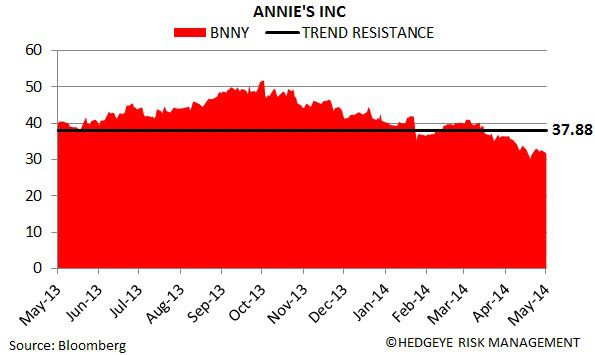

We added Annie’s (BNNY) to our Best Ideas list as a short on 04/07/2014 at $37.16/share. Since this time, the stock has traded down approximately ~15% while earnings estimates have essentially remained flat. With the company set to report 4QF14 earnings on June 10th, we are reiterating our short.

To be clear, we believe Annie’s is a strong, resonant brand that is well positioned to grow within the natural and organic segment of the food industry. This is generally acknowledged by the street, as the company has been awarded a substantial premium valuation to its peer group. While this gap has tightened since we released our call, it still exists to a notable degree. BNNY is showing significantly stronger top line growth than its peers, but we have legitimate concerns with the company’s ability to manage EPS in the intermediate-term; a risk that we believe is not fully reflected in stock.

In our view, managing a rapidly growing business is becoming increasingly challenging – a problem the recent Joplin plant acquisition could exacerbate. While last year’s balance sheet issues give cause for concern, management has done an adequate job tightening internal controls. What is more concerning to us, however, is increased competition (WWAV, WMT), building margin pressure (cheese, organic grains), a lack of earnings visibility and aggressive estimates.

We remain bearish on an intermediate-term TREND duration and continue to believe that 4QF14 and FY15 estimates will prove too aggressive as Annie’s incurs some common growing pains.

Research Recap:

New Best Idea: Short BNNY (04/07/2014)

Presentation: Short BNNY (04/10/2014)

BNNY: Intermediate-Term Downside (04/11/2014)

Howard Penney

Managing Director

Fred Masotta

Analyst