One of the main lessons from what is becoming as forceful an up move as we had on the way down is that Wall Street continues manages risk on a revisionist basis. This is not a proactive investment process. It’s reactive, and you should capitalize on its outputs.

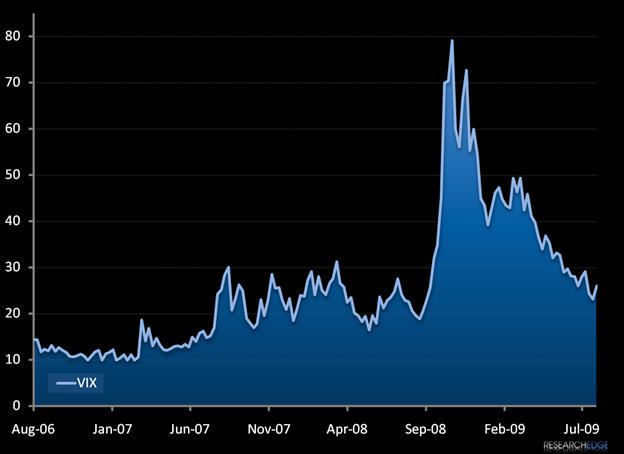

Prior to Q2 of 2008, for most 30-year old hedge fund managers a VIX above 30 was unheard of. Although I’m using that age to be cute, the reality is that there are very few institutional managers who managed their portfolios in a 30-80 VIX environment prior to 2008. Today, there are equally as many PM’s who are being told to manage their exposures towards a 30-80 environment AFTER the fact.

The probabilities of seeing a VIX over 30 anytime in the immediate term are very slim. That, of course, makes the 30-80 range a tail risk that we should perpetually consider. But it also means that you’ll get crushed on 97% of the days in this current trading environment by hedging towards that tail risk scenario. Tail risk is exactly that – not in the heart of the bell curve of daily price distributions.

Across all three of our key durations, the VIX remains broken. While it’s nowhere near as nasty as the US Dollar chart, this is one of the most bearish charts in all of global macro right now.

The long term TAIL line = $41.29 and the intermediate term TREND line = $30.57. Until you see these lines penetrated to the upside, you’ll be paid to buy low and sell high.

Trade the range confidently, rather than in fear. The days of calling for crashes and squeezes are behind us… for now… simply because everyone continues to look for them.

KM

Keith R. McCullough

Chief Executive Officer