Here’s another theme with meaningful impact on the footwear space, which I think helps Payless over the next two years. Wal*Mart has covertly indicated over the past month that it is increasingly downsizing its presence in the footwear space to concentrate on more profitable offerings.

Here’s the math… Wal*Mart did $306bn in the US last year. About 11% of that was apparel, footwear, and accessories. Only about 100bps-200bps was driven by footwear, which suggests about $5bn annually. For what it’s worth, Zappos generated $1bn in gross sales last year. Yes, Zappos is bigger than one might think.

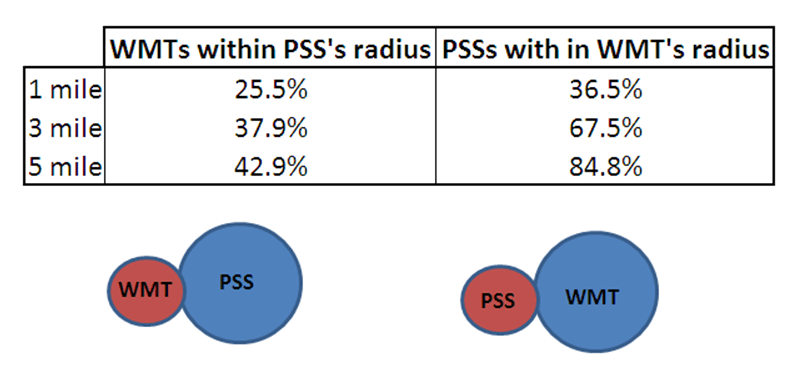

But where Zappos and Wal*Mart don’t compare is on price point – where Zappos is over 2x the $9.98 average price at WMT. Who does compete? You guessed it…Payless. Check out the table below. It shows that a quarter of Payless stores have a Wal*Mart within a mile radius. 43% have a WMT within 5 miles.

Let’s say Wal*Mart scales down footwear to 1% of sales over 3 years as it cycles through its remodel process. That suggests over $2bn is up for grabs. If I take it a step further and assume that 38% is within reach (within a 3-mile radius), then that’s $760mm. If PSS grabs only 10% of that, it would be a 3% comp alone. At a 30% incremental margin, we’re talking $0.23 per share. That’s off a base of $1.06 last year.

Talk about leverage…