Note summary

- PUSHBACK vs. REALITY: Management and the sell-side are trying to push back on our thesis. Below is a summary of what we've heard, and our response with incremental data and analysis addressing each counterpoint. Please let us know what other pushback your're hearing so we can address that as well.

-

SUPPORTING CHARTS & ANALYSIS: The initial version of this note was too long, so we cropped it, attempting to keep it text-light and chart-heavy. Happy to send over additional analysis or discuss in more detail.

-

THE ONE QUESTION THAT MATTERS: The only way management can settle the debate is by answering one question: "What percentage of your current customers have been advertising and/or generating revenue for YELP for more than a year?" Everything else is just noise.

PUSHBACK vs. Reality

Not surprisingly, management and the sell-side pushing back on our thesis; mostly through attacking the messenger, rather than the thesis itself (i.e. ad hominem). Below is a summary response to each attempted rebuttal, with supporting details in the next section.

- CAN'T CALCULATE ATTRITION RATE?: from the customer repeat rate. This is all about the language. When management says this, they are referring to calculating the annual rate from the quarterly customer repeat rate, they're not saying that we can't calculate the quarterly rate, nor does it address absolute levels of attrition.

- EFFECTIVE SALESFORCE? The pushback is that if YELP is having heightened attrition issues, it must have a very effective salesforce to compensate. The reality is the exact opposite. YELP's salesforce has been growing ~50% y/y each of at least the last 8 quarters. We estimate that its salesforce would be wildly unproductive if YELP wasn't having these attrition issues (i.e. unprofitable).

- COHORT GROWTH TOO STRONG: The pushback is that the strong growth in its early cohorts wouldn't be possible if YELP was having heightened attrition issues. The reality is that ~50% of US Businesses reside in these cohorts, and YELP was very slow to penetrate these cohorts in terms of both Claimed & Active Businesses.

- OTHER SERVICES SKEWING METRICS: The pushback is that customer repeat rate could be distorted in any one period from accounts intermittently deploying deals & gift certificates. The reality is that argument doesn't consider customer overlap. Regardless, quarterly fluctuations across less than 5% of its revenues don't matter; especially since its attrition issues are a recurring quarterly theme.

SUPPORTING CHARTS & ANALYSIS

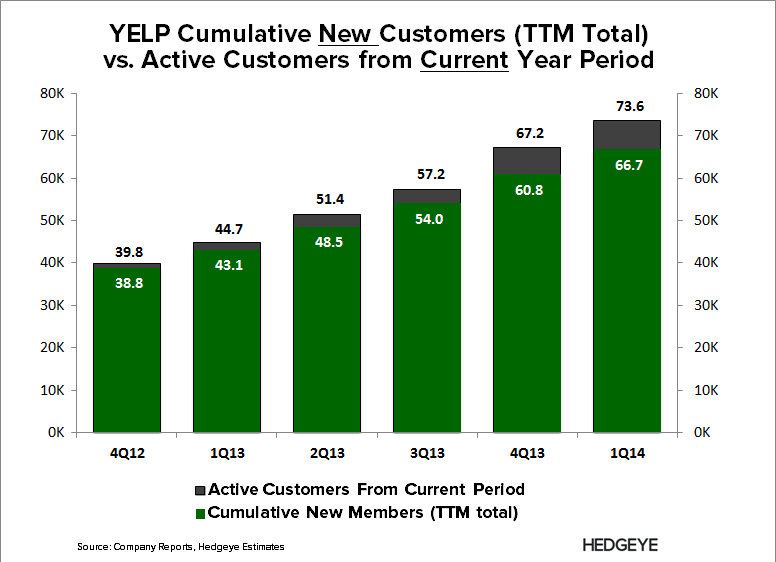

Can't Calculate Attrition Rates?: There is no debating the quarterly attrition rates, or the magnitude of new and lost accounts. We can't calculate the exact annual rate, but that is function of the source of those lost accounts (prior vs. new customers), not whether YELP is actually losing them. Most advertising customers sign annual contracts, meaning most of its new business can't be lost within a year (without paying 2-3 month penalty). So the bulk of those lost accounts are coming from existing accounts signed before the most recent LTM period. Comparing cumulative lost accounts to prior-year period accounts, and cumulative new accounts to current period accounts, tells the story.

<chart14>

Effective Salesforce: The chart below measures New Revenue/Rep:

(New Accounts x YELP stated ARPU)/Trailing Sales Reps. The Reps are lagged on a 9-month basis (so any hires during the quarter or in the 6 months prior are assumed to generate no revenue). The difference in the two metrics below is our calculation for new revenue vs. what is implied by account growth in YELP's reported metrics; the latter suggests its salesforce isn't generating enough new business to cover their own salaries (note: this is base only, not inclusive of ancillary employment costs).

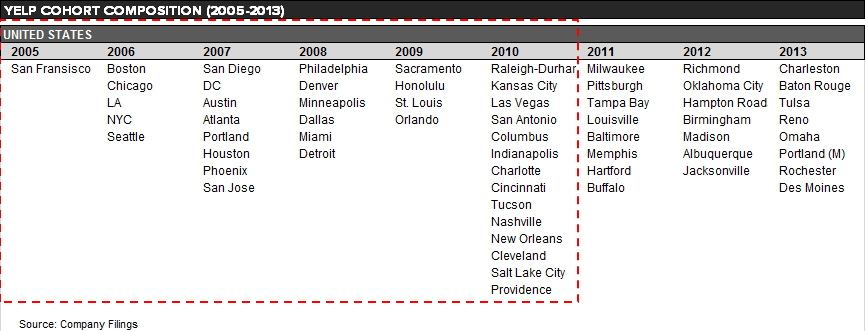

Cohort Growth: YELP had been slow to penetrate this segment, with only ~300 claimed businesses at the end of 2010 out of the total pool of at least 1.9M potential businesses in these cohorts. In short, most of the early cohort wasn't even on YELP by the end of 2010. Cohort growth remains strong because YELP didn't meaningfully penetrate this group until it started ramping its salesforce. Since 50% of US businesses reside in these early cohorts, we expect YELP will see decelerating growth in the later cohorts first given that included markets are relatively smaller.

Other Services Skewing Results: The pushback doesn't assume customer overlap between Local Advertising and Other Services (e.g. a customer could could stop offering a deal, but still advertise with YELP). Even if there weren't any overlap, Deals/Gift Certificates are less than 5% of revenue, so how much of an impact could these fluctuations in these services make on the overall quarterly attrition trend? Regardless, the attrition trend is too consistent for this argument to hold any water.

THE ONLY QUESTION THAT MATTERS

"What percentage of your current customers have been advertising and/or generating revenue for YELP for more than a year"

Answering this question will settle the debate, and is the only way that management can refute our analysis, or make any claims that it is not experiencing heightened attrition.

This question is basically a derivative of its customer repeat rate metric, so the only reason management would avoid the question is if they have something to hide.

We asked YELP's CFO this question, and didn't get an answer: YELP: Chat with the CFO (Recap). So if you have a line into management, see what they say. If you happen to get a number or a ballpark figure, let us know, and we'll let you know if the math makes sense.

The key to answer the answering this question will come from YELP's customers, not management. In this regard, stay tuned.

RISK TO OUR CALL

In light of M&A activity heating up, this remains the key risk to our call. A recent rumor suggests a major player is looking at YELP. While possible, we think it unlikely once the potential acquirer gets a look at their financials.

FINAL THOUGHT

Management and the sell-side will try to spin the story any way they can to avoid addressing the core issues. Collectively, we haven't heard anything remotely close to a credible rebuttal to our thesis. But please, let us know what other pushback you're hearing so we can address that too. Truth be told, we're having some fun with this.

Hesham Shaaban, CFA

@HedgeyeInternet