This note was originally published at 8am on May 05, 2014 for Hedgeye subscribers.

“There is no friendship in trade.”

-Cornelius Vanderbilt

Forget about what Facebook (FB) did on Friday. In one of the more epic 2 hour moves I have ever seen, the US bond market un-friended the US growth bulls, big time.

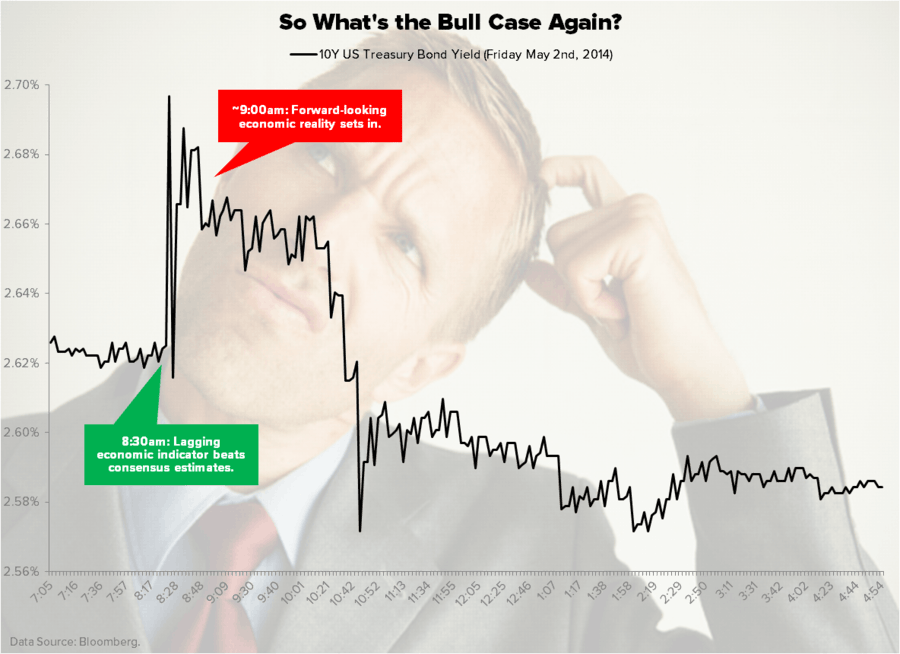

At 8:30AM the lagging of all lagging economic indicators (the monthly US unemployment rate) was met with some of the funniest tweets my contra-stream has ever seen: “Boom!” (as in this is great report), “Bye bye Bond Market”, “Stocks gonna rip!”, etc.

By 10:30AM, as you can see in the Chart of The Day, anyone who bought US growth stocks and sold what’s been working all year (Gold, Bonds, etc.) felt shame. #Tweetless

Back to the Global Macro Grind…

To be crystal clear, with the 10yr US Treasury Yield -15% YTD to 2.58% and US GDP 0.11% in Q114, Mr. Macro Bond Market has completely nailed it in 2014.

Since everyone other than guys @ISI (who are trying to story-tell about 3-4% US Growth) understands the relationship between a rising bond market (falling bond yields) and falling growth expectations, the real-time price truth is on the tape.

With the Russell2000 (proxy for US Growth stocks) -3% YTD, what else is going on out there on the scoreboard?

- US Dollar down another -0.3% last week to $79.51 on the US Dollar Index (re-testing its YTD lows)

- The Currency Power Couple (Euro and Pound) were up another +0.3-0.4% last week to +1.9-3.0% YTD vs the Burning Buck

- European Stocks (EuroStoxx600) were up +1.3% last week (vs the Russell2000 +0.5%) to +2.9% YTD

- MSCI World Equity Index beat the Russell last week too, +1.2% = +1.8% YTD

- Canadian Stocks (TSX Composite Index) were up another +1.6% last week to +8.4% YTD

Blame Canada (who also had the “weather”, like the UK did – but didn’t spend the last 3 months blaming it like CNBC growth bulls have).

Now, if they can’t blame the weather for a 9-week high in US jobless claims (reported on Thursday, which isn’t a lagging jobs indicator), what precisely do you think they’ll start to blame as they cut their 2014 US GDP “forecasts”?

Alec, I’ll take US #InflationAccelerating for $500 (pre-tax!):

- Food Prices (CRB Foodstuffs Index) were up another +0.7% last week to a tasty +22.3% YTD

- Cattle Prices were up another +3.1% last week to +11.1% YTD

- Natural Gas Prices were up another +0.6% last week to +14.0% YTD

No worries though, the natural gas thing was all about the weather on the East Coast in February, right? If poor people being pulverized by food and shelter costs can’t afford the air conditioning this summer, tell them to go topless.

Cotton prices up another +1.1% last week to +12.3% YTD are prohibitive to wearing t-shirts anyway. After they eat an iPad, the median consumer in America (who makes $47,296.72 a year pre-tax and spends $42,996.83) can swallow Janet’s un-tapering reaction to slowing data, and like it.

Obviously this isn’t funny – an un-legislated Policy To Inflate (taxing 80% of Americans with QE on their cost of living) rarely is. Looking at the average American’s Spending Breakdown (slide 15 of our Q214 Macro Themes Deck):

- Housing = 29.2%

- Transportation = 17.6%

- Food = 12.5%

Yep, your un-elected Fed tells you all of that stuff is “non-core.” While food and shelter are primitive concepts for some, for most of us they are core costs. And since 30% of the country still rents, the all-time highs in US rents matters to real people with real costs too.

Oh yeah. I almost forgot to tie in the introduction of today’s note with the conclusion. Why is it that bond yields got slammed intraday on a “better than expected jobs report”? That’s easy. As opposed to being a backward-looking-editorial-passive-trend-follower, markets are forward looking.

My read-through on what both the bond and currency markets have been telling you for 4 months is that they’ll be telling you more of the same in the next 4 months. As growth slows, the Fed will get even easier à Dollar and Bond Yields fall further à Inflation continues to accelerate, and real growth consensus is un-friended, faster.

Our immediate-term Global Macro Risk Ranges are now as follows:

UST 10yr Yield 2.56-2.68%

SPX 1860-1888

RUT 1093-1133

USD 79.19-79.88

Gold 1291-1324

Corn 4.96-5.21

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer