Tickers: BYI, CZR, BEE, RCL, NCLH

EVENTS TO WATCH

- Mon June 2: Goldman Sachs Lodging, Gaming, Restaurant and Leisure Conference, New York

- Mon June 2 - Tues June 3: NYU Int'l Hospitality Industry Conference, New York

- Mon June 2 - Tues June 3: Midwest Gaming Summit, Rosemount, IL

- Tues June 3 - Thurs June 5: REITWeek, New York, NY

- Wed June 4 - Thurs June 5: Russian Gaming Week 2014

- Thurs June 5 - Todd in Vegas for slot suppliers mgmt meetings

- Tues June 10 - Thurs June 12: Bally Systems User Conference

Mohegan Sun

COMPANY NEWS

BYI – amended and restated its Corporate Credit Facility whereby the Company increased the facility by an additional $370 million to a maximum of $1.07 billion, extend the maturity date of the Company’s Term Loan A and revolving credit facility to May 27, 2019, and revise interest rate equal to either the applicable base rate or LIBOR, plus in each case a margin determined by the Company’s consolidated total leverage ratio, with a range of base rate margins from 0% to 1.00% and a range of LIBOR margins from 1.00% to 2.00%.

Takeaway: More buybacks or should we expect a small acquisition?

BEL:PM - Belle Corp (SINO:PM) – announced its intention to undertake a reorganization of its gaming assets under a separate listed entity. The Board of Directors of Belle Corporation approved a re-organization under which Belle will inject its 100% ownership of Premium Leisure Amusements Inc (PLAI) and its shares representing 34.5% of Pacific Online Systems Corporation into Sinophil (SINO:PM) Corporation, a subsidiary of Belle that is listed on the Philippine Stock Exchange. PLAI is part of the consortium that holds the PAGCOR license for "City of Dreams Manilla" to be operated by Melco Crown Philippines and located in PAGCOR Entertainment City. Belle will retain direct ownership of the land and building of City of Dreams Manilla, from which Belle will receive rental income. The reorganization is expected to be completed on or about August 2014.

Takeaway: Belle is a conglomerate and given the highly regulated nature of the gaming business, this separation makes sense.

CZR – Harrah's Tunica will close its doors today.

Takeaway: Tough market

FB – promoted Tarquin Henderson, head of gaming sales for Europe and MEA, to head up the company's real-money gambling project following the departure of former head Will Collins, who departed to start his own gaming consultancy firm.

Takeaway: Online gaming revenues may not be living up to expectations and early forecasts for FB?

BEE – closed on a $120 million limited recourse loan secured by the Loews Santa Monica Beach Hotel. The financing replaces the $108 million loan previously placed on the property. The loan carries a floating interest rates of LIBOR plus 225 bps and has an initial three-year term with four, one-year extension options pending certain financial and other conditions. Wells Fargo Bank originated the loan.

Takeaway: As expected but a modestly larger loan amount.

Equity Inns – American Realty Capital Hospitality Trust (a $2 billion non-traded REIT) announced it entered into an agreement to acquire the Equity Inns lodging portfolio of 126 hotels totaling 14,934 rooms across 35 states for $1.925 billion from subsidiaries of W2007 Grace I, LLC and WNT Holdings LLC - both of which are indirectly owned by one or more Goldman Sachs Whitehall Real Estate Funds.

Takeaway: Whitehall made a sizable return for its shareholders. Industry veterans will recall Whitehall announced its intention to acquire ENN in June 2007 for $1.27 billion – $23 a share in cash, 19% premium to the previous day's share price and closed on the acquisition on October 26, 2007. At the time, Equity Inns owned 132 limited-service hotels covering 15,700 rooms.

HLT – announced the launch of Curio - A Collection by Hilton. Curio - A Collection by Hilton (curiocollection.com) is a global collection of distinctive hotels. Letters of intent have been signed for the following properties: SLS Las Vegas Hotel & Casino; The Sam Houston Hotel in Houston, Texas; Hotel Alex Johnson in Rapid City, S.D.; The Franklin Hotel in Chapel Hill, N.C.; and a soon to be named hotel development in downtown Portland, Ore.

Takeaway: Everyone is in the boutique business.

RCL - (Travel Weekly) Celebrity Cruises will pay commission on what is typically invoiced as noncommissionable cruise fare (NCF) on some cruises sold in June by travel agents in North America. The extra commission applies to 2015 sailings, if agents book veranda cabins and above. NCFs can account to 10-15% of the total cruise price. Dondra Ritzenthaler, Celebrity's senior VP of Sales said that 2015 bookings were not notably behind or in need of a boost. “It’s a 30 day way to say thank you to all of our travel partners who have really supported us through all of our promotions,” she said.

Takeaway: This short-term promotion could give an early boost for Celebrity 2015 bookings, particularly on the heels of the success of its 123Go! program.

NCLH - Hawaii's Visitor Spending and Arrivals Continue to Dip (Travel Agent Central)

Fewer visitors came by cruise ships (-22.2% YoY) and that led to a slight drop in total arrivals to Hawaii (-0.7%) at 662,553 visitors. The dip in cruise passengers can be attributed to poor access to Hawaii’s harbors, says Mike McCartney, president and CEO of the Hawaii Tourism Authority. “We recently issued a request for proposals for maritime vessel scheduling software, which will help to establish an integrated system that will ease vessel scheduling to optimize the use of dock space to accommodate more cruise ships throughout the Hawaiian Islands...Visitor arrivals and expenditures will continue to plateau in 2014, in comparison to the past two record-breaking years," added McCartney.

Takeaway: Could the slowdown in this expensive tourist destination continue? Hawaii cruise pricing has been dipping as well. NCLH itineraries have 7% exposure in 2014.

Insider Transactions:

RCL – EVP Harri U. Kulovaara sold 41,985 shares of the stock on Thursday, May 29th at an average price of $54.60, and he now directly owns 32,905 shares.

SHO – CFO Bryan Giglia sold 15,763 shares of stock on Thursday, May 29th at an average price of $14.61, and he now directly owns 115,449 shares.

Takeaway: More insider selling in the Cruise and Lodging sectors. Buying seems to be on Gaming side.

INDUSTRY NEWS

Japan Gaming Expansion – late on Friday, Japanese Prime Minister Shinzo Abe who had remained silent on the issue of casinos, gave a strong endorsement to legislation that would legalize casino gambling in Japan. Abe visited both RWS and MBS during his recent trip to Singapore. The initial gaming legislation is expected to pass the Diet this fall, at which time, legislation and debate will move on to a second bill concerning concrete regulations, which proponents hope can be passed in 2016. Allowing for three years of construction prior to the 2020 Tokyo Summer Olympics which open on July 24, 2020 and close on August 9, 2020.

Takeaway: We're hearing as long as Abe remains in power, casino legislation will happen. There is more than sufficient time to approve the required two-step legislation as well as complete construction prior to the opening of the 2020 Tokyo Summer Olympics.

Zhuhai-Macau-Hong Kong Bridge – The Infrastructure Development Office conceded that it had encountered a serious delay in the reclamation work of urban Zone A just across the waters from Areia Preta, which is a major public infrastructure project linking Macau to the Hong Kong-Zhuhai-Macau Bridge. Zone A, the biggest of the five reclaimed zones, is located across the waters from Areia Preta – the northeastern district of the Macau Peninsula. The 138-hectare zone is to be linked to the Zhuhai-Macau artificial island to its east, where the Hong Kong-Zhuhai-Macau Bridge will land. The bridge is expected to be in use by 2016

Takeaway: More infrastructure project delays

Pennsylvania Online Poker Legislation – Pennsylvania State Senator Edwin Erickson announced his intention to formally introduce State Bill 1386 (legislation that would authorize Interactive Gaming in the form of online poker). Gross gaming revenue would be taxed at 14% – less than New Jersey but higher than Nevada.

Takeaway: More support for our contention that legal online gaming will ultimately take the place of interstate online poker.

MACRO

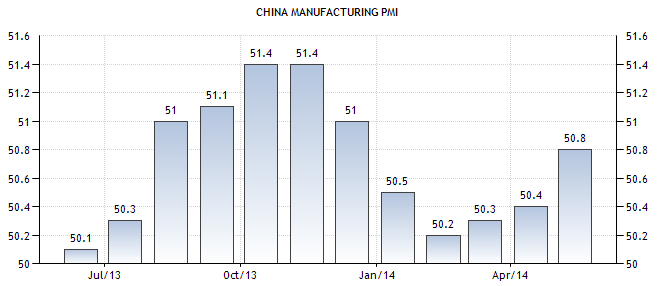

China Economic Growth - China Manufacturing PMI rises in May to 50.8 versus expectations of 50.7, up from 50.4 in April and February's low of 50.2

Hedgeye remains negative on consumer spending and believes in more inflation. Following a great call on rising housing prices, the Hedgeye

Macro/Financials team is turning decidedly less positive.

Takeaway: We’ve found housing prices to be the single most significant factor in driving gaming revenues over the past 20 years in virtually all gaming markets across the US.