RETAIL FIRST LOOK: "THESE GO TO 11"

03 AUGUST 2009

TODAY’S CALL OUT

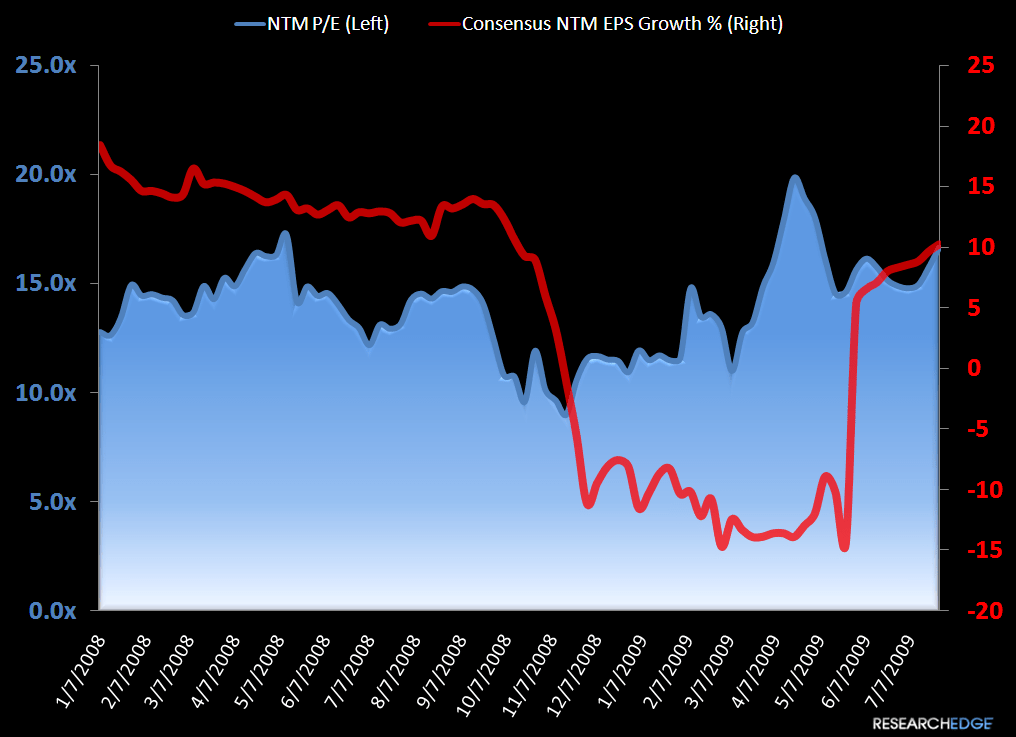

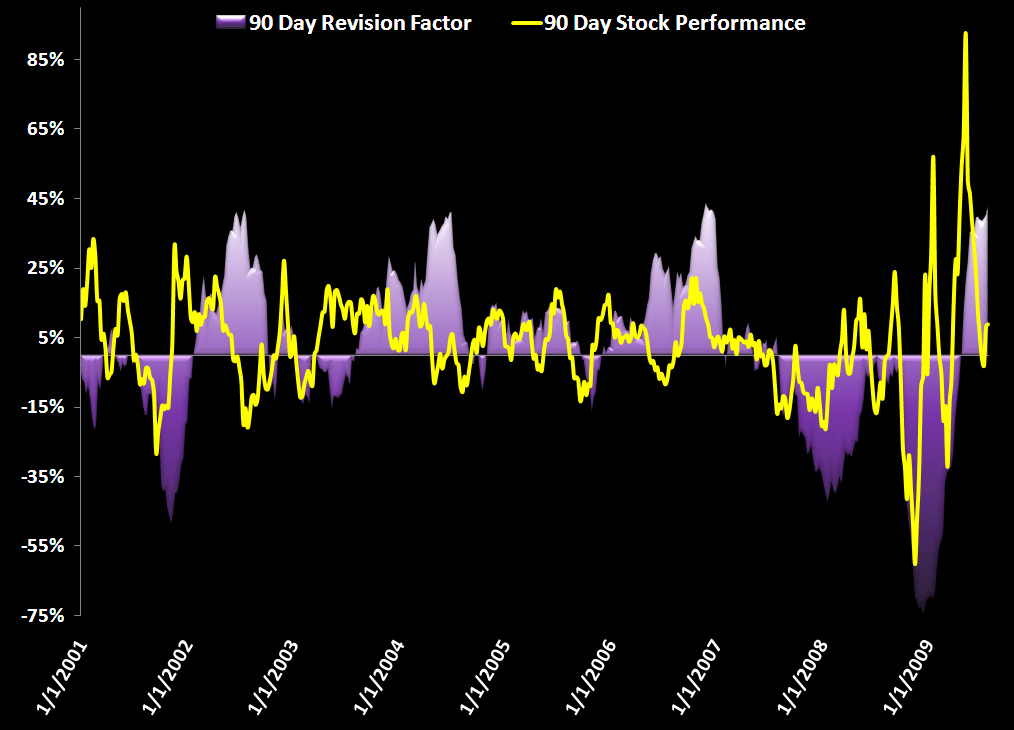

We’ve seen forward earnings growth expectations go from 6-11% over the past month. Yes the group has run meaningfully. But 11 to 20% over 3 months is not out of the question. Do you want to be short into that? Be my guest.

For those of you that have never seen the parody about the 1970s fictional metal band, go to YouTube and search for ‘these go to 11.’ It kind of speaks for itself. Unlike Nigel Tufnel, I am not focused right now on modified Marshall amps, but on consensus earnings growth expectations for the next 12-months.

Why? Well, because it matters more than ever with a 15% run in the MVR vs. a 10% run in the market over the last month. Is the outperformance justified? My opinion is that it definitely is. Math does not lie. We’re seeing the rate of earnings growth accelerate into the back half. We can all say ‘yeah the market already knows this, and the group is trading at a 15x p/e.’ But the reality is that we’ve seen forward earnings growth expectations go from 6% to 11% over the past month. Yes, the market knows this, but here’s a novel thought… With excess SG&A cuts, ridiculously easy comps, and fall/holiday ordering plans down in the double digit range (setting up for firm inventory position and higher GM%), can forward growth expectations pierce 20% within 3 months? The answer is Yes.

These go to 20?

That, my friends, is not yet in the stocks today. Do not get me wrong. McGough is not a blind bull oblivious to the factors impacting consumer spending (and retrenchment) over the next 2-3 years. But we’ve got more good news to come from the EPS picture before any big downside calls on the group make sense to me.

LEVINE’S LOW DOWN

Some Notable Call Outs

- In a move sure to challenge Wal-Mart’s low-price leadership, Kmart is selling a 24-count box of Crayola Crayons for $0.20 this back to school season. Kmart’s price is 20% below Wal-Mart’s price of $0.25! If you’re not into the buying the iconic yellow and green box, then head to Office Max for a box of Schoolio von Hulio crayons for $0.01 (yes, a penny). This certainly seems like the making of “crayon wars” to me.

- While many bankruptcy cases in the retail sector have resulted in liquidation, there are a few exceptions. On Friday, after just four months of Chapter 11 protection, Sportsman’s Warehouse announced the court approved the company’s reorganization plan. The outdoor retailer’s emergence from bankruptcy is a result of a capital infusion from private equity firm, Seidler Equity Partners. Interestingly, Cabela’s mentioned last week that it was gaining market share from a competitor operating under Chapter 11.

- Over the past few weeks, I’ve highlighted several companies that are experimenting and using social media sites/Twitter to promote brands and to connect directly with target consumers. However, the power of the Internet and “crowdsourcing” is now being used in a new way. Let me draw your attention to Groupon, a marketing company uses the power of the masses on the Internet. Groupon sends out daily e-mails with a deal that offers a product or service at a discounted price. The business relies on the collective purchasing power of a group of interested consumers, hence the name Groupon. Participating merchants pay a commission, which makes the service a viable business at a time when so many online ideas are interesting but not profitable. For the deal of the day to work, a minimum number of people have to buy it. That “crowdsourcing” encourages subscribers to tell their friends, family and co-workers. As word spreads, the selected business gains exposure. While the service currently operates in about 14 cities, expect the “buzz” on this one to grow quickly. After all, the viral nature of the Internet and the consumers’ appetite for a deal could not intersect at a better time than now.

MORNING NEWS

- Vendors can perhaps breathe a little easier over CIT - The group’s profitable factoring business, Trade Finance, on Friday got a boost when $1 billion was earmarked to fund the operation, a move aimed at proving to vendors that CIT has the money to fund clients’ needs. In a letter to clients, John Daly, president of Trade Finance, wrote that “CIT Trade Finance is one of the nation’s oldest providers of factoring and financing services. The companies that have placed their confidence in us — our clients — range from family-owned and -operated manufacturers to global publicly traded corporations. We believe we have sufficient liquidity to meet our obligations and our clients’ needs while our parent company implements its restructuring plan.” CIT Trade Finance “remains open for business. We are actively reaching out to and working with our clients to ensure they continue to access our services needed to run their business. Credit is being checked, invoices are being collected and funds are being remitted,” Daly emphasized. <wwd.com/business-news>

- Vietnam apparel industry to improve working conditions - Better Work Vietnam has begun offering new services to apparel enterprises in Vietnam’s southern provinces, helping them improve working conditions for more than 700,000 workers and boost the competitiveness. Tara Rangarajan, Program Manager of Better Work Vietnam, said: "Better Work Vietnam looks forward to working as partners with Vietnamese apparel enterprises, workers, and the Government of Vietnam to make sustainable improvements in labor conditions. The goal of our work is to find practical solutions that will decrease costs for project participants, enhance factory competitiveness in international markets, and reduce poverty among Vietnamese apparel workers, their families, and communities". Initially targeting apparel factories with more than 200 workers located in Ho Chi Minh City and neighboring provinces," said Nguyen Van Tien, chief labor inspectorate of MoLISA and chair of Better Work Vietnam’s Project Advisory Committee. <fashionnetasia.com>

- British retail organization giants combine - The British Fashion Council (BFC) is the latest organization to become a member of the trade association UK Fashion and Textile Association(UKFT). "UKFT’s aim is to be the ‘single voice’ of the fashion and textile industry, representing businesses of all sizes – whether they be a small design-led company or a multi-million pound organization. Having the BFC on board adds further depth on the design side and enables us to work more closely on initiatives that will help designers be better placed to develop sales both in the UK and overseas and receive first-hand guidance on national and international issues that will affect them," said Peter Lucas, chairman, UKFT. Harold Tillman, chairman, BFC, added: "The BFC promotes leading British fashion designers in a global market, supports emerging talent to showcase and develop their businesses and organizes events, including London Fashion Week and the British Fashion Awards, to support these goals and strengthen the UK’s reputation for developing design excellence. <fashionnetasia.com>

- Annual report of sport participation - The annual report is out from the Sporting Goods Manufacturers Association. The report details participation trends in sports and provides insight into what sports are growing and what sports are hurting. Here are some interesting figures: (1) The biggest increase in participation in team sports in 2008 was ultimate Frisbee, up 20.8%. (2) Hunting and target shooting with a handgun was up 10.7% and 13.9%, respectively, this year. (3) There were 17 million people playing table tennis last year, a 15.5% increase from 2007. (4) The worst decline in participation in team sports in 2008 was roller hockey, down 15.4%. (5) Last year, 15% of cheerleaders and 29% of gymnasts were male. (6) Last year, 6% of tackle football players and 18% of paintball players were female. (7) Archery participation was up 7.7 percent. (8) Skateboarding participation was down 7.4% in 2008 and is now down 20.8% since 2000. (9) Interest in the UFC might be skyrocketing, but mixed martial arts participation actually went don 1.4% last year. That has nothing on boxing, which is down 42.3% as compared to participation in the sport eight years ago. (10) Lacrosse has long been called the fastest growing sport in America, as it has grown 117% since 2000. Still, only 1.9 million people played lacrosse in 2008 compared to something like slow pitch softball, which had 9.8 million participants. <cnbc.com>

- Footwear companies saw shares plummet in 2008, so for many in 2009, there’s been nowhere to go but up - But even as shares grew in percentage, few firms saw their stock prices return to the levels seen at the beginning of last year. Here’s how the retailers tracked by Footwear News stacked up in the first half of 2009, ranked by percentage of change: Dillards 133%, Sears Holdings Corp. 72%, TJX Cos. 54%, Nordstrom Inc. 49%, JC Penny 45%, Bakers Footwear Group 39%, Foot Locker 39%, Collective Brands 24%, Shoe Carnival 23%, Dick's Sporting Goods 22%. <wwd.com/footwear-news>

- German Retail Sales Unexpectedly Slump for Second Month on Unemployment - Retail sales in Germany, Europe’s largest economy, unexpectedly dropped for a second month in June as rising unemployment prompted consumers to trim spending. <bloomberg.com>

- A Gap and Levi Strauss jean factory in Africa is illegally dumping chemicals - A factory that makes jeans for Gap and Levi Strauss is illegally dumping chemical waste in a river and two unsecured tips where it poses a hazard to children. The scandal was uncovered by a Sunday Times investigation into pollution caused by a plant in Lesotho, southern Africa, which supplies denim to the two companies. Dark blue effluent from the factory of Nien Hsing, a Taiwanese firm, was pouring into a river from which people draw water for cooking and bathing. The firm was also dumping needles, razors and harmful chemicals such as caustic soda at municipal dumps that have attracted child rag-pickers as young as five in search of cloth fragments to sell for fuel. Many of the children, who work for up to 10 hours a day, complain of breathing difficulties, weeping eyes and rashes. <theretailbulletin.com/news>

- Van Heusen looks to expand retail presence in India - Apparel brand Van Heusen from the Madura Garments group is looking to implement an extensive retail expansion plan by opening 25 exclusive stores this year and 65 more stores by the end of financial year 2012. The brand wants to have a pan-India presence and reach 50 tier-I and tier-II cities. The average size of the stores will be 200 square feet and the flagship stores will cover 7,000 square feet. The company is planning most of its stores on high street locations because it does not want to be dependent on malls. The company will have stores in four different formats – men, women, V Dot for youngsters and a combination of all of these. <indiaretailing.com>

- Private label beauty manufacturer purchases large stake in Lucy B Cosmetics - Absolute Amenities Inc., a Riverside, Calif.-based private-label beauty manufacturer headed by Jackie Applebaum, has purchased a stake in Lucy B Cosmetics for an undisclosed sum. Baldock and Sacchi are remaining with the brand and are creative directors as well as president and vice president, respectively. “The creative person really has to be free to be creative, and then there is the other side of how do you make the business run,” said Applebaum. “You can’t build a house unless you have a strong foundation. That is my job to build the foundation. It’s Lucy’s job to build the beautiful house.” Applebaum said she could provide Lucy B Cosmetics with the back end and financing needed to grow the brand beyond its current distribution of roughly 270 U.S. doors, including Anthropologie and QVC. She added the brand’s focus on specialty stores wouldn’t change and estimated it would generate $3 million in retail sales in the first year of her involvement. The Lucy B Cosmetics assortment contains 22 stockkeeping units that use ingredients from Australian flowers and colorful graphics evocative of the Australian landscape. <wwd.com/business-news>

- Sport Supply Group, Inc. said it has acquired certain team sports assets from Har-Bell Athletic Goods of Springfield, MO - Bryan Tucker, Owner of Har-Bell, will be employed by SSG as will his existing sales force in Missouri. Sport Supply did not assume any liabilities in the transaction. Terms were not disclosed. <sportsonesource.com>

- Highline United making progress in footwear - Executives at Highline United may have stepped into the footwear arena quietly with soft launches in 2008, but they are now gearing up to draw major attention to their portfolio of brands. The New York-based firm, whose brand roster includes United Nude, Ash and Luxury Rebel, along with licensing agreements with Miss Sixty and Tracy Reese, formally debuted in June with a launch party at its 7,600-sq.-ft. Chelsea showroom and is making a concentrated push to attract department stores and better independents with its mix of bridge women’s footwear.“June was our coming out party,” said Highline United President Matt Joyce, who has held top sales and merchandising roles at Nordstrom, Via Spiga, Kenneth Cole, Nine West and Steve Madden. “We wanted to make sure we brought in the product correctly, are taking care of our customers and have [footwear] that is viable for the future.”The company, named after New York’s newest city park, an elevated and out-of-service railway called the High Line, began showing capsule collections at last summer’s FFANY and WSA shows and has spent the last year building a mix of brands targeted at retailers looking for bridge-priced footwear that has been designed and sourced globally.“We have people in Italy, France, China, the U.K. and Russia,” Joyce said. “It’s a global mentality [and] it gives us the opportunity to get a broader view rather than just see what’s happening in [one place].” Early goals for the company, said VP of sales Scott Kaminsky, include building each of the brands and positioning the firm to become a long-term and dominant player in the industry. <wwd.com/footwear-news>

MACRO SECTOR VIEW AND TRADING CALL OUTS: