TODAY’S S&P 500 SET-UP – May 15, 2014

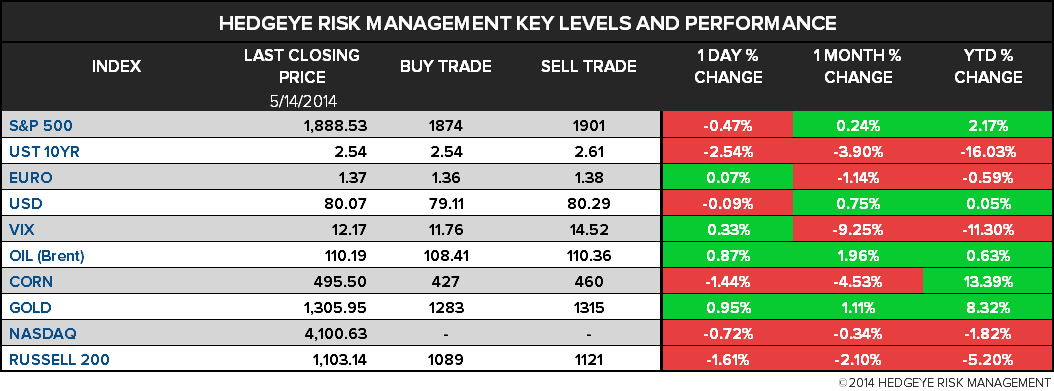

As we look at today's setup for the S&P 500, the range is 27 points or 0.77% downside to 1874 and 0.66% upside to 1901.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.17 from 2.18

- VIX closed at 12.17 1 day percent change of 0.33%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: Empire Manufacturing, May, est. 6 (prior 1.29)

- 8:30am: Fed’s Dudley speaks in New York

- 8:30am: Consumer Price Index, April, est. 0.3% (prior 0.2%)

- CPI Ex Food and Energy, April, est. 0.1% (prior 0.2%)

- 8:30am: Initial Jobless Claims, May 10, est. 320k (prior 319k)

- Continuing Claims, May 3, est. 2.690m (prior 2.685m)

- 9am: Net Long-term TIC Flows, March est. $40b (prior $85.7b)

- Total Net TIC Flows, March (prior $167.7b)

- 9:15am: Industrial Production, April, est. 0.0% (prior 0.7%)

- Capacity Utilization, April, est. 79.1% (prior 79.2%)

- Manufacturing (SIC) Production, April, est. 0.3% (prior 0.5%)

- 9:45am: Bloomberg Consumer Comfort, May 11 (prior 37.1)

- 10am: Philadelphia Fed Business Outlook, May, est. 14.0 (prior 16.6)

- 10am: MBA Mortgage Delinquencies, 1Q (prior 6.39%)

- Mortgage Foreclosures, 1Q (prior 2.86%)

- 10am: NAHB Housing Market Index, May, est. 49 (prior 47)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- TBA: Commerce Dept. issues benchmark revisions on factory orders, etc.

- 6:10pm: Fed’s Yellen speaks in Washington

GOVERNMENT:

- Senate in session, House out

- President Obama speaks at National Sept 11th Memorial/Museum

- 10am: Senate Banking Cmte marks up housing finance bill; 538 Dirksen

- 10:30am: Sens. Durbin, Harkin, Murphy, Schatz, hold news conf. w/Young Invincibles to call on Education Dept to put stronger student protections for-profit college career ed pgms

- 10:30am: FCC set to decide whether to start writing open-Internet rules .

- Also considering policies, rules for broadcast TV spectrum incentive auction, aggregation spectrum rules for mobile wireless services

- U.S. Trade Representative Michael Froman visits China to talk with officials ahead of APEC Trade Ministers meeting in Qingdao

- U.S. ELECTION WRAP: Bill Clinton on Immigration; Democrats’ Ads

WHAT TO WATCH:

- Europe economy underperforms with weakness from France to Italy

- FCC to decide whether to write open-Internet rules

- France fortifies anti-takeover tool as GE-Siemens eye Alstom

- Cisco sales forecast tops ests. as Chambers seeks turnaround

- 13F deadline: Ackman, Buffett, Peltz to divulge holdings

- JPMorgan, Citigroup, others release monthly delinquencies

- CFTC reviews U.S. banks’ overseas trading for possible evasion

- Carlyle’s Rubenstein speaks as SALT Conference continues

- Changes announced for MSCI country index shuffle

- AstraZeneca cancer drug coveted by Pfizer shows promise in trial

- Senators ask for anti-trust review on PFE, AZN plan: Reuters

- Times Co. publisher said to always have clashed with Abramson

- Wynn, MGM plan Japan IPOs to fund casino projects

- Teva loses suit seeking to block FDA generic Copaxone approval

- Musk sees need for multiple “gigafactories” for battery demand

- Japan’s economy accelerated in 1Q before tax rise

- Senate Banking Cmte marks up Fannie Mae reform bill

- Murphy Oil looking to sell stake in Malaysian assets: WSJ

EARNINGS:

- Advance Auto Parts (AAP) 8:30am, $2.15

- Air Canada (AC/B CN) 6am, C$(0.48) - Preview

- Alliant Techsystems (ATK) 7am, $2.40

- Applied Materials (AMAT) 4:02pm, $0.28

- Autodesk (ADSK) 4:01pm, $0.21

- CA Inc (CA) 7am, $0.59

- CAE (CAE CN) 8:40am, C$0.20

- Flowers Foods (FLO) 6am, $0.30

- J.C. Penney (JCP) 4pm, $(1.22) - Preview

- Kohl’s (KSS) 7am, $0.63 - Preview

- Nordstrom (JWN) 4:04pm, $0.68 - Preview

- Power of Canada (POW CN) 2pm, C$0.61

- Prestige Brands (PBH) 6am, $0.33

- Teekay (TK) 8:30am, $(0.18)

- Wal-Mart Stores (WMT) 7:02am, $1.15 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel Plunges Most in 31 Months as Surge Judged to Be Overdone

- WTI Drops From Three-Week High as Stockpiles Gain; Brent Steady

- China Aluminum Sales for Beer Cans Foiling Deficit: Commodities

- Gold Below One-Week High as U.S. Outlook Weighed Against Ukraine

- Coffee Advances as Brazilian Output Seen Lower; Sugar Retreats

- Wheat Extends Longest Slump Since November on Ample World Supply

- Gold Sales Drop in Hong Kong Seen Signaling Lower Chinese Demand

- Steel Rebar Falls to Record Low as Chinese Mills Increase Output

- London Metal Exchange Gets Permission to Appeal Warehouse Ruling

- IEA Sees Higher Demand for OPEC Crude Amid Inventory Deficit

- Moscow Hosts Summit as Gazprom Warns Ukraine on Gas Cut: Energy

- Chocolate Consumption in Indonesia Seen Doubling in Three Years

- Long-Run Coking Coal Demand Underpinned by Steel, Urbanization

- Pemex May Struggle to Keep Output as Mexico Debates Energy Laws

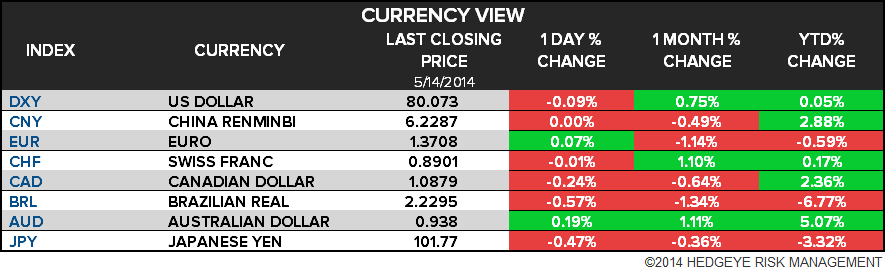

CURRENCIES

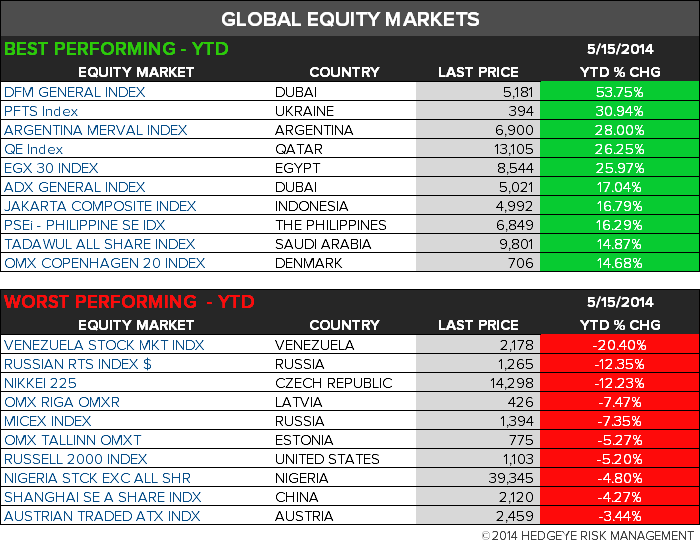

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

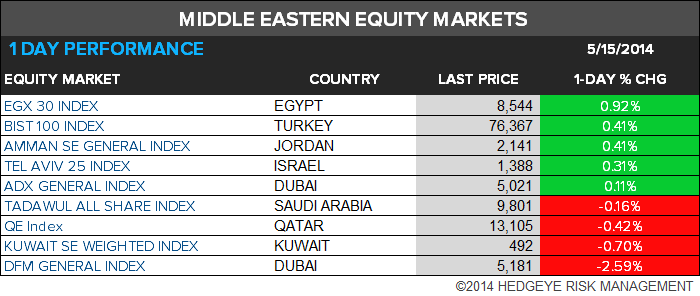

MIDDLE EAST

The Hedgeye Macro Team