HEDGEYETV

Jim Lacamp, portfolio manager at Macroportfolio Advisors at UBS, discusses the Fed, U.S. economy, and how Keynesian economics is leading the U.S. down the Road to Perdition with Hedgeye CEO Keith McCullough.

Here's the question-and-answer portion from our daily institutional Morning Call hosted by Hedgeye CEO Keith McCullough and Senior Macro Analyst Darius Dale. Keith answers questions on markets, hedge fund performance and even youth hockey.

Hedgeye CEO Keith McCullough walks us through what the markets are telling us about growth, inflation, yield spreads and more.

CARTOONS

Click here to subscribe to Cartoon of the Day.

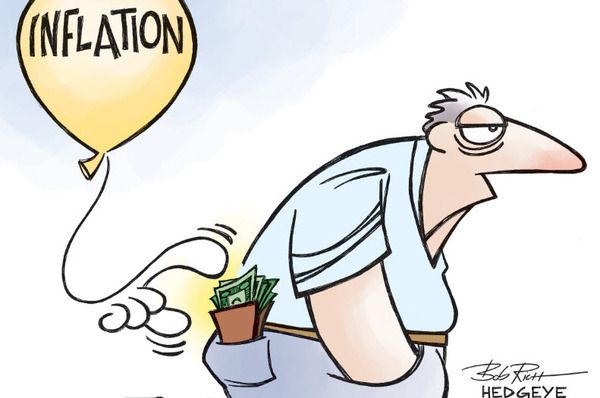

While lies about inflation in Washington can most definitely live, they can’t live forever.

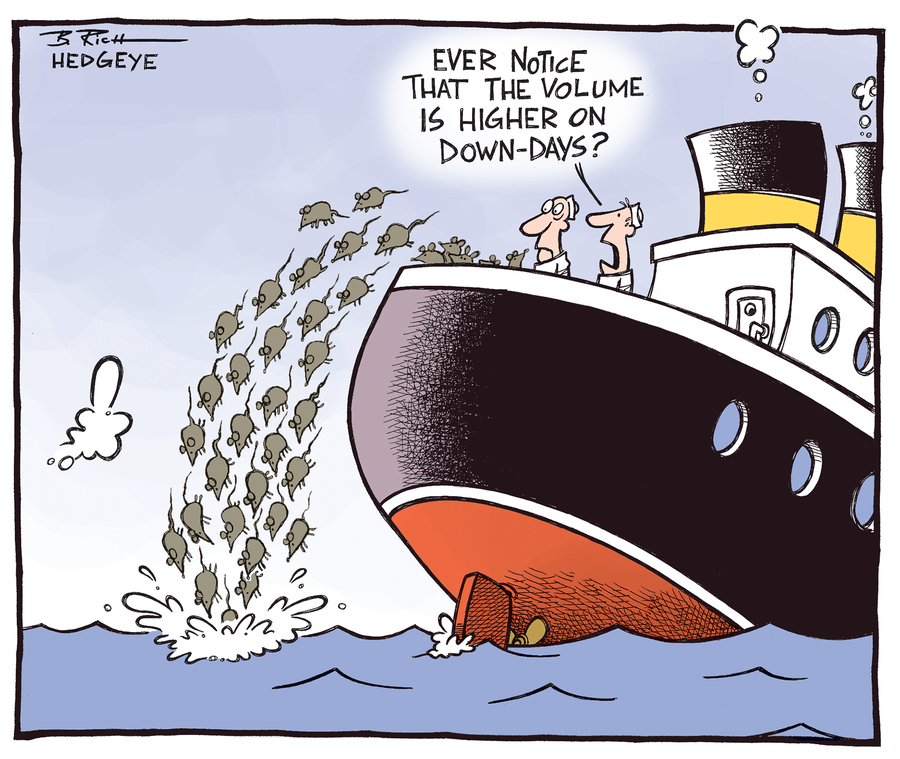

We’ve been hitting you with this DOWN-volume-UP-day thing square in the head this year.

CHART

POLL

Oil prices are surging – meaning higher prices at the pump – just in time for Memorial Day weekend when Americans are being taxed six-ways to Sunday from rent to food. It’s just another sign of#InflationAccelerating. So while every car-owning American who fills up the tank may be feeling the pinch, we wanted to know how it’s affecting your holiday. Click here to view the poll and results.

HEDGEYE.COM

10 More Signs of #InflationAccelerating

US rents (34% of Americans have to rent, and like it) and the cost of living hit all-time highs this week, so alongside #RentRipping, here’s more year-to-date #InflationAcclerating data. Click here to continue reading.

Hedgeye Energy: Why $BPT Is A One Dollar Bill Selling For Two

I'll pay you $1 per year for the next 8 years. The payments are not guaranteed, they have equity-like risk. How much would you pay me today for this deal? A BPT long would give me $10. Click here for more.

Mortgage Demand Falls Again This Week

Wednesday’s MBA mortgage purchase application data shows housing demand dropped for a second week in a row in spite of falling rates. Click here to read more.

Hedgeye Retail: Target Execs Should Be Afraid For Their Jobs | $TGT

Normally we wouldn't characterize the opinion of one disgruntled employee as indicative of the corporate culture, but the fact that Target's CMO, Jeff Jones, personally addressed the anonymous letter in public is telling. Click here to continue reading.