Ron Ruggless of Nation’s Restaurant News published a relevant and timely article yesterday afternoon, highlighting the wave of private equity activity that hit the restaurant industry last year. David L. Epstein, principal with the Chapman Group, was particularly complimentary of the refranchising efforts of Applebee’s (DIN) and Wendy’s (WEN) in 2013. Similar to us, Epstein is surprised by the lack of transactions in 2014:

“I thought the huge success Wendy’s and Applebee’s have had in selling their corporate units to franchisees that a lot of other restaurants would see that and embark upon the same thing, but we haven’t seen that.”

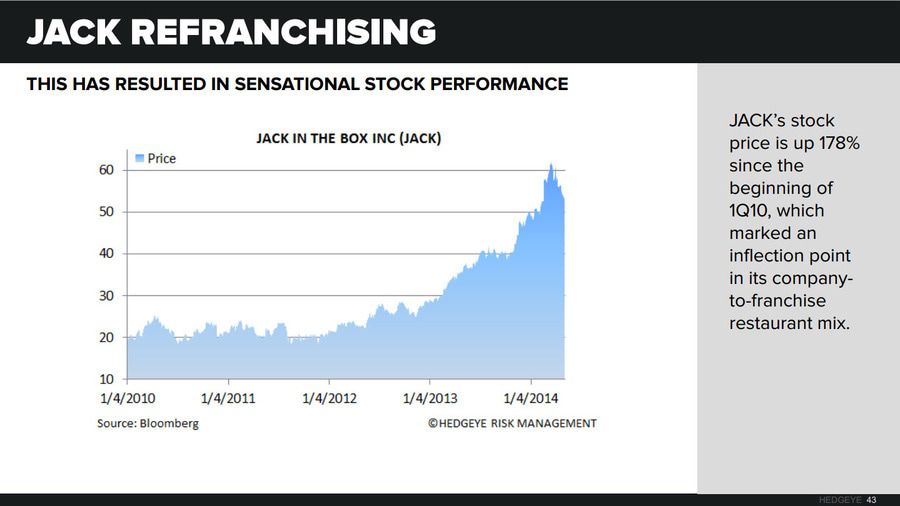

As you know, we’ve been strong advocates of a potential refranchising effort at Bob Evans Farms (BOBE), suggesting that the transition to an asset-light model would benefit the company greatly. We typically point to the successful restructuring Jack in the Box (JACK) has undergone over the past few years, but Applebee’s is another reminder of the significant value that can be created under such a scenario.

We continue to believe BOBE would benefit from a reliable, diversified revenue stream and lower-risk business. Suggestions that refranchising is merely a financial engineering event are heavily misleading. In fact, franchisees have been known to run better restaurants than the franchisors running the brand, which would hypothetically lead to improved sales, traffic and brand perception. BOBE would benefit greatly from finding a few franchisee partners to address the operational issues plaguing the company and recent history suggests there is significant appetite for these types of deals.

We surmise the appetite on Wall Street would be as strong – investors tend to favor asset-light operators, often awarding these companies with premium multiples. In our view, it’s a win-win.

Howard Penney

Managing Director

Fred Masotta

Analyst