Not Too Hot, Not Too Cold ... Just Right for More Tapering

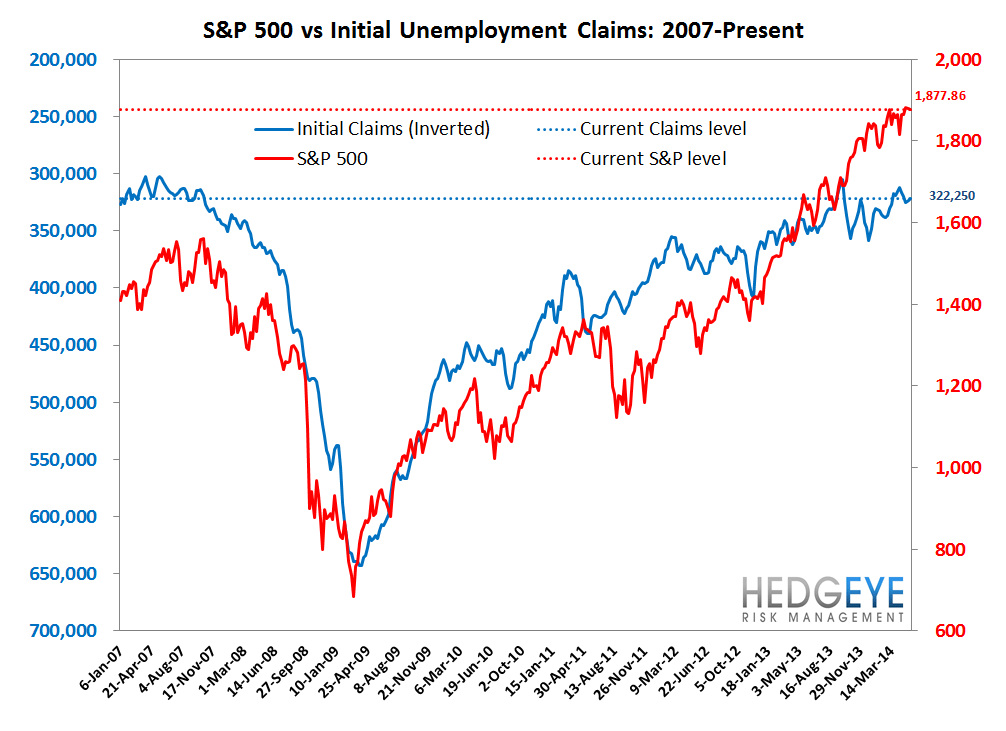

This morning's claims data isn't as bad as it looks, but it's not great either. The previous week was anomalous in its strength, whereas this week is more or less in line with the steady trendline rate of improvement we've been seeing for a while now.

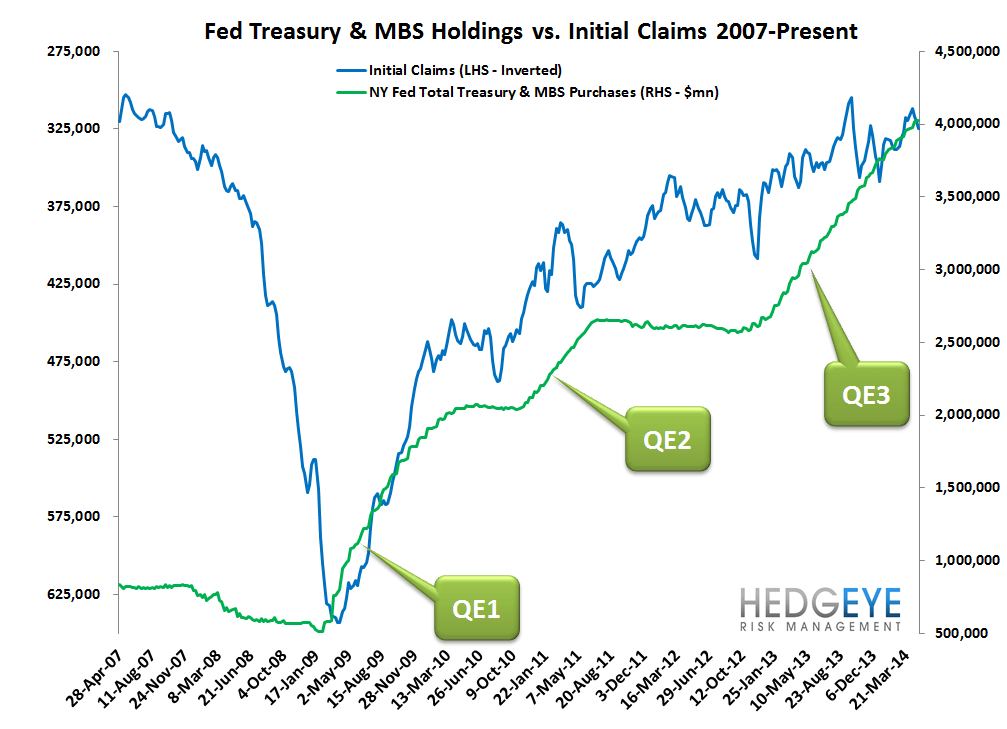

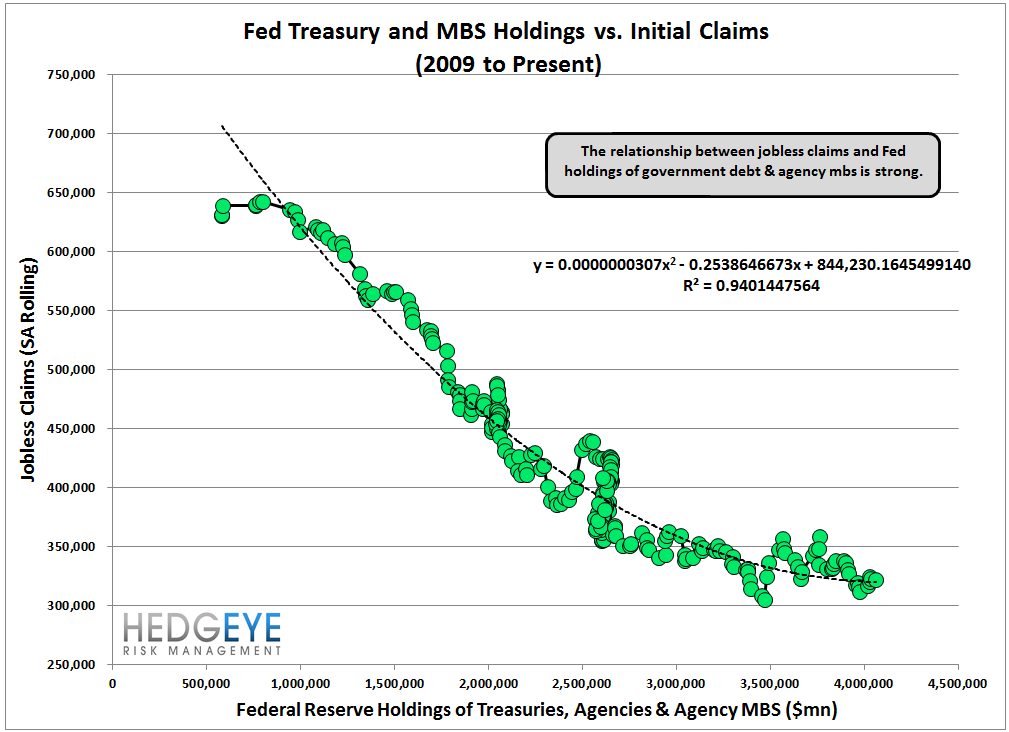

The important takeaway is this. The labor market remains strong enough for the Fed to push forward with its taper. The taper is pushing long-term rates lower (counterintuitive, we realize .... for more on why, see our note from May 6 entitled "Tapering = Rates Falling"). This means more tough sledding for Financials positively correlated to long-term rates such as banks (R = +0.62), Life Insurers (R = +0.75) and Online Brokers (R = 0.67). Conversely, negatively correlated Financials include the agency mortgage REITs like NLY, MFA (R = -0.90) and select bond fund managers (i.e. AB, where R = -0.45). Squaring these values will tell you the magnitude of the headwind you're fighting being long. Yield plays also do well amid falling rates so our recent Best Idea addition, OZM, should fare well alongside our traditional fixed income asset manager idea LM.

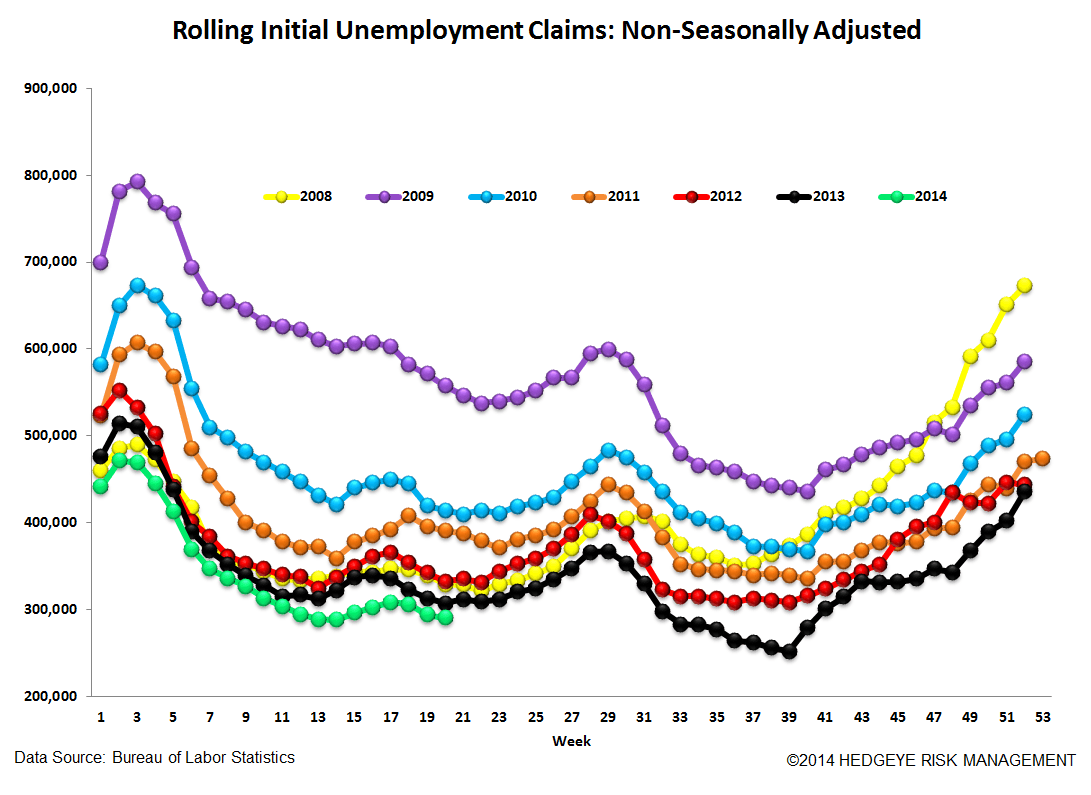

The Data

Prior to revision, initial jobless claims rose 29k to 326k from 297k WoW, as the prior week's number was revised up by 1k to 298k.

The headline (unrevised) number shows claims were higher by 28k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -1k WoW to 322.25k.

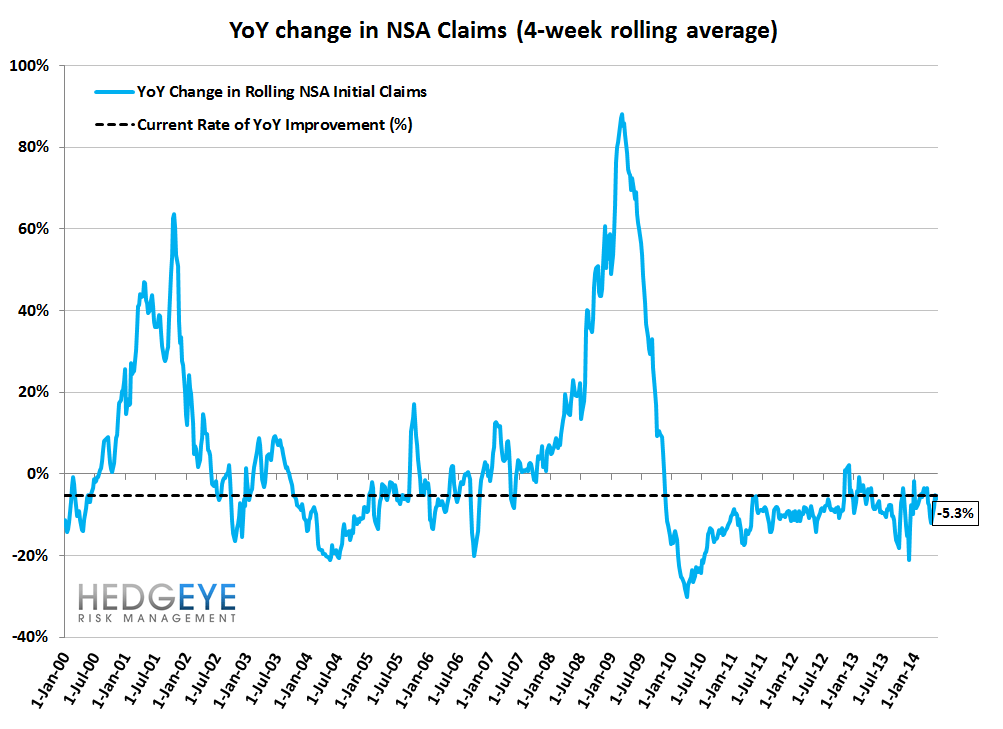

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -5.3% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -6.1%

Yield Spreads

The 2-10 spread rose 2 basis points WoW to 220 bps. 2Q14TD, the 2-10 spread is averaging 225 bps, which is lower by -14 bps relative to 1Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT