Party Like It's 1999 ...

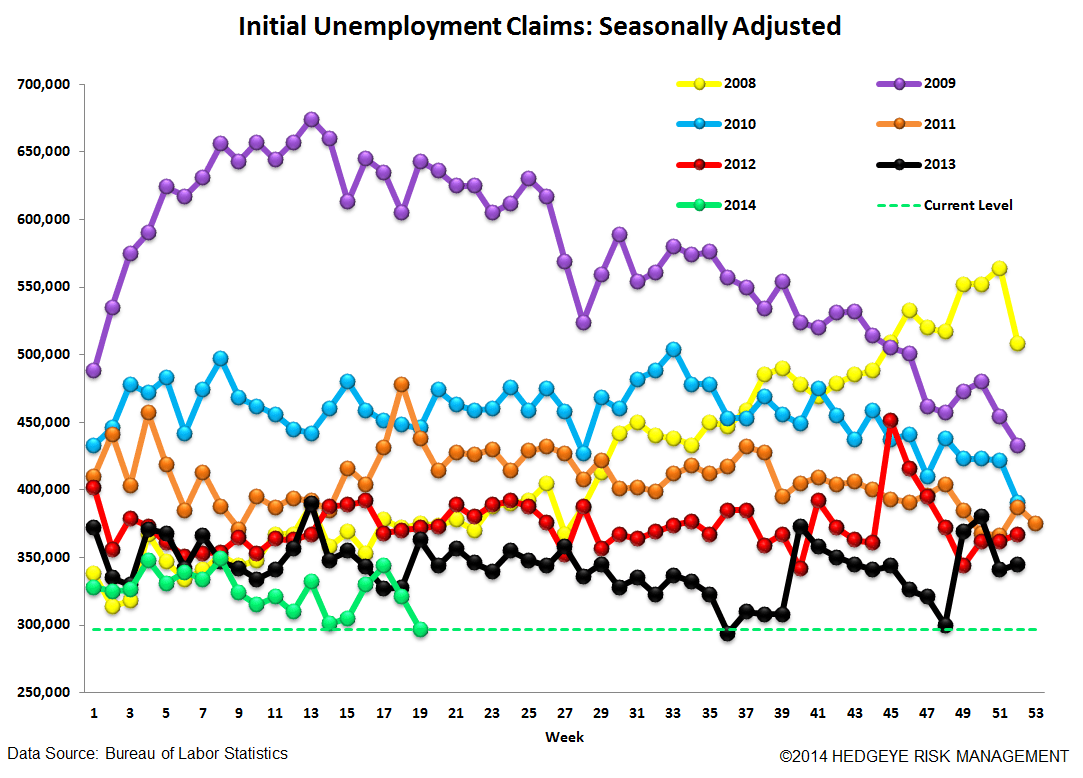

The labor market is heading very much in the right direction again. This morning's data marked just the second time since 2007 that the SA print came in below 300k. As the chart below shows, 300k is a Rubicon of sorts in that it has historically coincided with levels of near-peak employment such as 1999 and 2006. It's interesting to look at the contrast between then and now as the unemployment rate and NFP reports remain well off the levels seen in those respective timeframes. The disconnect has largely to do with the long-term unemployed, both those being counted in the data and those who've dropped out of the work force, either due to disability or otherwise. If one excludes those in the long-term unemployed category one finds that the labor market today is functionally similar to that last seen in the '99 and '06 periods, albeit with much more modest wage inflation. We would reiterate the question, however, that if claims are a measure of slack in the labor force and slack is tight it would seem reasonable to assume that wage inflation should be coming in the near future. The one wrinkle here remains housing, which is showing plenty of signs of ongoing deceleration.

The Data

Prior to revision, initial jobless claims fell 22k to 297k from 319k WoW, as the prior week's number was revised up by 2k to 321k.

The headline (unrevised) number shows claims were lower by 24k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2k WoW to 323k.

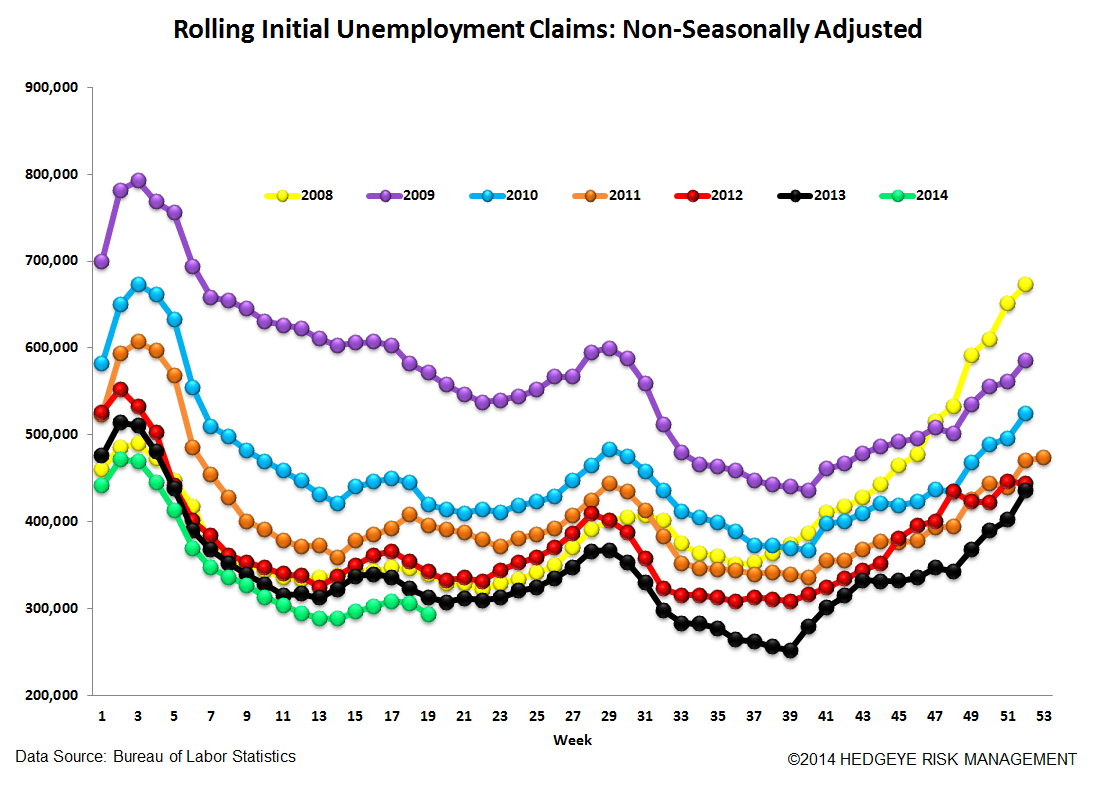

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -6.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -5.2%

Yield Spreads

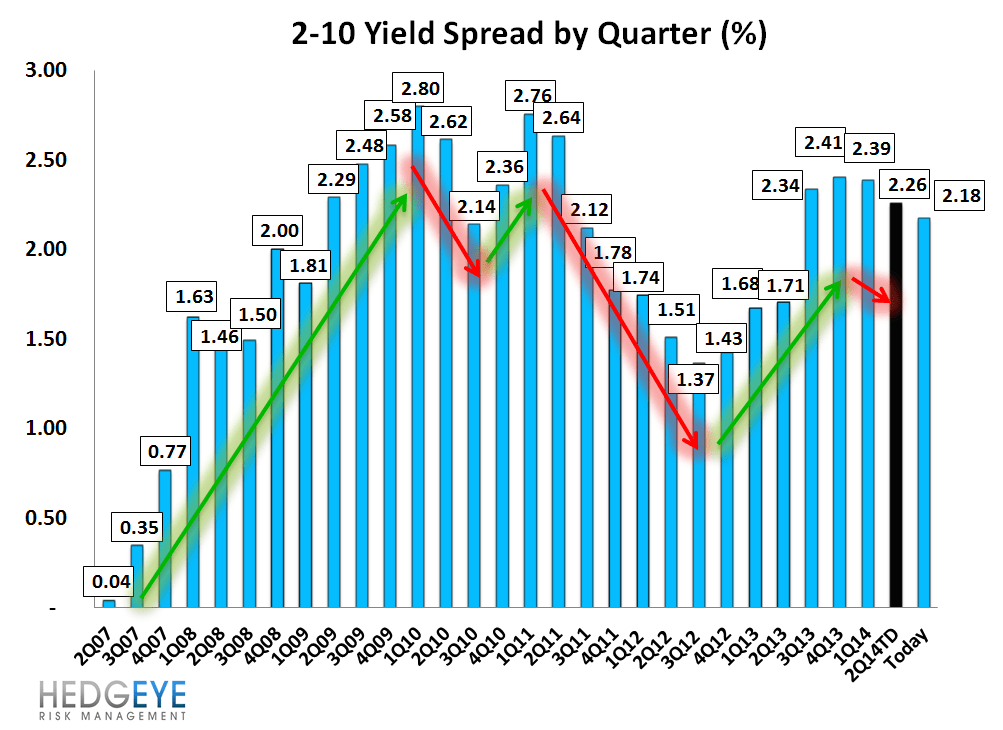

The 2-10 spread fell -1 basis points WoW to 218 bps. 2Q14TD, the 2-10 spread is averaging 226 bps, which is lower by -13 bps relative to 1Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT