This note was originally published at 8am on May 16, 2014 for Hedgeye subscribers.

“Only the wisest and stupidest of men never change.”

-Confucius

I’ve been on vacation for most of the last two weeks. My first child is projected to be born on June 1st , so I figured it was best to take vacation now. This was based on the sage advice from some of the more seasoned fathers at Hedgeye.

I’m not always good at unplugging on vacation, but this time I did a decent job. As I was getting caught up last night, the most interesting article I read was from Business Insider. It seems while I was gone they anointed Hedgeye the most polarizing firm in finance!

I have to admit, even though Business Insider’s journalistic standards aren’t the highest, I thought that was kind of cool. When we started the firm more than six years ago, our sole intention was to shake things up. And it seems we have done so. So far, at least, mission accomplished.

Back to the Global Macro Grind...

So, the big question now that I’m back in the proverbial saddle is: what did I miss? Based on the return of the SPY, I’d say not too much. When I left for vacation on May 5th, the S&P 500 closed at 1,884.2. Yesterday it closed at 1870.85. For those that don’t have their HP-12C handy, that is a negative return of roughly -0.7%. Nothing to write home about to be sure.

Thankfully, my colleagues were keeping busy despite the lackluster performance in U.S. equities. Over the last two weeks on the idea side, we added two longs to our Best Idea list: Bob Evans Farms (BOBE) and Och-Ziff (OZM). Both ideas, though certainly very different, are very compelling.

Bob Evans Farms, as many of you may know, is a smallish cap restaurant company. Although our Restaurant Sector Head, the sage Howard Penney, has been more cautious than not on his sector, BOBE is one company he likes on the long side.

According to Howard the thesis is as follows:

- STODGY, OLD COMPANY: As you know, we are big supporters of change at DRI and feel that BOBE is in a very similar situation. BOBE is a stodgy, old company that has flown under the radar for far too long. It has a history of mismanagement evidenced by flawed strategic rationale, excessively bloated cost structures and severe underperformance relative to peers. Its poor operating performance presents a tremendous opportunity.

- UNLOCKING SIGNIFICANT SHAREHOLDER VALUE: We believe Sandell has identified significant, largely feasible, opportunities to enhance shareholder value. In our view, the opportunities are endless. More particularly, we see tremendous upside value in separating the foods business from the restaurant business, transitioning to an asset light model to capitalize on its vast real estate holdings, and attacking the middle of the P&L.

- THE OTHER SIDE OF THE TRADE: We have a ton of respect for Sandell and the work they’ve done. In fact, we believe that, over time, they have uncovered far more than they originally set out to. As a result, there is now an opportunity for them to capture bountiful, low hanging fruit that will immediately impact the company for the better. We believe in Sandell’s resolve and while the street is seemingly betting against them, we’ll gladly take the other side of the trade.

I’m not going to steal all of Howard’s thunder, but if you’d like more details, please email sales@hedgeye.com. Incidentally, another of Howard’s top ideas, Darden (DRI) announced this morning that they are selling one of their divisions, Red Lobster, to Golden Gate Capital for $2.1 billion. Oh snap!

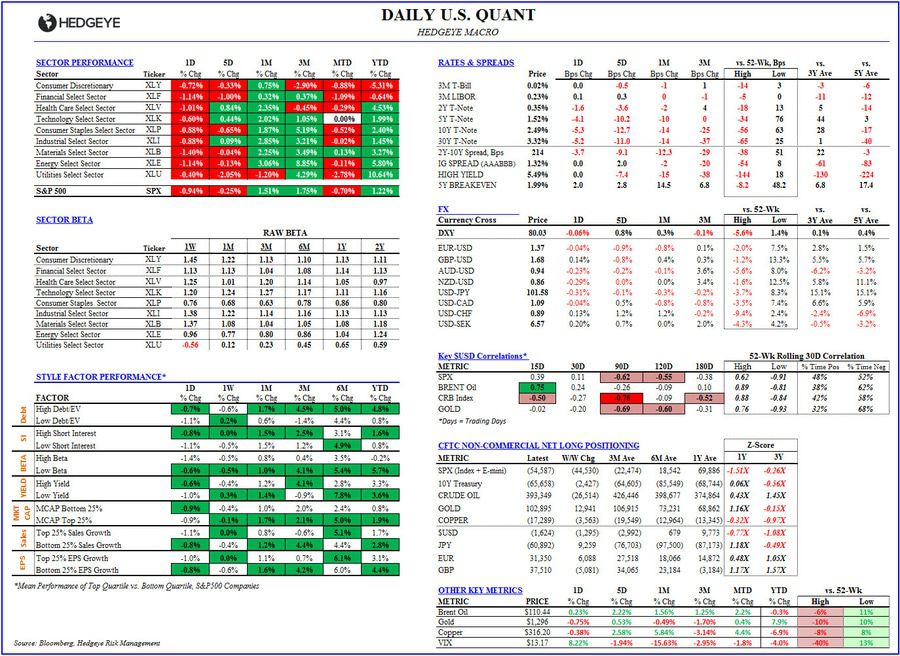

More broadly though, and other than a few alpha generating idea, those of us that vacationed for the first half of May didn’t miss a whole lot from return perspective. In the Chart of the Day below, I’ve highlighted our daily U.S. quant screen and for the month-to-date the worst performing SP500 sector is the Utilities, which is down 2.78%. Meanwhile, the best performing sector is Materials, which is up +0.13%.

On some level, that is actually new. Specifically, in May the worst performing sector is actually the best performing sector on the year. Currently, Utilities are up an impressive 10.6% for the year-to-date. Who would’ve thunk it?

Switching gears, on the global macro front this morning , the United Nations released a 37-page report on the human rights situation in the eastern Ukraine. On a serious note, that is actually not news, but does exemplify the ineffectiveness of the U.N. and its ability to deal with Vladimir Putin and the gong show in the Ukraine. But, at negative -13.4% on the year, the Russian stock market seems to be dealing with him appropriately.

Meanwhile, on the bond front, the bears seemingly just won’t give up. According to Bloomberg, the ProShares Ultra 20+ Year Treasury ETF (TBT) has seen inflows of 21.6% this year. This comes despite the ETF falling almost 21.6%. In addition, there are 1.12MM short contracts of treasury futures on the Chicago Board of Trade, which compares to the five year average of 713K. Further, a recent survey of economists expects the 10-year yields to rise 75 basis points by year end. Didn’t know what consensus in Treasury land was, now you know!

And as our nemesis John Maynard Keynes famously said:

“Markets can remain irrational longer than you can remain solvent.”

Indeed.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.49%-2.61%

SPX 1861-1882

RUT 1086-1112

VIX 12.14-14.52

USD 79.11-80.26

Gold 1281-1315

Keep your head up and stick on the ice,

Daryl G. Jones