TODAY’S S&P 500 SET-UP – May 22, 2014

As we look at today's setup for the S&P 500, the range is 32 points or 1.22% downside to 1865 and 0.48% upside to 1897.

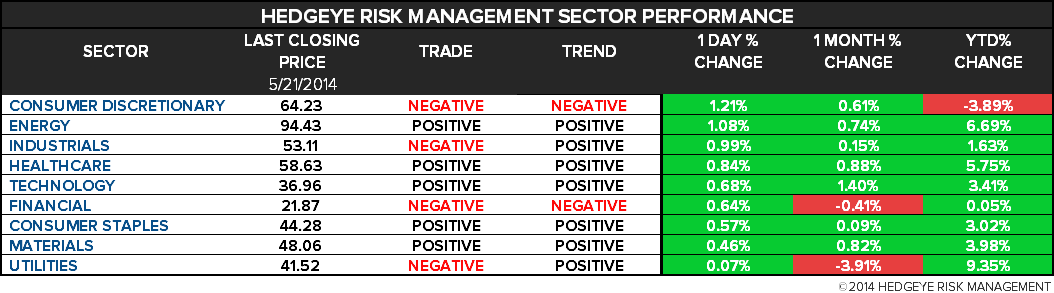

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.20 from 2.19

- VIX closed at 11.91 1 day percent change of -8.10%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed National Activity Index, April est. 0.0 (prior 0.2)

- 8:30am: Initial Jobless Claims, May 17, est. 310k (prior 297k)

- Continuing Claims, May 10, est. 2.675m (prior 2.667m)

- 9:45am: Bloomberg Economic Expectations, May (prior 48)

- 9:45am: Markit US Manufacturing PMI, May prelim est. 55.5 (prior 55.4)

- 10am: Existing Home Sales, April, est. 4.69m (prior 4.59m)

- 10am: Index of Leading Economic Indicators, April, est. 0.4% (prior 0.8%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Kansas City May Fed Manufact. Index, est. 7 (prior 7)

- 4pm: Fed’s Williams speaks in San Francisco

GOVERNMENT:

- President Obama speaks on tourism at Baseball Hall of Fame, travels to Chicago for DSCC events

- 8am: SEC Chair Mary Jo White at Investment Co. Institute

- 9:45am: House Financial Svcs Cmte resumes May 7 small cap., emerging growth co. legislation, community banks

- 10am: U.S. Chamber of Commerce conf. call on SEC’s Pay Ratio Rule

- 10:45am: House Minority Leader Pelosi holds press conference

- 11:30am: House Speaker Boehner holds news conference

WHAT TO WATCH:

- BofA said to abandon market-making unit amid industry scrutiny

- Vivendi selling Activision stake worth ~$850m

- China manufacturing gauge rises in stabilization sign

- JD.com raises $1.78b, pricing IPO above offer range

- Mastercard declined Sberbank offer to buy Maestro brand: IFX

- Reynolds in advanced talks to buy Lorillard, Reuters says

- Weibo loss more than doubles on rising costs to add users

- China to review security of IT products, suppliers: Xinhua

- Unilever to sell sauce brands to Mizkan for $2.15b

- Russia says troops near Ukraine to return to base by June 1

- Euro-area services surge helps recovery as factories cool

- U.S. sends troops to Chad to hunt for kidnapped Nigerian girls

- EU 4-day parliament elections begin in U.K., Netherlands

- Germany wants to question Facebook, Google CEOs on NSA: Welt

AM EARNS:

- Best Buy Co. (BBY) 7am, $0.19 - Preview

- Buckle (BKE) 7am, $0.78

- Dollar Tree (DLTR) 7:31am, $0.66

- GameStop (GME) 8:30am, $0.57

- Movado Group (MOV) 7am, $0.32

- Nordson (NDSN) 7am, $0.89

- Patterson Cos (PDCO) 7am, $0.66

- Perry Ellis International (PERY) 7am, $0.27

- Royal Bank of Canada (RY CN) 6am, C$1.43 - Preview

- Sears Holdings (SHLD) 6am, ($1.91)

- Toro Co. (TTC) 8:30am, $1.48

- Toronto-Dominion Bank (TD CN) 6:30am, C$1.02

PM EARNS:

- Aeropostale (ARO) 4:01pm, ($0.72) - Preview

- Aruba Networks (ARUN) 4:05pm, $0.20

- Brocade Communications Systems (BRCD) 4pm,$0.18

- Compuware (CPWR) 4:05pm, $0.08

- DryShips (DRYS) 4:05pm, $0.004

- Fresh Market (TFM) 4:02pm, $0.43

- Gap/The (GPS) 4pm, $0.57

- Hewlett-Packard Co (HPQ) 4:04pm, $0.88 - Preview

- Marvell Technology Group (MRVL) 4:05pm, $0.22

- Mentor Graphics (MENT) 4:05pm, $0.06

- Ross Stores (ROST) 4pm,$1.15 - Preview

- TiVo (TIVO) 4:01pm, $0.06

- Youku Tudou (YOKU) 4:30pm, ($1.11)

- Zumiez (ZUMZ) 4pm, $0.05

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Soybeans Advance to 11-Month High as China Demand Seen Rising

- Brent Trades Near 11-Week High on China Factory Data; WTI Steady

- China’s Bauxite Loss Spurs Export Boom in Australia: Commodities

- Copper Rises as China Factory Gauge Adds to World Demand Outlook

- Gold Trades Above One-Week Low as Palladium Near 33-Month High

- Arabica Drops to 7-Week Low on Ample Supplies; Cocoa Advances

- Steel Rebar Climbs for Second Day on Iron Ore Price, China PMI

- Russia-China Deal Seen Damping LNG Prices Amid Rising Output

- Gold Imports by India Seen Advancing as RBI Relaxes Some Curbs

- Mexico Crude Needs New Markets as U.S. Exports Surge, Citi Says

- Aluminum Market Focuses on Surplus, Premiums: Outlook

- Gold-Palladium Ratio at 10-Year Low on Supply: Chart of the Day

- U.S. Crude Oil, Like Horses, Banned From Being Exported Overseas

- Gazprom Bulls’ China Fixation Is Misguided to Top Moscow Broker

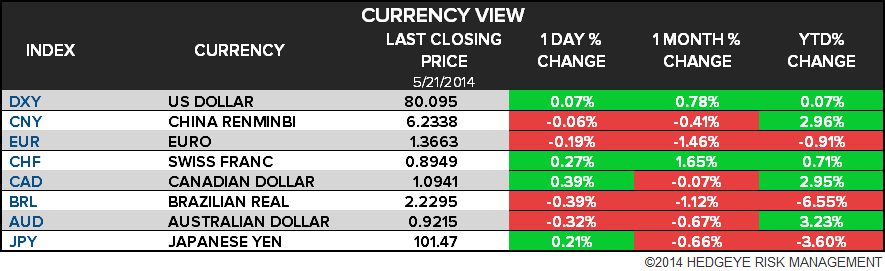

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

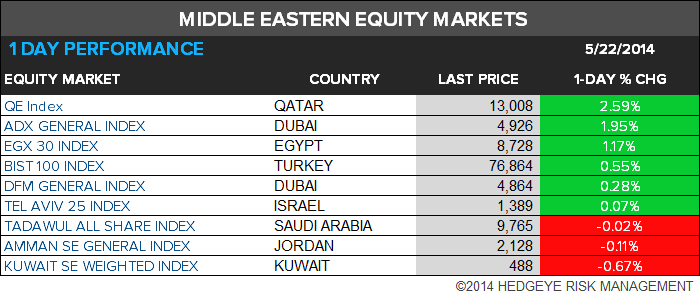

MIDDLE EAST

The Hedgeye Macro Team