Conclusion: Though the fundamental call is playing out as expected, we still think TGT is a ‘Best Idea’ short. The reality is that the narrative on this name will change dramatically over the next 12 months after a real CEO is hired, major strategic decisions are made and we get away from the tactical discussion about whether traffic is up or down by 50bps or how many Frozen DVDs Target sold. We’ll be talking about a new CEO’s vision to both transform the company, and fix all the mistakes made over the past 5 years. That might sound like great news, but it will be expensive news. You don’t build a world-class e-commerce platform without investing a few billion on the balance sheet and P&L. You also don’t change the make-up of your customers and product offerings and brand image without some painful organizational changes and operational expenses that hurt over a multi-year time period before they ultimately help grow market share, margins, and returns. Our point is that the bar has been reset for this FY closer to a level that we think is doable. But this company might not earn anything higher than $4.00 for another 3-years. We won’t wait a day for mediocrity – nevermind 3 years. This stock should have a 4-handle.

DETAILS

We added TGT to our Best Ideas list as a Short on 4/24, and there it will stay. The quarter played out exactly as planned; the company traded margin for comp (which was still negative) in the US, and meaningfully underperformed in Canada. But our call went far beyond the quarter. It is based on the premise that five years ago Target set out on a path to dramatically alter its persona. Mind you, in the mid-2000s Target was the anti-Wal-Mart, and was viewed as a fashion leader for a younger demographic (i.e. Tar-Jay). At that point, it was clearly worth a higher multiple, which it consistently commanded. But then three things happened that would ultimately cost Sheinhafel his job – and No, one of them was NOT the data breach.

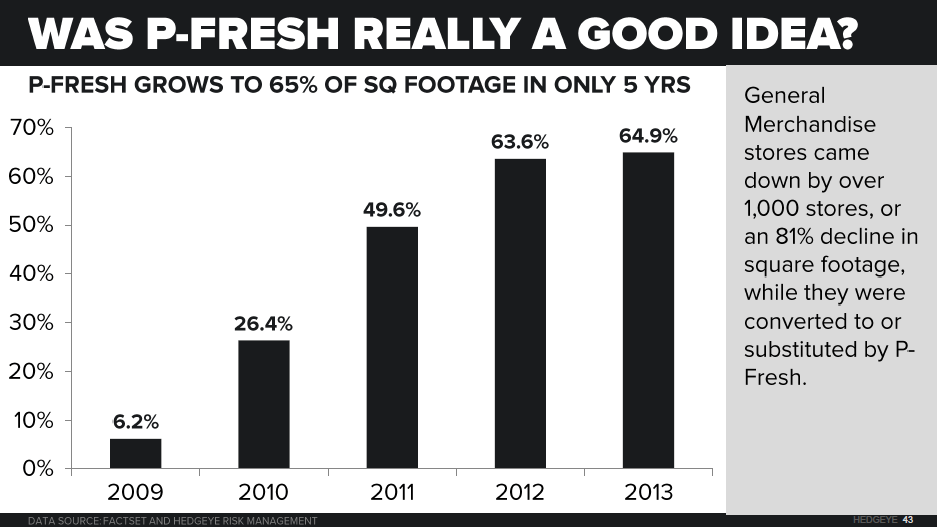

1) TGT converted 65% of stores to P-Fresh – which mirrored WMT’s supercenters (ie sell people milk and eggs so they stick around and buy diapers, sweaters and lipstick).

2) TGT pushed the Red Card, which offered 5% off on all purchases. This went from 6.5% of sales to 20% of sales over 5 years.

3) The company was spending on the above initiatives while the rest of retail was investing in e-commerce, something TGT is severely deficient in.

Maybe all these things seemed a good idea to TGT at the time. But it fundamentally changed the makeup of the company.

1) That old cool Tar-Jay is not just dormant, but it is officially dead. Now TGT competes in the US more closely with WMT than it ever has before. So it’s got WMT on one end, supermarkets on another, department stores on another, and even dollar stores to a certain extent. This is one of the least appealing competitive sets we can think of. And that’s not even mentioning AMZN, which is emerging as one of its biggest competitors whether Target likes it or not.

2) The Red Card might have seemed like a good idea as well. After all, some retailers have had great success with similar reward cards. It’s not the 100bps in margin that TGT gives back to consumers that we have a problem with. But rather, we think that the mix of customers changes meaningfully when you start incentivizing them with price. To be clear, we understand the nature of US retail, and price discounting can be a great weapon. But when TGT was more of a cool-ish fashion-leading department store, it did not have to incentivize people with a Red Card to be loyal. Now it is a different animal altogether. Our point is that we encounter many people who think that historical peak margins could someday be doable. We think it’s close to impossible.

3) Lastly, the dot.com element is pathetic. Every statistic we track shows that target.com is near the bottom of the pack when compared to other retailers’ online business. We hear Mulligan say on the conference call that they are ‘channel agnostic’, and that they don’t care if a person buys online or in the store. Seriously? 46% of what your store sells is Food and Home Essentials – these are things that you need people to come into the store to buy repeatedly at lower margin so they buy high margin seasonal goods. This company needs people in its stores, period.

SO WHAT HAPPEN’S NOW

We think that today’s conference call was so bad yet so enlightening. We walked away with the firm view that both the company and the Street are hyperfocused on issues that are impacting the next 2-3 quarters of earnings. Those things are important as it relates to near-term trading. We respect that. But the reality is that there were some people who are interviewing for the CEO job who were listening in to the call. Others will read the transcript. Those people could care less about a couple points in traffic growth, or weakness in gross margin, or whether Target sold a million Frozen DVDs (still in disbelief that they talked about this). They’re going to have to make a handful of strategic decisions when they start their new job if they want to get paid 3-5 years down the road -- because status-quo is not acceptable. If it is, then the Board will be hiring the wrong person, and they should probably hand in their own resignations while they’re at it.

Our point here is that what we heard on today’s call is a narrative that will be a distant memory in 9-12 months’ time. We’ll be talking about a new CEO’s vision to both transform the company, and fix all the mistakes made over the past 5 years. That might sound like great news, but it will be expensive news. You don’t build a world-class e-commerce platform without investing a few billion on the balance sheet and P&L. You also don’t change the make-up of your customers and product offerings and brand image without some painful organizational changes and operational expenses that hurt over a multi-year time period before they ultimately help grow market share, margins, and returns.

The bar has been reset for this FY closer to a level that we think is doable. But this company might not earn anything higher than $4.00 for another 3-years. We won’t wait a day for mediocrity – nevermind 3 years.