The Hedgeye Restaurants team posted a note earlier today on the impact of M&A deals between Hillshire Brands' (HSH), Pilgrim's Pride (PPC), and Pinnacle Foods (PF), which we've included below as it relates to the food industry.

---

BOBE: M&A Activity Heating Up in the Food Business

Following Hillshire Brands’ (HSH) recent agreement to acquire Pinnacle Foods (PF) for about $4.3 billion, Pilgrim’s Pride (PPC) announced its proposal this morning to acquire HSH for $45.00 in cash. The transaction, which is valued at $6.4 billion, places a 25% premium on the volume weighted average price of HSH shares over the 10 trading days following the announcement of the PF transaction. In the deal, PPC would pay 12.5x TTM EBITDA for HSH. According to the release, the proposal has the “unanimous support” of both Pilgrim’s and JBS SA’s Board of Directors. PPC will finance the acquisition with a mix of existing cash and new debt financing.

Merging with HSH will allow PPC to expand its business in branded foods, an area that only makes up 20% of PPC’s current sales. According to the release, the goal of the transaction is to create “a leading branded, protein-focused company with strong, consistent earnings and complementary competencies.” HSH’s current brand portfolio consists of leading brands in core categories, including Jimmy Dean, Hillshire Farm, Ball Park, State Fair, Aidells and others.

This deal was of particular interest to us because it highlights the surging demand for packaged and prepared foods companies. This ties directly into our Long BOBE Best Idea thesis, which calls for the spinoff or sale of BEF Foods that activist Sandell Asset Management first suggested.

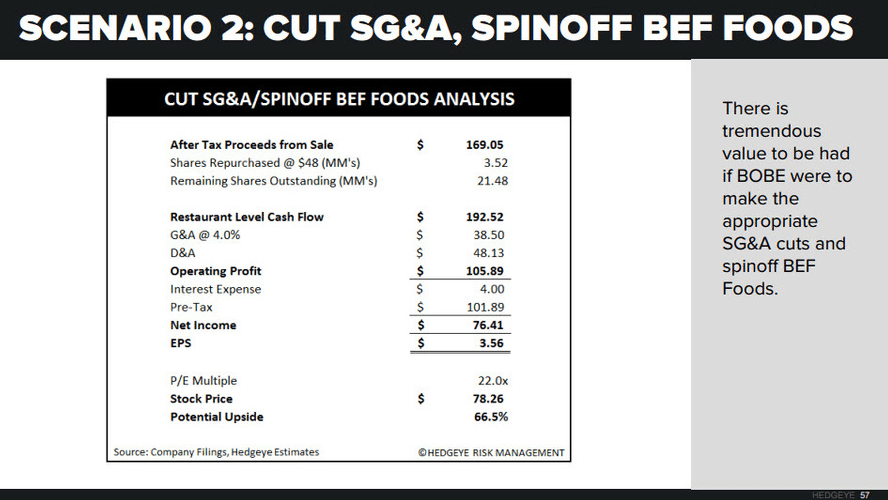

In the case of BOBE, we see tremendous upside value in separating the foods business from the restaurant business and believe the company could spinoff BEF Foods at a substantial premium to its current value.

The food processing business is linked to the founding of the company and, to be clear, we fully appreciate the desire to maintain tradition within a business. With that being said, we believe this connection is severely limiting the potential of the company. Other than the historic connection between BEF Foods and Bob Evans Restaurants, there are very few, if any, synergies between the businesses. We believe each business would benefit greatly from laser-focused, uncompromised operating strategies. A separation would allow BOBE to focus on efficiently running its restaurants, while enabling BEF Foods to increase sales in the foodservice industry and further diversify its customer base. As a separate entity, we believe BEF Foods would have an enormous runway for growth.

We maintain that such a transaction, in conjunction with significant SG&A cuts at BOBE, would result in substantial shareholder value creation for shareholders.

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst