Below are Hedgeye analysts' latest updates on our EIGHT current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

We also feature three research notes from earlier this week which offer valuable insight into the market and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

GLD – We added Gold to Investing Ideas this past week. Click here to read the full report.

HCA – Hedgeye Healthcare sector head Tom Tobin remains bullish on HCA Holdings, but has no new updates this week.

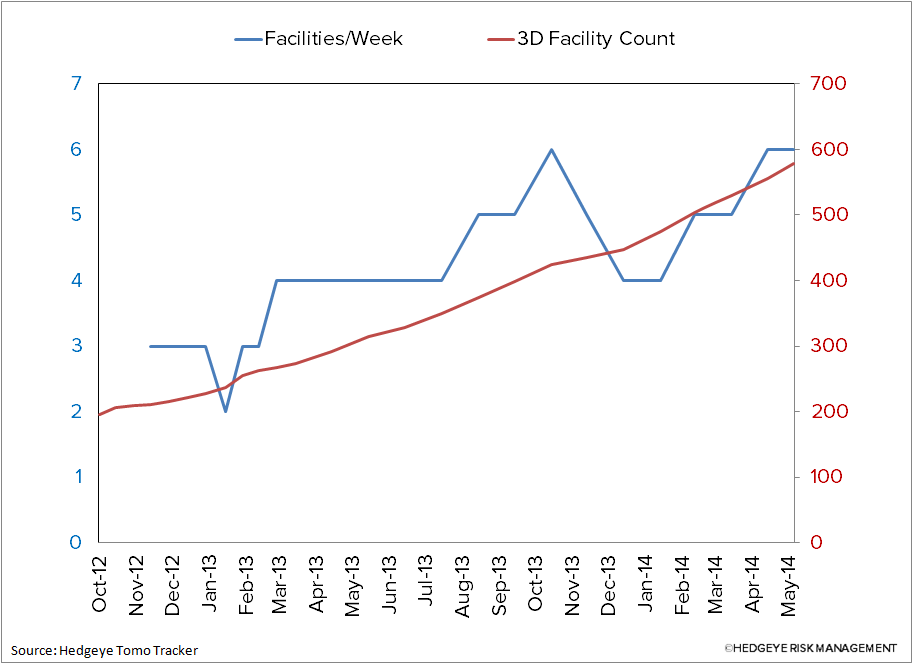

HOLX – We’re continuing to see a nice acceleration in facility conversions to 3D Tomosynthesis in our data. The chart below shows the result from the update we ran earlier this morning. Facility counts and the placement rate continue to climb. The pace needs to pick up next month, however to hit our near term estimates, although the announcement of a reimbursement code should help if we’re right on what we think the agency does. Next week we are hosting a call with a leading expert in the field. He has one of the most detailed perspectives on what CMS will decide for a reimbursement for 3D Tomosynthesis.

LM – Our weekly tracking of mutual funds flows from the Investment Company Institute remained defensive this week with the combination of taxable and tax-free bond funds having another strong week of production with $3.9 billion in inflow, well above the running year-to-date average for 2014 of $2.1 billion per week. Conversely, equity funds had only the third net outflow of the year with $1.0 billion leaving all equity mutual funds, well below the year-to-date average of a $3.1 billion inflow. This emerging defensive posture by investors is very favorable for Legg Mason with 55% of its assets-under-management in bonds, the largest exposure in the traditional asset manager group.

LO – Once again rumors swirled this week that Lorillard is going to get taken out. We think the market is getting over its ski tips on an imminent timetable for a deal given acquisition challenges.

We maintain our Best Idea Long Call Lorillard (presented on March 4 of this year). We think investors are best served to ride out the rumor mill pushing the stock higher as we don’t expect an imminent deal, and maintain that LO is fairly valued as a stand-alone or takeout target at $80/share (more below).

We view a hypothetical deal (especially an imminent one) between RAI and LO as challenged on three main factors:

- Our main flag is that a combined RAI + LO would own ~ 67% of U.S. menthol market, which we believe should trigger anti-trust flags.

- Big tobacco is already a highly concentrated industry in the U.S. across the big three – MO has a leading ~51% of market share; a combined RAI + LO would equate to ~ 42% share.

- BAT may look to maintain or increase its ownership in RAI (for the remaining 58%), however it cannot act until July of this year when a 10-year standstill agreement between it and RAI expires.

A scenario suggests that RAI could look to divest such menthol brands as Kool, Winston and Salem (~5% total market share), which could serve to change the consideration of the FTC/DOJ, however all of this shopping would take time.

As part of the Best Idea’s thesis we did not consider a RAI + LO deal. We think the decision to replace CEO Daan Delen with Susan Cameron, who held the CEO seat for 7 years ending in 2011, is contributing fuel to the speculation that she wants to come out of the box “strong” with this deal.

Our thesis is built on the superior fundamentals of the Lorillard portfolio:

- We do not see Menthol Regulation Risk from the FDA over the medium term (1-2 years) and assign less than a 20% probability over the long term.

- We expect blu e-cigs to benefit from first mover advantage and maintain leading market share despite competitive pressures from Big Tobacco’s entry into the category. Looking out 5 years to 2018, we model blu’s earnings contributing 31% to total LO, and accelerating earnings growth in the combined company.

- We expect strong and stable menthol fundamentals driven by lasting consumer and demographic trends that differ from traditional tobacco.

We maintain a fair value $80/share target would equate to a price 30% higher than today’s, so we think it pays to hold on to LO amidst the rumor winds!

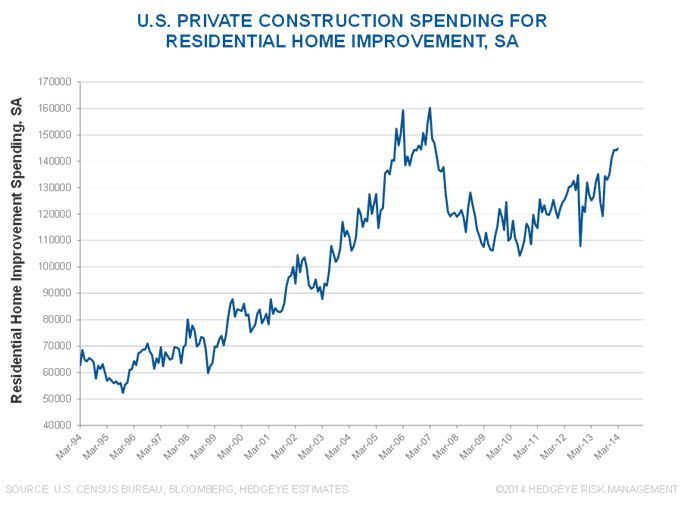

OC – While the US residential housing market appears to be softening, residential home improvement spending continues to rebound from its post financial crisis lows. Owens Corning should benefit from tightening building codes and improved competitive dynamics in coming years. Shorter-term, we suspect that the company may benefit from a bounce-back in activity from earlier weather-related weakness.

RH – William’s Sonoma (WSM) reported earnings on Wednesday (5/22) after the close and the company reported a 10.0% consolidated comp – 85% above consensus estimates. More importantly, WSM’s two flagship furniture banners, Pottery Barn and West Elm, posted 9.7% and 18.8% comps respectively.

We view the event as a ‘State of the Union’ on the high-income consumer. There has been some trepidation surrounding the US consumer, much of it warranted in light of the less than positive 1Q earnings season to date. But, the concepts skewed towards the high-income subset have been resilient, i.e. KATE, TIF, and WSM. This gives us stronger conviction in our 1Q Restoration Hardware estimates which call for a 15% retail comp compared to the street at 10%.

ZQK – Quiksilver had a 9% rally over two days for one reason and one reason only – the company announced its quarterly reporting date of June 2. The company has had a wall of silence since the second quarter ended last month and gave zero indication to the Street as to when it would release earnings. That might be acceptable for a $10bn market cap company that actually earns money, but in this market it is certainly not acceptable for a company like ZQK. This is a company that has to be massively shareholder-friendly – and the fact is that it is not. It has to seriously upgrade its investor relations/communication program. Most notably, the Street perceives the announcement as an indication by ZQK that it will not tank the quarter. Presumably, if the company were to preannounce, it would have done so alongside the announcement of its earnings date. We still think that ZQK is just emerging from its darkest hour. After 1.5 years of a new management team making all the tough decisions, we should start to see margin improvement and top line growth in 2H. As we’ve stated all along, we think it will be acquired at a double digit price sometime over 24 months.

* * * * * * *

Click on each title below to unlock the institutional content.

Internet & Media analyst Hesham Shaaban had an honest and forthcoming conversation with YELP CFO Rob Krolik but is reiterating the short.

LINN Makes 1st Permian Trade & Nothing Changes

Energy analyst Kevin Kaiser analyzes LINN Energy and ExxonMobil's announcement of an asset swap.

Restaurants sector head Howard Penney explains why he is still stunned by the sheer arrogance of Darden management.