Conclusion

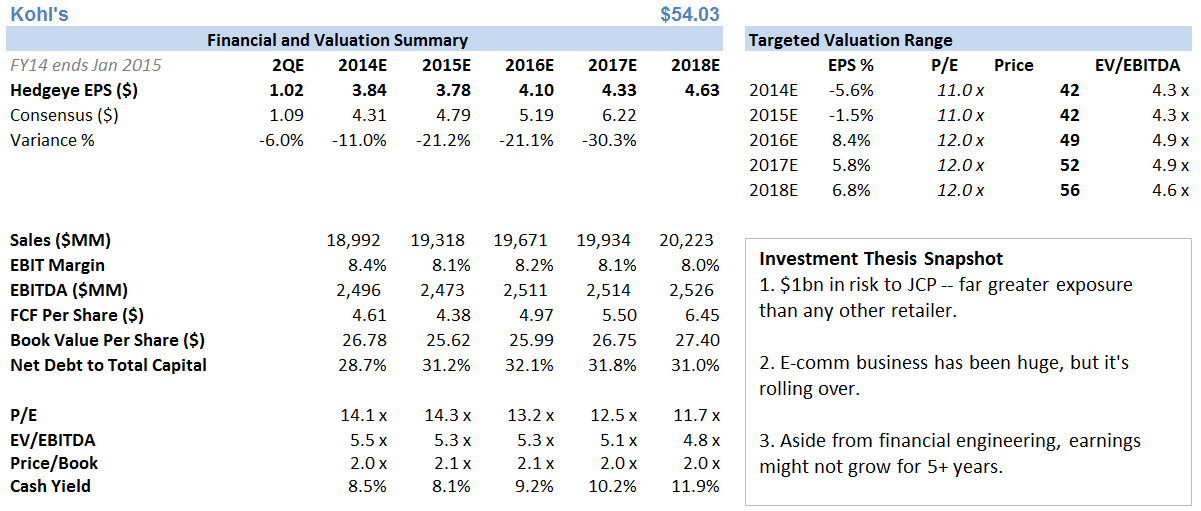

No change to our KSS Short Thesis. If anything, the lack of conviction and strategic thought process from management on the conference call reaffirmed our view that the problems at this company go far beyond a singular quarterly report. The weak comp (-3.4%) was not a major surprise given what we’ve seen out of other retailers, but even we didn’t think we’d see anything worse than -2.5%. What’s surprising is that the company held its full year EPS guidance constant despite the $0.03 miss.

We get the favorable impact of a lower tax rate and lower share count. But KSS is taking down D&A – which helps by $0.15 (or 3.7% EPS growth). Companies don’t make a decision to change depreciation rates so early in the year if they’re confident about where they’re headed. Also, KSS didn’t disclose its dot.com growth for the first time in at least three years. KSS has had the best growth rate in e-commerce out of any major retailer over the past eight years (38.9% CAGR) and it has served as a pillar of support for KSS’ growth algorithm. That’s clearly weakening.

And of course, JC Penney as an emerging competitive threat was not mentioned even once on the call. We think the Macro and industry cross currents are going to smack KSS from every direction, and we don’t think it sees it coming. We’re lowering our already below-consensus estimate for this FY by a nickel to $3.84. We don’t see how sales or margins are up for the year. In the outer years, we remain 20-30% below the consensus.

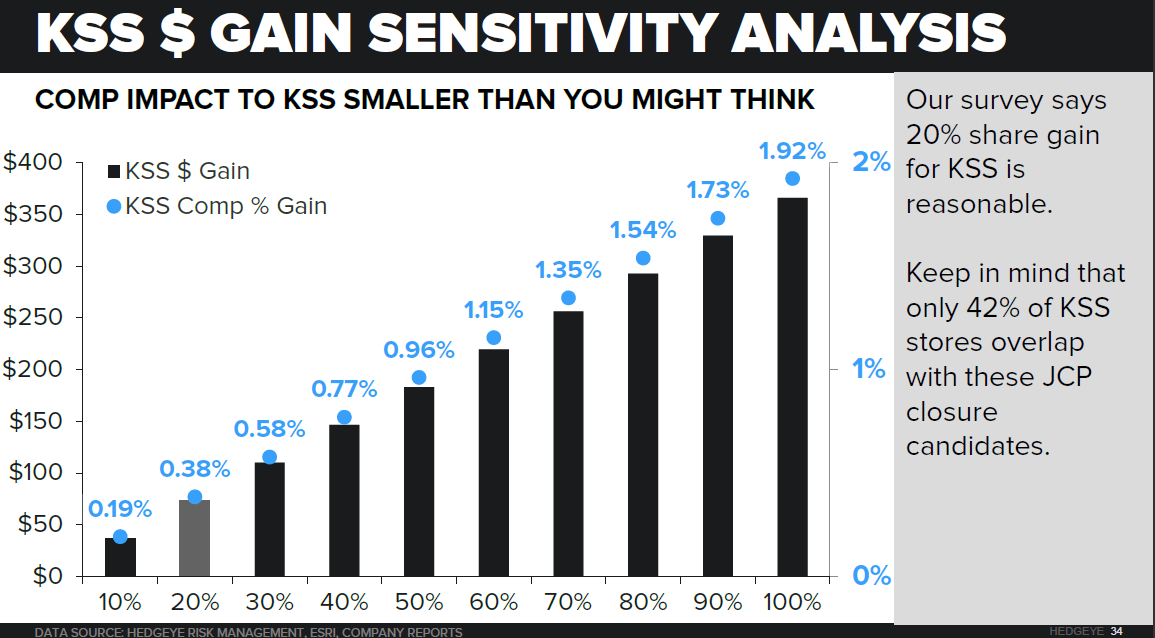

Here’s a few points relevant to KSS from our revenue overlap study from earlier this week regarding JCP and KSS. The punchline – based on a detailed analysis – is that JCP has about 300 stores to close. We overlapped each of those locations with every KSS store market by market to gauge the potential revenue windfall for KSS, as we viewed a meaningful revenue shift from JCP closures as one of the few risks to a KSS short. In the end, it was far less than we suspected.

1. Revenue Impact of Closures. Our math suggests that these stores would only result in about $550mm-$600mm in revenue loss to JCP. Importantly, KSS only overlaps in 42% of these markets. Our research shows that KSS took about 19% of the $5.4bn in sales JCP hemorrhaged over the past three years. If we apply a 20% share gain level to this analysis for KSS, it suggests about $73mm, or less than 0.4% to KSS in comp. If you want to get more aggressive and assume that KSS takes 100% of that revenue (which WMT won’t allow) you’re looking at about 1.9% in comp to KSS. We think something far below 1% is closer to reality. Here’s the sensitivity analysis below.

2. No Growth KSS. This analysis suggests to us that KSS can only add stores in lower demographic areas. We fully recognize that there are few people running around touting KSS as a unit growth story. But this math is definitely worth sharing. The numbers on the horizontal axis refer to JCP’s entire store base. The bucket to the far left is represents the most attractive demographic locations. The bucket to the far right represents the least attractive locations. The columns show the percent overlap KSS has in each bucket of those JCP stores. The point is that in the top 600 locations, KSS has near 100% overlap with JCP. Then it begins to tail down slightly – with the only real opportunity for growth in JCP’s worst 300-400 markets.

3. KSS Has The Greatest Exposure to JCP Prior (Not Future) Share Loss. Every time we conduct a survey, we look at the dispersion of the of the lost JCP business by retailer. We had a lot of people argue with us over the past two quarters when we presented our 18-19% share stat – but this time around, it was validated yet again. The numbers suggest that KSS captured about $1bn of the $5.4bn JCP gave away. WMT is slightly higher, but as it relates to percent of each retailer’s sales, no one even comes close to KSS at 5.3% of total sales.