Today we hosted a call to discuss our short thesis on KSS, and why JCP is both the biggest opportunity and threat to the thesis. While we presented the results of our third department store consumer survey and our e-commerce analysis (both very insightful), we think that the meat of our presentation was in our analysis of the real estate and demographics for every single one of the stores for JCP and KSS. The conclusions are significant. We outlined our research in a 47-page slide deck, and can’t possibly encapsulate all of that here. But here are some of the more salient points. For the full deck and audio presentation, click the link below.

- Audio Link: CLICK HERE

- Materials Link: CLICK HERE

Here are a few select highlights…

1. Real Estate Approach: We think that the biggest threat to a KSS short is JCP announcing a significant number of store closures, which would presumably help KSS longer term as it relates to market share. In order to properly assess this risk, we analyzed every JCP market to see where the most likely closures are, and whether or not they overlap with KSS. For starters, we did not simply map out store locations (a feat in itself) and draw a circle around each point on the map to gauge overlap by market. We mapped out a 15-minute driving radius around every store, which as you can see by the chart below is very different for every single store location in the country. This shows Tallahassee, FL, which has two locations where JCP and KSS overlap perfectly, and another location where JCP exists without KSS as a competitor. We did this in every market in the US.

2. Productivity Analysis. This next chart shows us what the implied sales per square foot range is for JCP’s 1089 stores. What we know is that in the US, JCP has 0.47% share of wallet in apparel, home furnishings and other relevant retail goods across its portfolio in aggregate – again, we’re looking at all expenditures within a 15 minute drive of its stores. If we apply that ratio to each market, we get implied sales/square foot levels ranging from $8 to nearly $1,000 (Manhattan). We know that share is likely to vary by market, so we’re not trying to say that these are the exact productivity levels of each store. But directionally, we think we’re right. And that direction tells us that 782 stores, or nearly 72% of JCP locations, are running below the system average of $98/square foot.

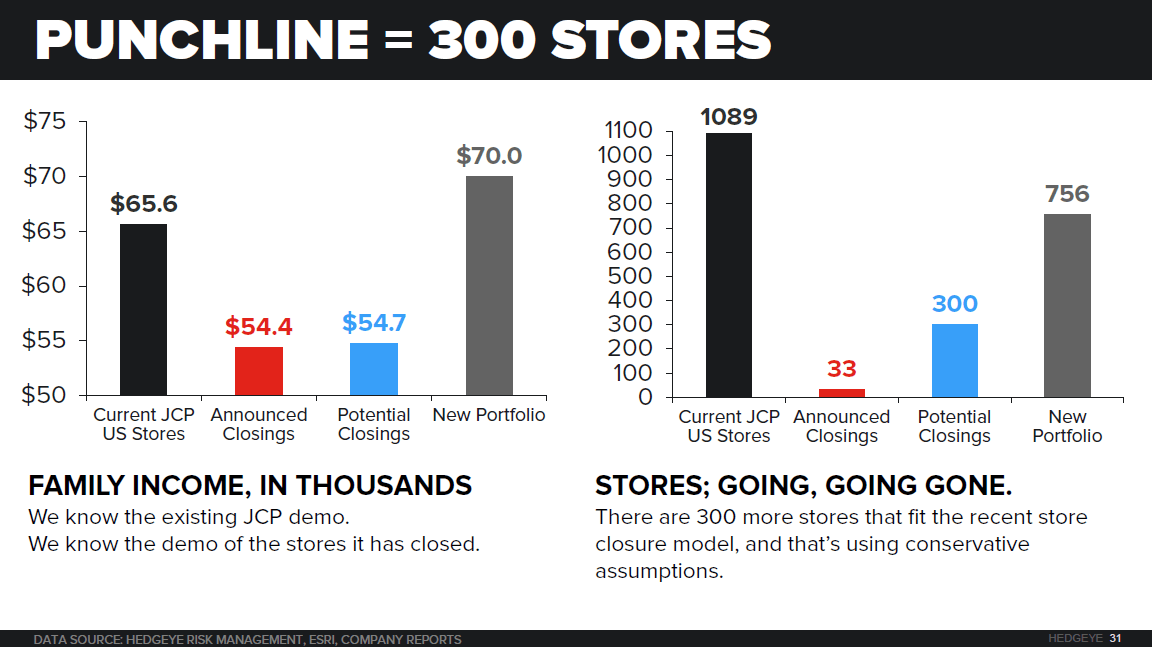

3. 300 Store Closures: We think that JCP needs to close 300 locations, at a minimum. We know that the demographic profile in the surrounding area of JCP stores in aggregate is about $66k in annual household income. We also know that JCP just identified 33 stores that it is closing. We analyzed those locations, and the demographic profile is $54k annually – that’s 18% lower than the portfolio average. So we looked throughout the system of JCP stores and looked to see how many other stores fit that profile. There are 300. If these stores are closed, the average income statistic goes up for the whole portfolio by 7% to $70k. The 300 stores closed have implied sales/square foot of less than $38 annually. There are still almost 500 stores above $38 and yet still below the system average.

4. Revenue Impact of Closures. Our math suggests that these stores would only result in about $550mm-$600mm in revenue loss to JCP. Importantly, KSS only overlaps in 42% of these markets. Our research shows that KSS took about 19% of the $5.4bn in sales JCP hemorrhaged over the past three years. If we apply a 20% share gain level to this analysis for KSS, it suggests about $73mm, or less than 0.4% to KSS in comp. If you want to get more aggressive and assume that KSS takes 100% of that revenue (which WMT won’t allow) you’re looking at about 1.9% in comp to KSS. We think something far below 1% is closer to reality. Here’s the sensitivity analysis below.

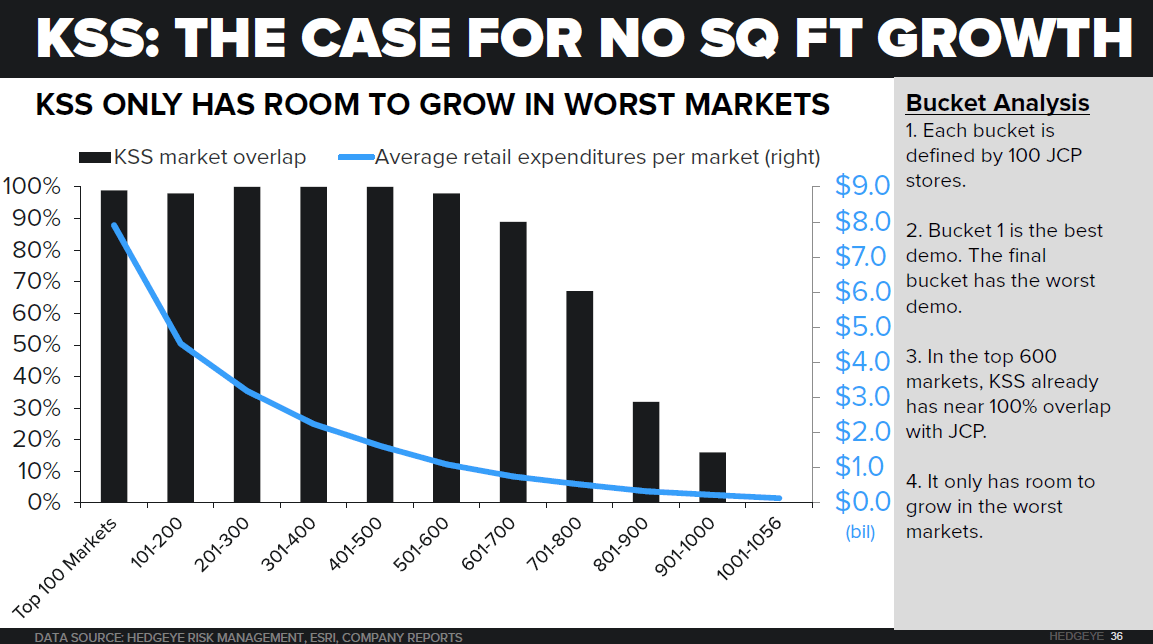

5. No Growth KSS. This analysis suggests to us that KSS can only add stores in lower demographic areas. We fully recognize that there are few people running around touting KSS as a unit growth story. But this math is definitely worth sharing. The numbers on the horizontal axis refer to JCP’s entire store base. The bucket to the far left is represents the most attractive demographic locations. The bucket to the far right represents the least attractive locations. The columns show the percent overlap KSS has in each bucket of those JCP stores. The point is that in the top 600 locations, KSS has near 100% overlap with JCP. Then it begins to tail down slightly – with the only real opportunity for growth in JCP’s worst 300-400 markets.

6. KSS Has The Greatest Exposure to JCP Prior (Not Future) Share Loss. Every time we conduct a survey, we look at the dispersion of the of the lost JCP business by retailer. We had a lot of people argue with us over the past two quarters when we presented our 18-19% share stat – but this time around, it was validated yet again. The numbers suggest that KSS captured about $1bn of the $5.4bn JCP gave away. WMT is slightly higher, but as it relates to percent of each retailer’s sales, no one even comes close to KSS at 5.3% of total sales.

7. Shopping Trend Getting Better On The Margin for JCP. There’s half a dozen slides in our deck outlining results of our consumer survey. In this one we ask people if they are buying more or less vs. a year ago at each store. Now with three surveys under our belt to an identical demographic group each time, we can at least compare the retailer sentiment to prior surveys to game the incremental change. Bottom line is that JCP is showing steady improvement, while KSS is not.

Please see the link to the presentation materials above for all of our analysis on these and other topics.