Although selling off sharply from the highs, Nickel has gone on a huge run over the last week to touch two-year highs on healthy volumes. The snapshots below from yesterday's close provide a good visual for the magnitude of the recent move. The volume table represents all active nickel contracts traded.

Without drawing any unfounded causality, a few data points surrounding the recent volatility are included below:

- Last week VALE SA, one of the top 3 Nickel producing companies in the world, suspended its operations off the coast of the South Pacific Island of New Caledonia after a contaminants spill

- BHP Hilton has recently announced its intent to sell its Nickel unit. To put a perspective on the margin pressure they have dealt with, the company’s net margin for the year through June 2013 from its Nickel unit was 1.8% vs. 41% in 2007

- Supply concerns surrounding the Indonesian export ban along with the Russian/Ukrainian conflict have fueled supply concerns:

An axiomatic geopolitical dynamic may exist behind Indonesia’s ban of two major minerals in January, nickel ore and bauxite (commercial ore of aluminum). Two Russian companies, Rusal and Norilsk Nickel, the world’s largest aluminum and Nickel companies respectively, made a deliberate push for Jakarta to pass a controversial mineral ore export ban despite opposition from domestic mining companies and Asian buyers. The campaign was viewed as a positive for both parties at the expense of other global players in the space, namely China, Japan, and the U.S. Company personnel from both Rusal and Norilsk traveled to Indonesia repeatedly last year during a 6-month campaign in which they only agreed to spend billions of dollars on smelters if Indonesia banned nickel and bauxite exports.

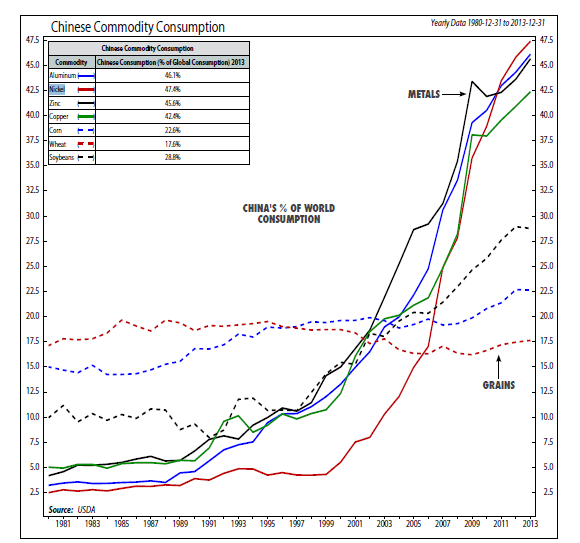

Although China is becoming a significant trading partner with Russia, they will undoubtedly face supply constraints. China currently consumes 47.4% of Nickel produced globally:

The campaign by Rusal and Norilsk was aimed at replacing costly capacity in Russia. The current regime in Indonesia has emphasized the need to earn more form its mineral resources. The export ban will force domestic mining companies to move up the production chain by pushing the processing of the minerals excavated. Jakartra denies having been influenced by either Russian company.

The ban will halt approximately $3Bn of annual exports and has probably helped propel Nickel higher this year (+45% YTD). The shares of both companies quickly rose over 10% in less than a month after the news hit. China and Japan are two of the largest buyers of Indonesian nickel ore, and Beijing is organizing a delegation of Chinese firms to travel to Jakarta to discuss the newly implemented rules. Japan is considering taking the Indonesian export ban to the World Trade Organization. The move has also hurt U.S. miners in Indonesia. Freeport-McMoRan and Newmont Mining Corp have now halted shipments and cut output due to a dispute over an escalating export tax under the new rules.

Macro Team