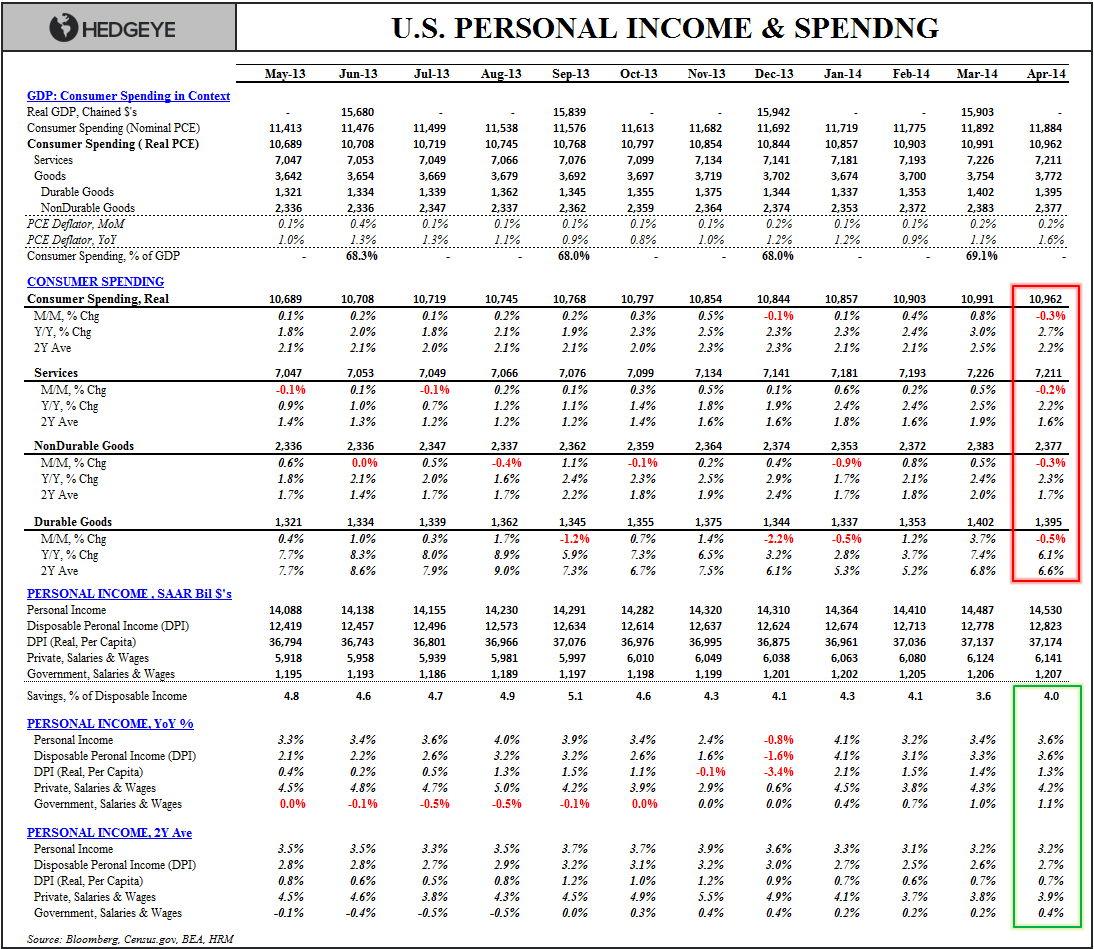

Summary: The savings rate ticked up, the rich reduced spending on luxury goods and the estimate of healthcare consumption growth decelerated. The result = negative MoM growth in real consumption across services, durables, and nondurables with all 3 decelerating on a YoY & 2Y basis as well. Growth estimates will get clipped (again).

As we’ve suggested repeatedly over 1H14, the current level of consumption growth (which sat as the singular source of strength in 1Q14 GDP) is overstated and/or unsustainable at reported 1Q14 levels.

Summarily, the thinking is essentially this:

The savings rate is at historic lows (meaning incremental consumption growth can’t be achieved via further savings reductions) while the conflation of static income growth and rising inflation (growing at multiples of income growth in some instances) will constrain the capacity of other discretionary consumption.

Accelerating spending on luxury goods buttressed a broader deceleration in demand for durables to start the year and the outlier acceleration in healthcare spending (which is very much an estimate and seemingly overstated in the context of reported 1Q14 Hospital results – see yesterday’s note MEXICAN STANDOFF: CLAIMS vs. GDP vs. EXPECTATIONS) was a primary driver of the reported growth in Services Consumption in 1Q.

In the context of the above dynamics, the balance of risk to household spending growth is to the downside as the expanding spread between nominal spending and nominal earnings is unsustainable and any combination of higher savings, a deceleration in peak spending growth by the rich or lower estimates for healthcare spending growth would act as deceleration’ary pressures on PCE growth.

We saw all three of negative dynamics manifest to start 2Q as the savings rate ticked up (from 3.6% to 4%), the rich reduced spending on luxury goods and the estimate of healthcare consumption growth decelerated. The result = negative MoM growth in real consumption across services, durables, and nondurables with all 3 decelerating on a YoY & 2Y as well.

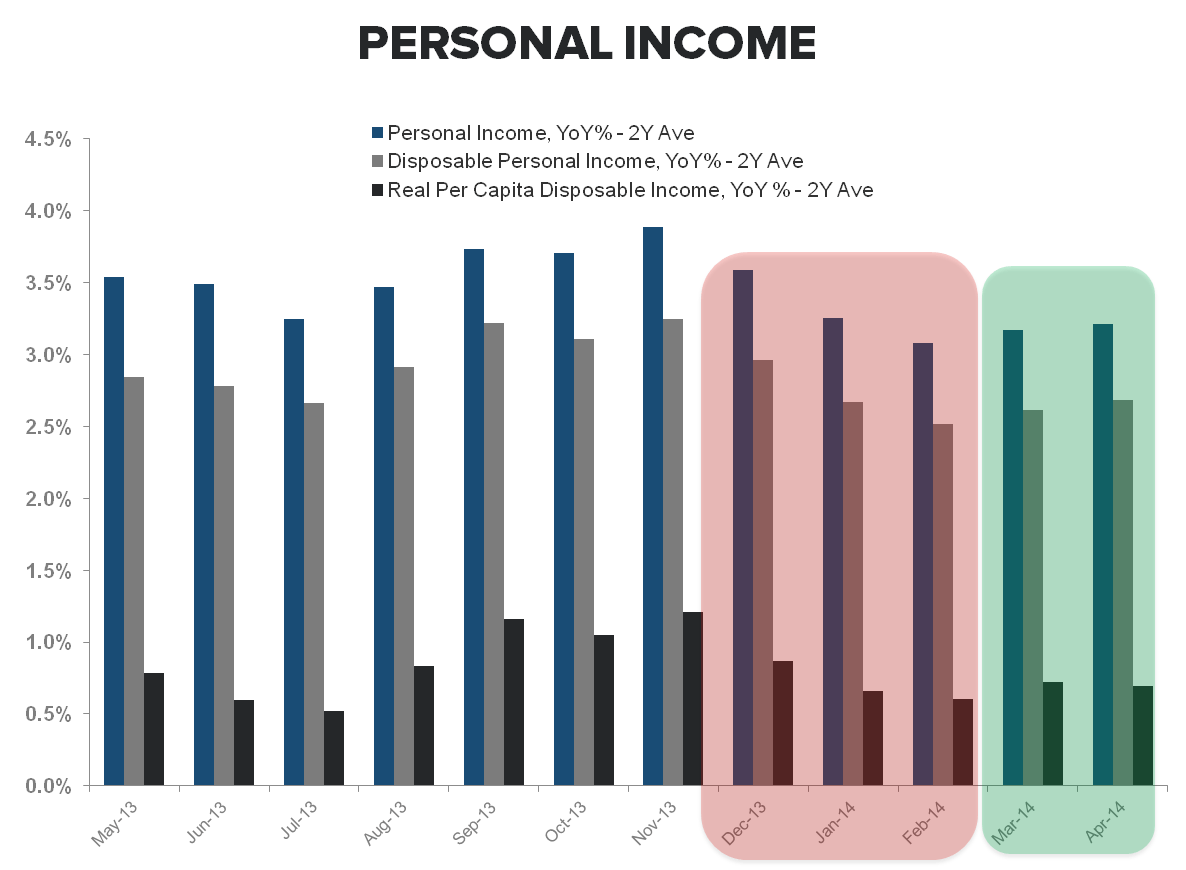

On the positive side, personal income growth, disposable personal income (DPI) growth, and aggregate private sector & government wage growth all improved marginally, sequentially. The sequential improvement is positive but not enough to support accelerating consumption growth, particularly alongside a higher savings rate, rising inflation, and a material slowdown in housing.

Growth estimates will get clipped (again) on today’s spending data, but consensus expectations for the balance of the year are still too high.

Enjoy the Weekend.

Christian B. Drake

@HedgeyeUSA