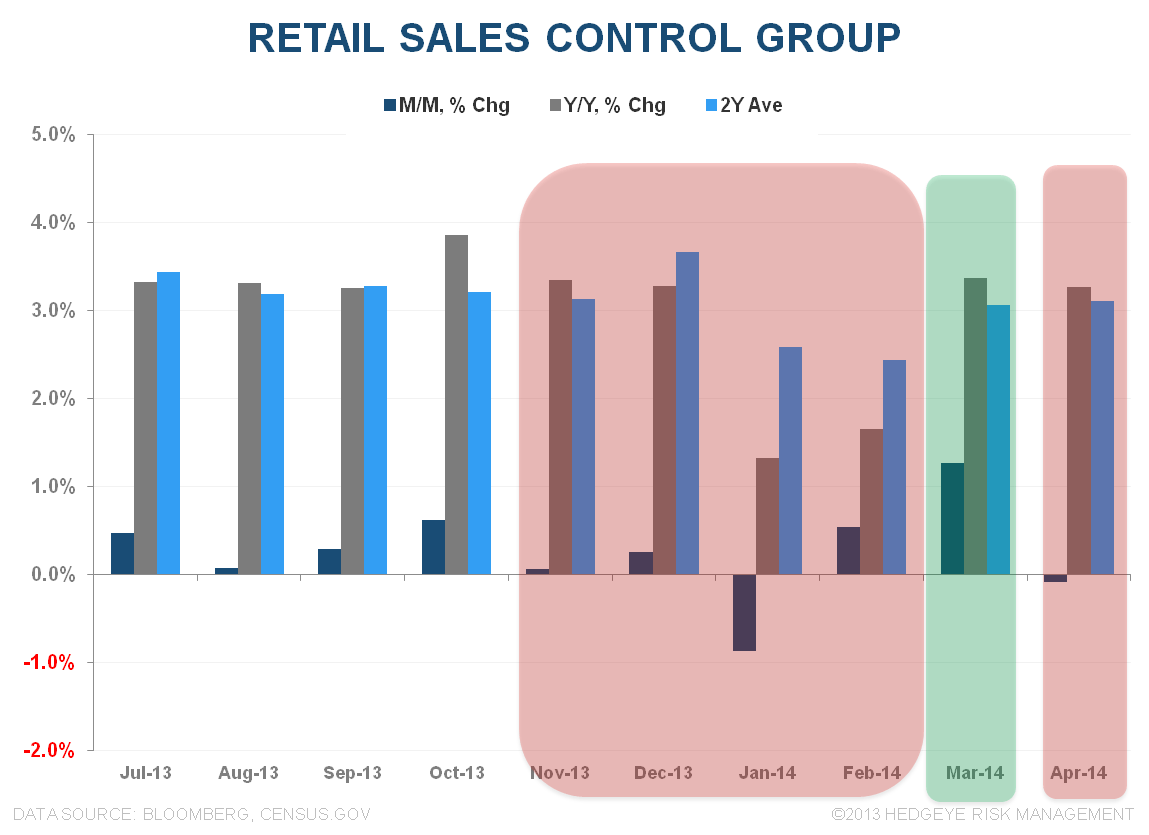

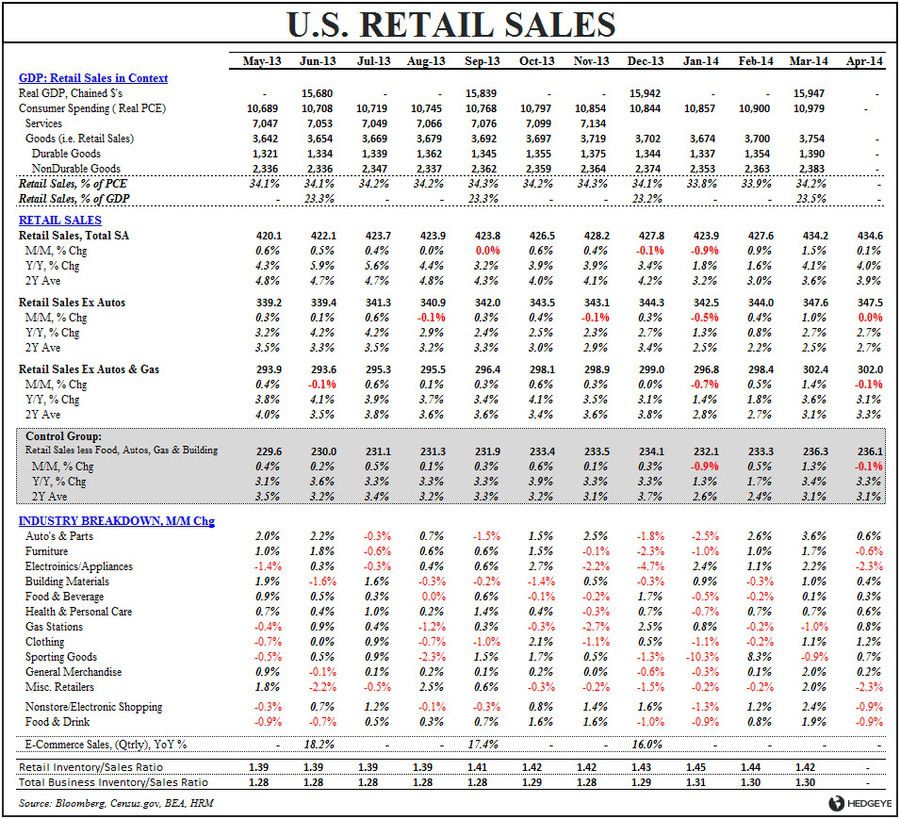

Headline Retail sales grew +0.1% sequentially while the Control Group measure (GDP input) declined -0.1% sequentially with electronics spending and the e-sales and dining-out proxies each decelerating on a MoM, YoY and 2Y basis.

The positive revision to the march data will help drag 1Q GDP back to positive territory but the early read through for reported 2Q growth is less sanguine – particularly in the context of consensus estimates which have increased ~20% over the last month to +3.3%.

Meanwhile, sales-to-Inventory ratio’s continue to peak despite the spread between nominal spending and nominal earnings growth re-expanding in recent months.

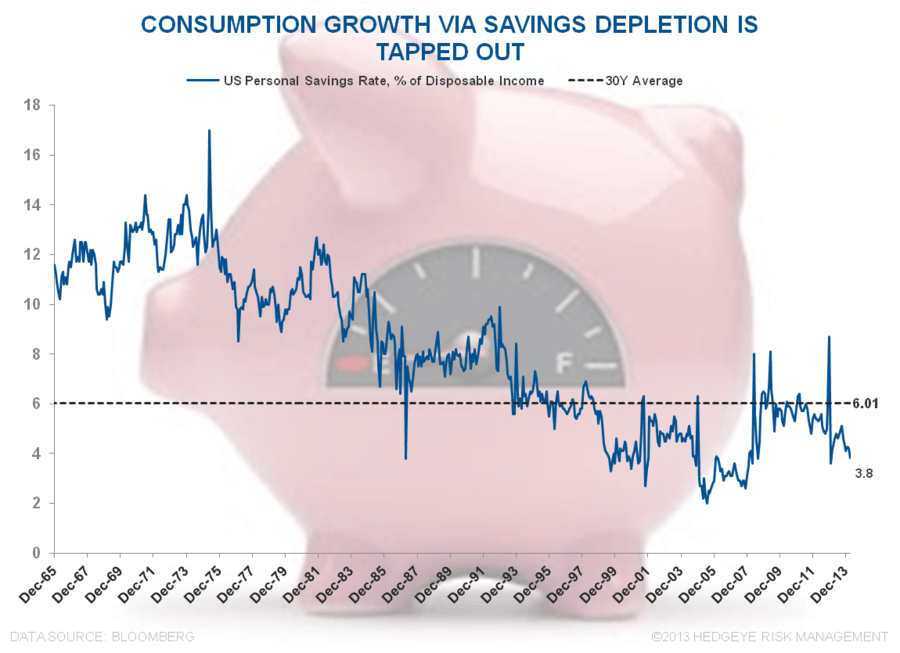

With wage growth running sub-2% and savings rates at a cycle low (& the very low end of the historical range) the upside to consumption growth over the immediate/intermediate term remains very much constrained, in our view.

In short, with the ~24% of the domestic economy that is retail sales off to an inauspicious start, consumption has some significant hay to bale in order to best rising consensus growth expectations and re-capture last year’s slope of growth.

With the dollar and 10Y broken and food/energy/housing inflation taking down a greater share of wallet, we're not convinced that consumption acceleration materializes.

Christian B. Drake

@HedgeyeUSA