********** High Frequency Trading Conf Call This Thursday **********

We will be hosting a conference call with former SEC Commissioner Roel Campos this Thursday, May 22nd at 2pm EST to weigh in on the current structure of the equity and derivative markets and how regulation around High Frequency Trading (HFT) may come down from regulators.

Mr. Campos served as one of the five commissioners of the Securities and Exchange Commission under Chairmans' William Donaldson and Christopher Cox from 2002 to 2007 and was instrumental in crafting the Commission's National Market System (Reg NMS) framework. Mr. Campos recently testified in front of the House Financial Services Committee in February of this year in a Hearing entitled "Equity Market Structure: A Review of SEC Regulation NMS."

CLICK HERE to add this Hedgeye Speaker Series call to your Outlook calendar; otherwise, the dial in instructions are also below:

Participant Dialing Instructions

Thursday May 22nd at 2 pm EST:

- Toll Free Number:

- Direct Dial Number:

- Conference Code: 189818#

This call should be of interest to investors in the following stocks:

NDAQ, CME, ICE, GS, MS, BLK, & JPM

Current Best Ideas:

Key Callouts:

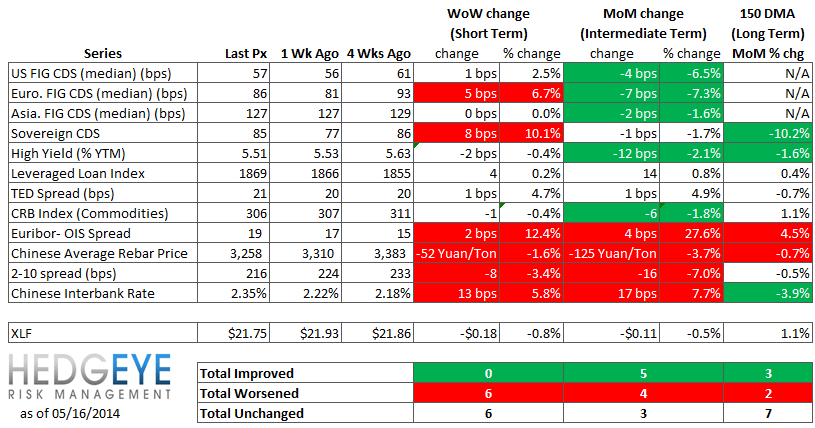

Two important callouts this week include the yield spread compression and the rising Euribor-OIS spread.

* 2-10 Spread – Last week the 2-10 spread tightened to 216 bps, -8 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

* Euribor-OIS Spread – The Euribor-OIS spread widened by 2 bps to 19 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 0 of 12 improved / 6 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Positive / 5 of 12 improved / 4 out of 12 worsened / 3 of 12 unchanged

• Long-term(WoW): Positive / 3 of 12 improved / 2 out of 12 worsened / 7 of 12 unchanged

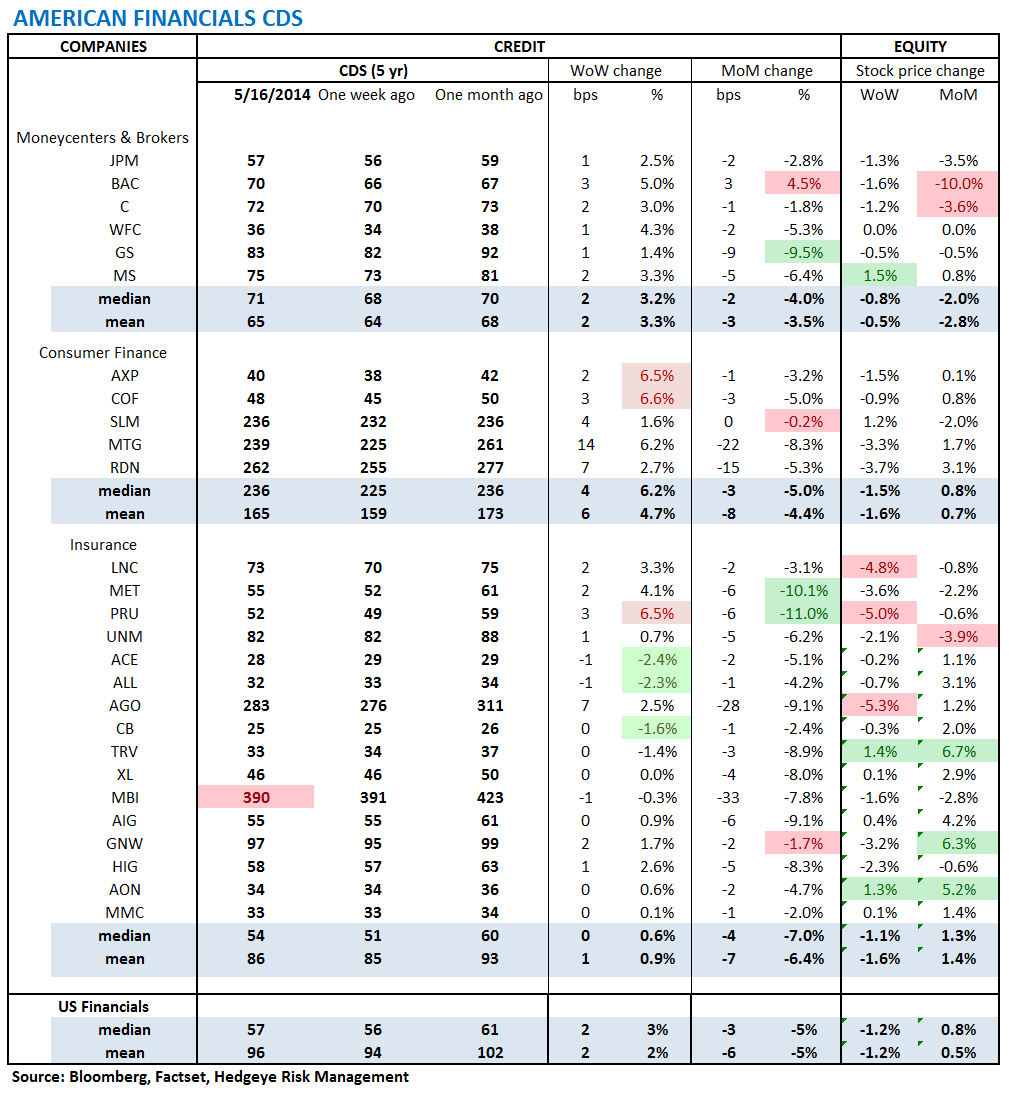

1. U.S. Financial CDS - Swaps widened for 21 out of 27 domestic financial institutions, but were wider by just 2 bps week-over-week.

Tightened the most WoW: ACE, ALL, CB

Widened the most WoW: COF, AXP, PRU

Tightened the most WoW: PRU, MET, GS

Widened the most/ tightened the least MoM: BAC, SLM, GNW

2. European Financial CDS - Swaps were notably widener in Europe last week, but remain modestly tighter month-over-month. Greek banks, which have seen their swaps tighten steadily for months now widened sharply.

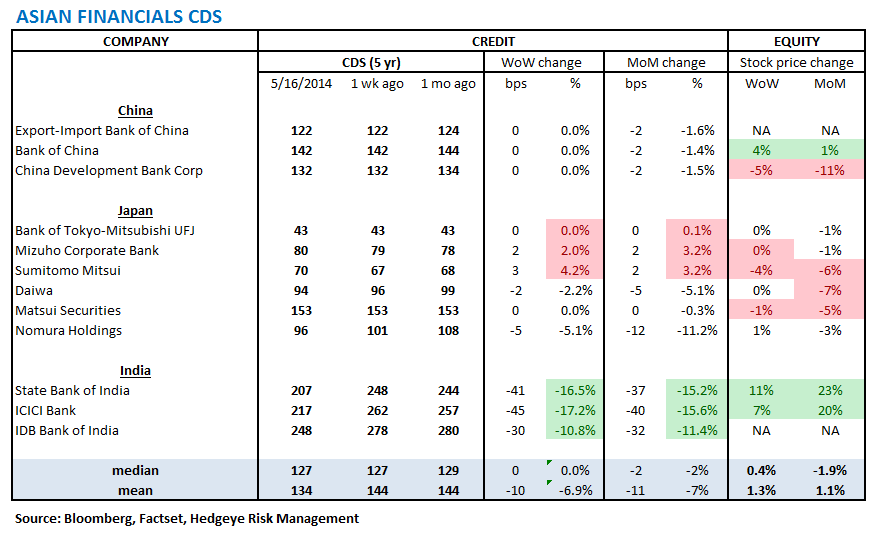

3. Asian Financial CDS - Indian banks were notably tighter last week, coming in by an average of 39 bps and are now tighter by almost as much on a month-over-month basis.

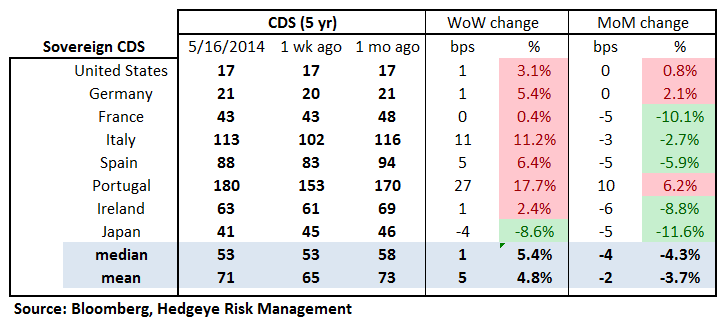

4. Sovereign CDS – Sovereign swaps widened last week. Italian sovereign swaps widened by 11% (11 bps to 113) and Portuguese sovereign swaps widened by 18% (27 bps to 180).

5. High Yield (YTM) Monitor – High Yield rates fell 2.2 bps last week, ending the week at 5.51% versus 5.53% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 3.0 points last week, ending at 1869.

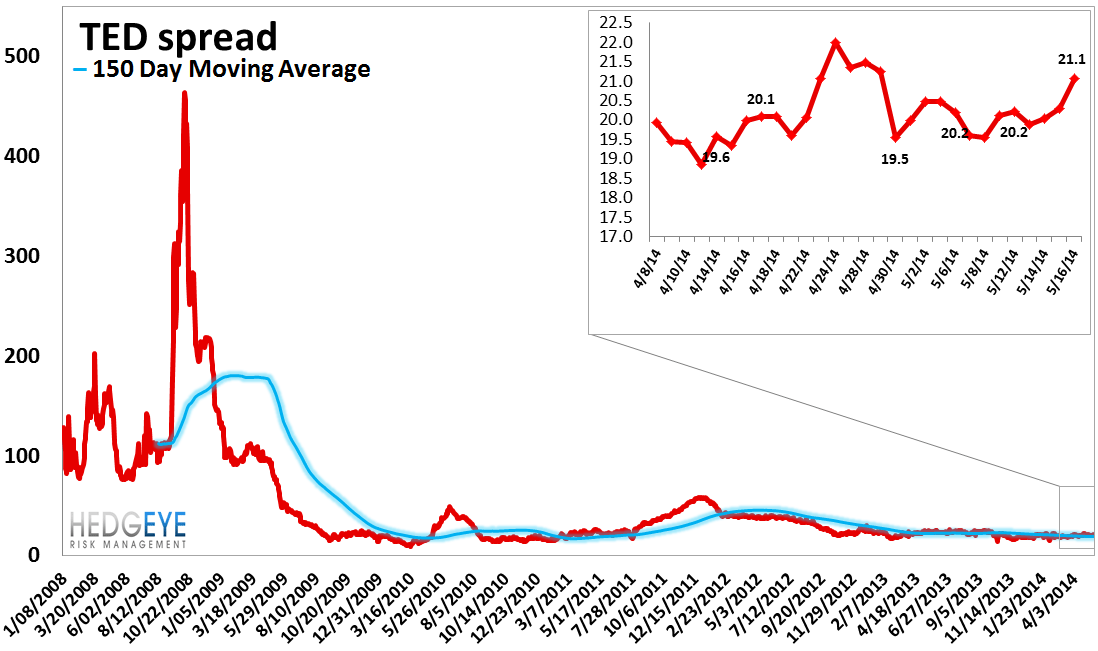

7. TED Spread Monitor – The TED spread rose 1.0 basis points last week, ending the week at 21.1 bps this week versus last week’s print of 20.11 bps.

8. CRB Commodity Price Index – The CRB index fell -0.4%, ending the week at 306 versus 307 the prior week. As compared with the prior month, commodity prices have decreased -1.8% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 19 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 13 basis points last week, ending the week at 2.35% versus last week’s print of 2.22%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China fell 1.6% last week, or 52 yuan/ton, to 3,258 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

12. 2-10 Spread – Last week the 2-10 spread tightened to 216 bps, -8 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.8% upside to TRADE resistance and 1.4% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT