While we are keeping BNNY on the Hedgeye Best Idea list as a short, it will be on a tight leash. Annie’s is a strong brand and we believe it will make a nice acquisition for a bigger food company someday.

Annie’s reported a disastrous quarter last night and we still don’t believe the company is on solid financial footing. While the balance sheet and cash flows are strong, the company continues to struggle to manage its high growth business.

Last night, BNNY missed on sales and margins, but was able to lessen the blow by aggressively cutting SG&A. To be clear, a growth company aggressively cutting SG&A is a sign of weakness, not strength, and we believe management lacks the infrastructure needed to grow the business. As expected, guidance for FY15 was well below Street expectations on both the top and bottom lines.

There are numerous ongoing issues the company faces:

- It has been unable to deal with the significant inflation in organic wheat.

- In an attempt to foster top line growth, management has forced innovation by entering new categories leading to significant inventory obsolescence and lower product mix.

- Management has not invested in the human capital needed to manage the business.

- Increased trade spending in a competitive retail environment.

- Insufficient internal controls.

- Increased competition.

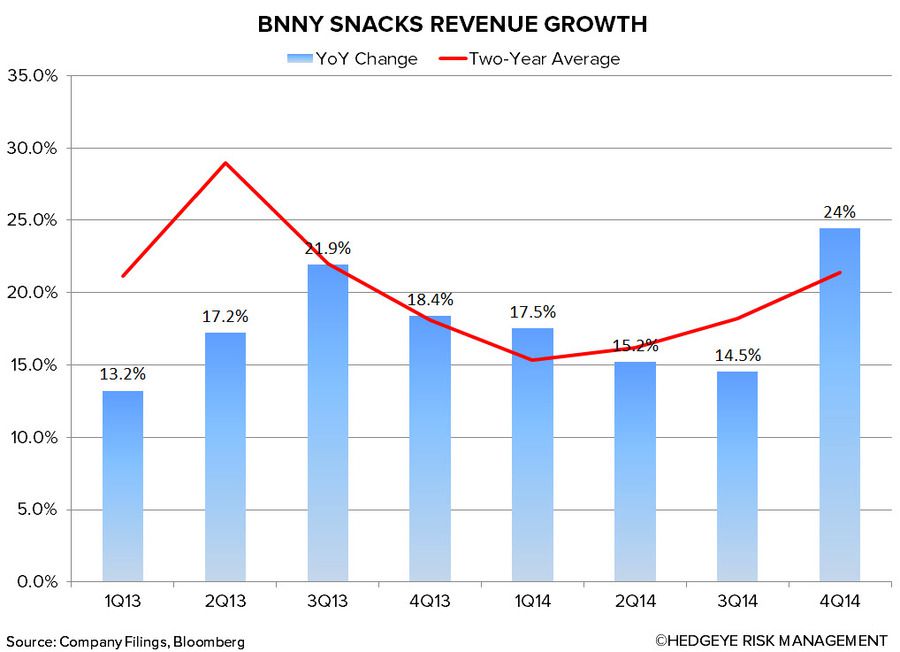

Management guided to sales growth of 18-20% (including the impact of the Joplin plant acquisition) versus the Street’s 18%. However, we’d argue that the Street had not reflected the acquisition in their numbers, so management actually guided down expectations. Part of the slowing top line (3-4%) is coming from a planned system-wide inventory reduction from UNFI in 1Q15. Excluding the impact of non-core contract manufacturing revenues related to the Joplin acquisition, adjusted net sales of Annie’s branded products are expected to grow in the range of 14-16% in FY15. In FY14, consumption of Annie’s grew 21% and 20% in 4Q14.

BNNY continues to have zero leverage in its business model. In FY15, gross margin is expected to be “comparable” to FY14, while SG&A is expected to be up in part due to higher stock-based compensation and normalizing incentive compensation expense. Given how little visibility management has, the lack of internal controls, and the investment needed to manage the business, we’d surmise that current FY15 guidance is highly suspect.

Call with any questions.

Howard Penney

Managing Director

Fred Masotta

Analyst