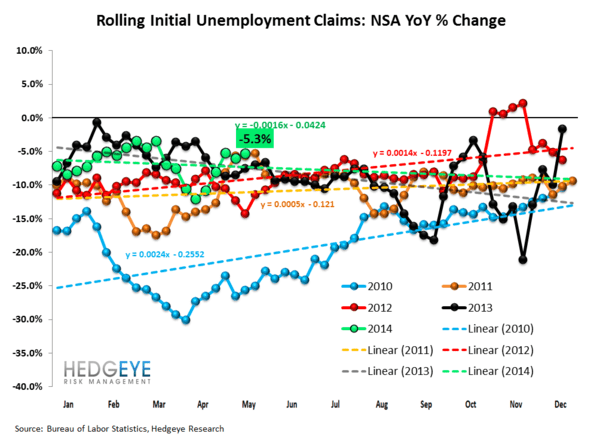

Headline claims rose +28K WoW to +326K while the rate of improvement in non-seasonally adjusted initial claims, our preferred read on the underlying trend in the labor market, decelerated to -5.5% YoY vs. -15.8% last week. The 4-wk rolling average in YoY NSA claims decelerated -80bps sequentially to -5.3% YoY.

In short, another week of decent (not outstanding) improvement as we continue to steadily track towards the frictional lower bound at ~300K in seasonally adjusted initial claims.

Josh Steiner, our head of financials research, characterized this morning’s claims data like this:

This morning's claims data isn't as bad as it looks, but it's not great either. The previous week was anomalous in its strength, whereas this week is more or less in line with the steady trendline rate of improvement we've been seeing for a while now. The important takeaway is this. The labor market remains strong enough for the Fed to push forward with its taper.

Source: Hedgeye Financials

The “strong enough” initial claims characterization sits as a sufficient microcosm for the broader domestic macro data as well.

Sequentially, the data is generally better but the reported March-May data certainly doesn’t reflect significant deferred 1Q (weather) demand or signal a return to the slope of growth observed over 1Q-3Q13 period last year.

Still, sequential improvement supports the wait-&-see/steady-as-she-goes policy approach promulgated by the fed again yesterday– at least over the nearer term.

With the 10Y and $USD both in bearish formation, the bond and currency markets continue to price in slowing growth. On the fundamental side, housing continues (& will continue) to slow (see today’s note: Biggest MoM Growth in Inventory...Ever) and the conflation of decelerating wage growth, a troughed savings rate and rising inflation continue to constrain any upside for “non-core” consumption growth. And from a comp perspective, growth comparisons get harder while inflation comps ease through the third quarter of this year.

More broadly, looking at growth and inflation expectations across our Global Macro dashboard (click on it for an expanded view) developed market growth estimates continue to rise while EM growth revisions remain negative. Interesting, funds continue to flow in the opposite direction of revision trends (ie. into EM markets & away from domestic/DM markets) – a phenomenon largely linked to persistent weakness in the dollar, in our view.

On the inflation side, expectations for ongoing disinflation remain the prevailing trend. Notably, the U.S. sits as one of the only developed market economies (alongside Canada) where inflation expectations have been rising.

Absent technical factors driving a material supply/demand imbalance for credit, rising inflation expectations + falling (nominal) bond yields = lower real growth expectations. We think that remains the right call for the immediate/intermediate term.

Christian B. Drake

@HedgeyeUSA