Tickers: HK.0027, IGT, MGM, OEH, PEB, CCL

EVENTS TO WATCH

- May 23 - Codere 1Q 2014 10am

- May 27 - Aristocrat 1H 2014 11pm (, Passcode: 9068797)

COMPANY NEWS

Galaxy Entertainment Group - (Macau Business Daily) According to Michael Mecca, President, Galaxy could record “high single digit growth in VIP gaming revenue this year”

TAKEAWAY: High single digit VIP gaming revenue growth would exceed investors' current expectations. We've been consistently modeling 7% VIP growth for 2014.

Genting Berhad - The Nevada Gaming Commission found Malaysia-based Genting Berhad suitable to do business in the state as Resorts World Las Vegas. Genting plans to incorporate 80 percent to 85 percent of the Echelon buildings into the Resorts World development. The first phase of RWLV is expected to be complete in 24 to 36 months.

TAKEAWAY: A formality given we witnessed site activity during a recent visit to Las Vegas

IGT - selected Matsui as the exclusive distributor for Electronic Gaming Machines in Korea.

TAKEAWAY: Establishing a relationship to help with the penetration of the developing Korean gaming market.

MGM - will spend more than $450 million to create The Park, an outdoor retail, dining and entertainment complex located between Monte Carlo and New York-New York. The project is anchored by a 20,000-seat sports arena and events center. MGM Resorts Chairman and CEO Jim Murren said the plans “do not include one single slot machine or table game.”

TAKEAWAY: Betting big on non-gaming amenities. Casino trends are still not great but we'd like to see the ROI analysis on this.

6460.JP Sega Sammy - Sega Sammy Creation (a division of Sega Sammy Holdings, Inc.) was established in June 2013 as a gaming machine manufacturer, with a focus on large-sized products. This week at G2E Asia 2014, the company unveiled the Sic Bo Bonus Jackpot, with four progressive levels of jackpot. Sega Sammy Creation plans to sell to casinos in Macau, Singapore and the Philippines, once its products are approved by regulators followed by North America and Japan - after gaming legislation is approved.

TAKEAWAY: Sega Sammy in the mix for Asian slots

OEH - According to the Spanish web-site (www.expansion.com) Marriott is the leading buyer the Hotel Ritz in Madrid. The U.S. hotel giant has offered 130 million euros for the historic property. OEH owns 50% of the hotel. OEH purchased the Hotel Ritz with its partner in 2003 for 125 million euros.

TAKEAWAY: A great price for a low EBITDA generating asset as well as considering industry experts believe the hotel needs between 40 million and 50 million euro capex investment.

PEB - acquired the 160-room Prescott Hotel, located in Union Square in San Francisco for $49 million or approximately $306,000 per key. Pebblebrook indicated it will undertake a comprehensive renovation and repositioning of the hotel sometime between 2015 and 2016, including all guest rooms, bathrooms and public areas

TAKEAWAY: By our math, we estimate PEB will spend an additional $8 million to renovate the property with the hope of doubling ADR and RevPAR. Assuming the majority of the incremental revenue drops to EBITDA, we estimate a 20% return on total invested capital for shareholders – but this is predicated on significantly higher ADR.

CCL - (Cruise Critic, Cruise Currents, Travel Weekly) Arnold Donald commentary:

- Carnival brand had record bookings over past few months. Public perception has improved.

- Most of China do not know about cruising

- Holland America's new ship will replace the lost capacity from the transfer of two older ships to Australia

- Need to convey the cruise product and value compared to a land vacation.

- MSC 2 new ships

- Would have only a "tiny percentage" impact on industry

- Risk that “psychological pricing” which could be introduced by MSC to fill its extra capacity could have a negative impact on rival lines

- Should create incremental demand and "soften the beachhead" to attract new-to-cruise customers

- CCL is the 5th largest purchaser of air travel in the wrold.

TAKEAWAY: Mostly positive commentary ahead of earnings in June but we do worry about industry supply growth.

CCL - (TTG) CLIA 2014: Commission remains an 'ongoing debate'

Carnival UK’s chief commercial officer, Gerard Tempest, has conceded that remuneration still “continues to be an ongoing debate”. Tempest insisted there were no immediate plans to alter the current 7% commission levels, which were increased in December last year, but added: “Never say never”. Tempest also conceded that late discounting remained an issue for the sector which, like all cruise lines, he is keen to tackle. “We are in an ongoing dialogue about our pricing strategy to see what we can do about some late discounting

TAKEAWAY: Still cautious on price discounting. On a fleetwide basis, CCL commissions as a % of gross revenues have been steady in 2012-2013 at 15.1%.

INDUSTRY NEWS

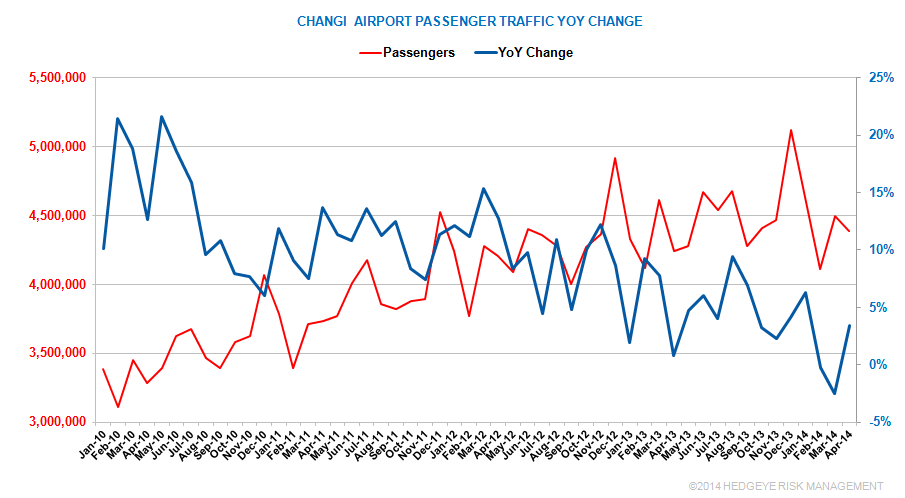

Singapore Changi visitation - handled 4.38 million passenger movements in April, +3.4% YoY. Thailand and China traffic registered declines of 15% and 8.0% respectively.

TAKEAWAY: The slowdown in Thai and Chinese travel is a worrisome trend.

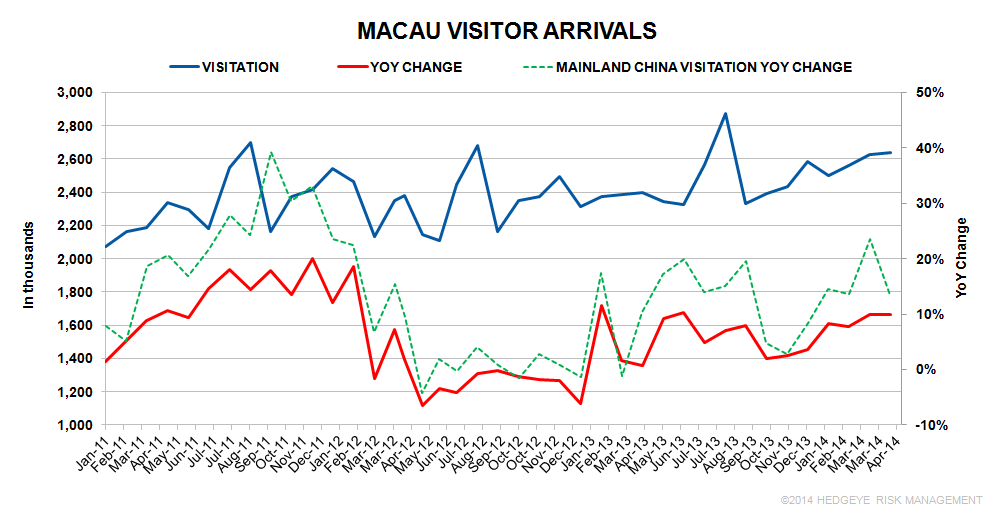

Macau visitation - attributable to the Easter holidays, visitor arrivals increased 10% YoY to 2,636,614 in April 2014. Visitors from Mainland China increased by 14% YoY to 1,743,776, coming primarily from Guangdong Province (685,796), Fujian Province (72,282) and Hunan Province (63,972). Mainland visitors travelling under the Individual Visit Scheme totaled 707,085, sharing 41% of the total from Mainland China. Visitors from Hong Kong (585,824) and the Republic of Korea (33,975) increased by 9% and 11% respectively. The average length of stay of visitors remained unchanged from a year earlier at 1.0 days.

TAKEAWAY: Good visitation numbers from Mainland China and Hong Kong.

Culinary Local 226 Workers to strike – against nine Downtown Las Vegas hotels/casinos beginning June 1. Upward of 2,000 restaurant workers, hotel housekeepers, cocktail servers, bartenders, and other members of the unions plan to walk off their jobs and picket outside the D, Four Queens, Binion’s, Fremont, Main Street Station, Plaza, Las Vegas Club, El Cortez and Golden Gate. However, union leaders still have meetings with El Cortez and Boyd Gaming Corp., which owns Fremont and Main Street Station casinos, scheduled before the strike date.

TAKEAWAY: We expect the remaining operators to reach agreement with the Union and avoid the disruptions of a worker strike.

Las Vegas Withdrew from 2016 GOP Convention Process - The Las Vegas 2016 Host Committee sent the withdrawal letter to the Republican National Committee because the Las Vegas Convention Center would have trouble “clearing enough days in the June 2016 calendar” to set up and host the presidential nominating party as well as lacked VIP sky boxes required for the event. Additionally, despite strong support from Sheldon Adelson and Steve Wynn, the city also was having problems guaranteeing $60 million to $70 million to hold the event. Denver, Dallas, Cleveland and Kansas City, are the remaining contenders.

TAKEAWAY: A mild negative for Las Vegas.

Macau Resident Payouts - The government says it will begin paying this year’s cash handouts in the first week of July. Executive Council spokesman Leong Heng Teng says that between July and September the government will share MOP5.65 billion (US$707.46 million) among about 650,000 people. Over 590,000 permanent residents will each receive MOP9,000 (MOP1,000 higher than last year) and over 61,000 temporary residents will each receive MOP5,400.

Additionally, the government will make a MOP7,000 deposit directly into the retirement fund for each eligible residents and a smaller MOP5,400 contribution for non-permanent residents. The amounts to be paid are the biggest ever since cash handouts began in 2008.

TAKEAWAY: The residents share in the gaming profits.

Avian Flu - the National Health and Family Planning Commission of China notified the World Health Organization (WHO) of four additional laboratory confirmed cases of human infection with avian influenza A (H7N9) virus.

TAKEAWAY: Not much to worry about at this point.

China Immigration - Guangdong authorities received at least 10,000 applications on the first day of the E-permit pilot scheme.

TAKEAWAY: Strong early applications for a "e-passport" which will reduce border crossing immigration processing time from 30-45 seconds to 8-10 seconds.

Lodging Transaction - The St. Regis Monarch Beach Resort has been sold to KSL Capital Partners LLC, a Denver-based private equity firm, by an affiliate of Washington Holdings. No transaction details were disclosed.

TAKEAWAY: Great timing on the acquisition and better timing on the sell.

MACRO

China Residential Real Estate- according to the Shanghai Securities News report that the Ministry of Housing will ease property restrictions for 30 non-first-tier cities, especially in those that have an over-supply of homes. While the ministry has decided on the policy, there remains no concrete timing for implementation, and first-tier cities will likely be excluded due to continuous signs of rising home prices.

TAKEAWAY: Anything to stem the macro decline

Hedgeye remains negative on consumer spending and believes in more inflation. Following a great call on rising housing prices, the Hedgeye

Macro/Financials team is turning decidedly less positive.

TAKEAWAY: We’ve found housing prices to be the single most significant factor in driving gaming revenues over the past 20 years in virtually all gaming markets across the US.