We’re not as concerned as most with LVS’s covenant situation for 2009. LVS will cross that hurdle but it will come at a price.

At the end of the 2Q09, LVS was in compliance with its US and Macau credit facility covenants, albeit with little cushion. As wrote about extensively in “LVS: CREDIT OPTIONS AND OUTCOMES” on February 24, 2009, the covenant levels step down in 3Q09 for both the US and the Macau credit facilities, and continue to step down further in 2010. This is why investors are concerned.

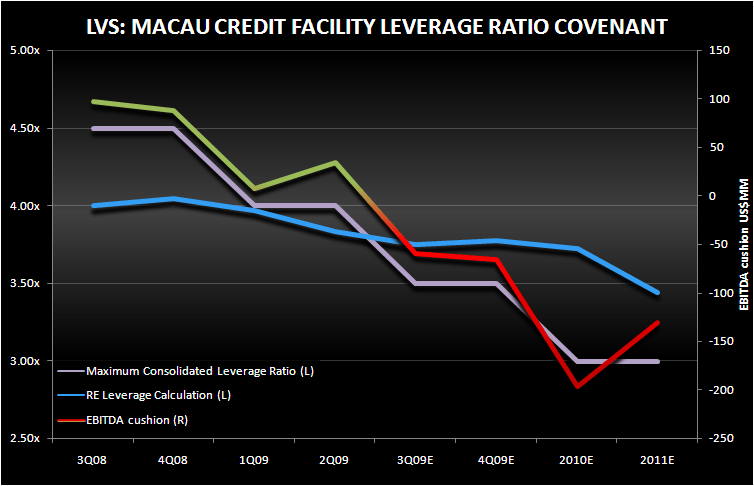

Macau Facility

We believe that LVS will be able to get an amendment in Macau, but at a price and with a “package of goodies” to the lender to boot. Given the low leverage on the Macau facility and the precedent of recent deals, we think that LVS should secure a fairly favorable deal. If only Sheldon could deliver on his promise to sell some non income producing assets, the cost would be limited. However, assets sales are unlikely in this market at the desired prices. An IPO cannot be floated until Q4 at the earliest but a definitive plan to IPO a minority stake in Macau would give the banks comfort and allow Sheldon still to restart construction on sites 5 & 6 in Macau. As we wrote about in “LVS: CHINA FORCING THE ISSUE”, Beijing may be twisting arms to get LVS the financing support it needs because they also want to see construction resume by year end.

In Macau, at the end of 2Q09, leverage stood at 3.8x versus a 4.0x covenant. There was $3.2BN of gross debt outstanding, and TTM EBITDA, for covenant compliance purposes, was $827MM. LVS paid down about $235MM of debt at the Macau subsidiary this quarter. As a reminder, the leverage test takes into account gross debt vs net debt in the US. At the end of the quarter, LVS had an EBITDA cushion of $35MM and a debt cushion of $138MM. Of course they also had $473MM of cash on hand at the Macau subsidiary, so real liquidity is closer to $600MM in Macau. In the 3Q09, the maximum leverage covenant steps down to 3.5x, which means that at $3.17BN of debt, LVS must have TTM EBITDA of $906MM to “clear” the covenant. We estimate that the TTM EBITDA will be $847MM, presenting a $60MM EBITDA problem for LVS. Alternatively, LVS can repay $210MM of debt in Macau, which they can do given the cash on hand. This may buy LVS some time, but the maximum permitted covenant steps down again in 2010 to 3.0x, meaning that on $3BN of debt LVS needs to generate over $1BN of TTM EBITDA.

With no new properties opening and additional competition coming from SJM (see “OCEANUS TO SINK SANDS MACAU” published on June 28, 2009) and WYNN, we are very skeptical that cost cuts alone will grow EBITDA by 20%.

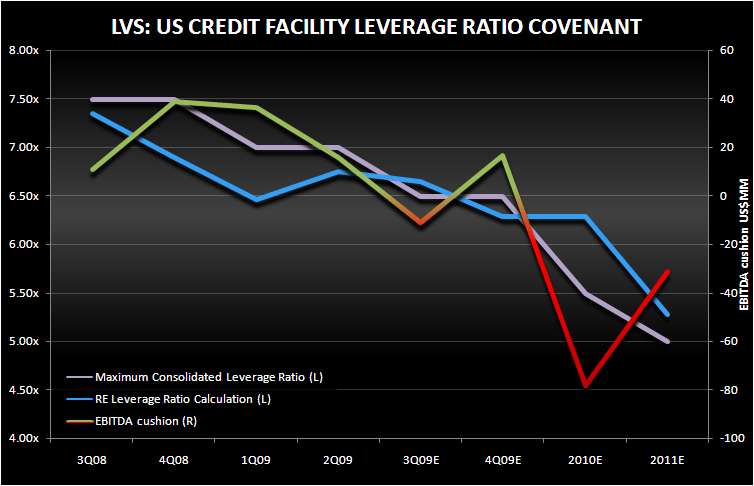

U.S. Facility

In the US, leverage was 6.8x versus a 7.0x covenant (net debt was $3.1BN and TTM EBITDA was $452MM). At the end of the quarter, LVS had a $16MM EBITDA cushion and $110MM debt cushion against its covenant. Next quarter, the maximum permitted leverage covenant steps down to 6.5x. In 2010, the covenant steps down to 5.5x and continues to step down to 5.0x in 2011 through maturity. There’s no question that when the agreement was originally crafted, Sheldon was relying on his “unique fundamental business plan by selling off our retail and our apartments and reducing or eliminating all our debt.” Unfortunately, for Sheldon and other real estate investors, that game of arbitrage worked well until the music stopped and suddenly there were no more buyers at “exaggerated prices”... leaving developers holding the bag.

To that end, we’re projecting TTM EBITDA improving to $490MM (as a reminder, Vegas suffered from very bad hold in 3Q08 and there will be pro-forma treatment for Bethlehem) and net debt of $3.3BN at the US subsidiary level, amounting to leverage of 6.7x versus a 6.5x covenant.

Since the breach is small, Sheldon could cure it by repurchasing up to $800MM LVS’s US bank debt. However, this strategy was significantly deleveraging when LVS’s bank debt was trading at 50% discount to par. Now that the credit markets have rallied, this strategy will be much less impactful with bank debt trading at 80 cents on the dollar.

We noticed that LVS pulled back (“deferred”) on capital expenditures this quarter, which should have been ramping into the opening of Singapore. If LVS plans to open Singapore on time, capex will need to ramp up and use some of the $2.6BN of cash that they are currently sitting on. 2010 is the year we are more concerned as the covenant issue gets worse 2010 with the step down. It will be tough to grow EBITDA with all the new high end product coming to Vegas next year (see “PLENTY OF ROOMS AVAILABLE AT THE STRIP INN IN 2010” published on July 17, 2009).