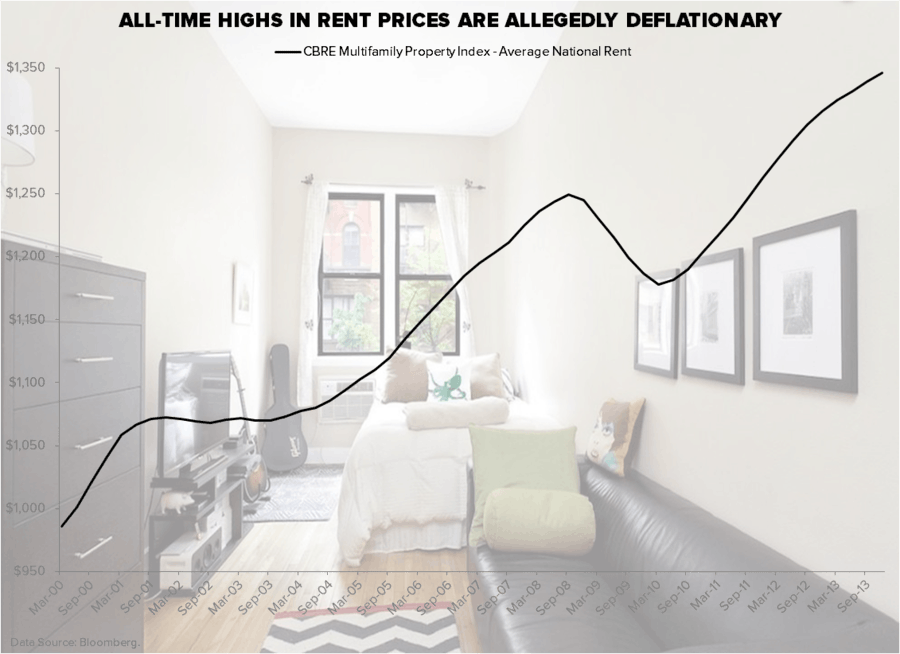

Oh, you mean you don’t eat REITS? But you’re still thinking about chasing some slow-growth yield? Obviously cost of living is ripping in this country, and since 1/3 of Americans rent, they can eat that inflation – and like it, because as Heseinberg explained in Breaking Bad, “I say so.”

The only good news I can give you on the US stock market is that buy-side consensus is starting to figure out the #InflationAccelerating slows US consumption growth theme. Here’s the updated CFTC Non-Commercial net long/short positions in the Big Macro stuff that matters:

- SPX (Index + Emini) closed the wk with a net short position of -40,901 contracts (vs. an avg NET LONG position of +16,256 contracts over the last 6 months)

- 10YR Treasury has a net long position now of +23,948 contracts (vs an avg NET SHORT position of -81,337 contracts over the last 6 months)

Put another way:

- If you were long growth equities and short bonds 6 months ago, you were killing it (but about to get killed)

- If you made the turn (out of growth stocks into slow-growth bonds) in the last 6 months, you are still killing it

Just because consensus is moving the way of economic gravity doesn’t mean the move is done. In Breaking Bad, Walter White explained this reality quite effectively to Saul too: “We’re done when I say we’re done.” And that’s all Mr. Macro Market is going to have to explain about that.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.48-2.61%

SPX 1861-1882

RUT 1089-1111

USD 79.16-80.21

WTIC Oil 101.05-102.97

Gold 1281-1318

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer