This note was originally published at 8am on April 29, 2014 for Hedgeye subscribers.

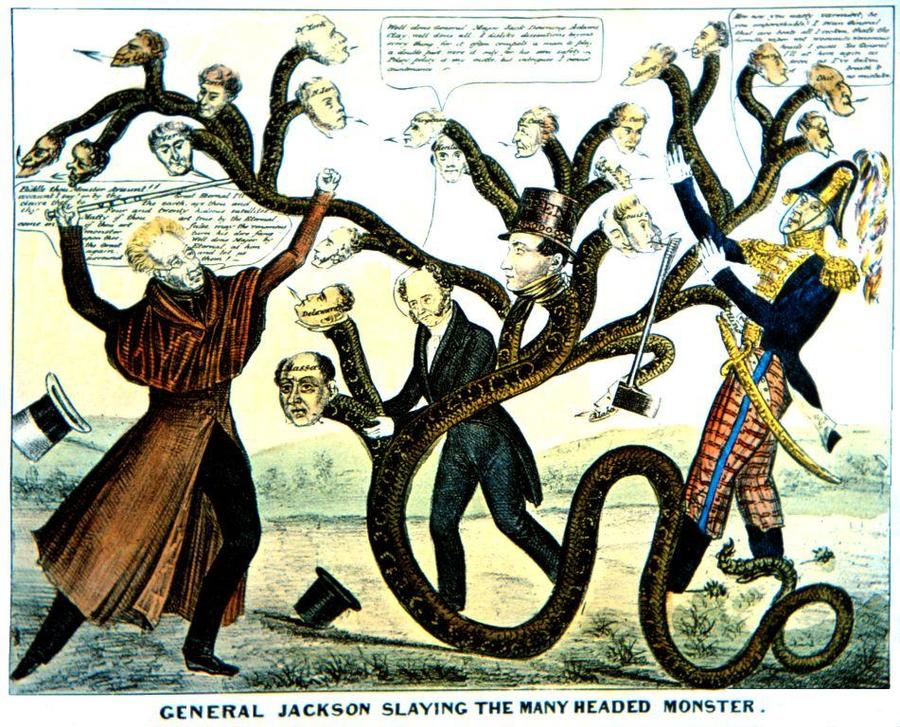

“The monster is trying to kill me, but I will kill it.”

-Andrew Jackson

That sounds pretty hard core; especially coming from the President of the United States!

“The Monster, formally known as the Second Bank of The United States (and more commonly as the Bank), originated as the brain child of Alexander Hamilton… Jackson saw himself in arms against the dragon, an infernal, demonic entity that must be destroyed.” (The First Tycoon, pg 93)

And you thought I was bearish on the un-elected and un-accountable US Federal Reserve. As I was flying from Indianapolis, IN to Minneapolis, MN last night reading this, I pulled the Delta Airlines polyester red blanket up to my chin and asked the flight attendant for cookies and milk.

Back to the Global Macro Grind…

#ScaryMonster, this US Policy To Inflate has become. The more I travel and talk this through with investors, the less convinced most are that this ends well. There’s no irony in that. Unless it’s “different this time”, burning the credibility of a country’s currency has never worked, for any country.

If I’m right and 2014 US GDP growth (real, not nominal) is closer to 1-2% than the 3-4% consensus economists and perma bulls alike are expecting, I think the societal side to this risk starts to kick in. That’s because what gets us to 1-2% is #InflationAccelerating. And nothing kills The People’s confidence more than a government that they think is lying to them.

“In 1832… so began the Bank War; the result of not merely Jackson’s obsessions, but the cultural crisis of the times. It broke out because two great waves now crashed into one another: the individualistic, anti-aristocratic, competitive impulse fostered by the Revolution, and the instinct to organize, amalgamate, develop, and bring order to the chaos of the marketplace.”

Sound familiar?

“Indeed, out of this conflict would emerge a new American economic outlook; a culture that embraced equality of opportunity and fierce competition, as well as sophisticated business institutions.” (The First Tycoon, pg 95)

Sophisticated about applying chaos theory and non-linear risk analytics to their linear models, the Fed and Old Wall Street are not. I think they might be getting dumber (see Bank of America (BAC) yesterday, who had to report that they miscounted the moneys, again!).

That’s one of the reasons why the Financials (XLF) got tagged for a -0.6% loss yesterday (with the SP500 +0.3% on the day). What’s happening out there at both the sector and style factoring levels of the market is crystal clear – it’s called variance:

- Variance rises during market phase transitions (i.e. from US #GrowthAccelerating in 2013 to inflation slowing growth in 2014)

- Variance plummets when you can literally buy anything (because everything goes up)

For the US stock market, the so-easy-a-monkey-can-do-it (low-variance) environment ended on December 31, 2013. Here’s what I mean by that if you look at the variance in yesterday’s US stock market move:

- Financials (XLF) -0.6%

- Biotech (IBB) -0.4%

- Russell2000 (IWM) -0.4%

Versus:

- #YieldChasing Consumer Staples (XLP) +1.1%

- Slow-growth-yield chasing Utilities (XLU) +0.5%

- Energy #InflationAccelerating (XLE) +0.2%

That’s why I said it in my investor meetings yesterday in Indy and I’ll say it again in Minneapolis to long-only risk managers today – if you want to be invested alongside our 2014 Macro Themes, you:

- Buy Inflation (XLE, DBA, COW, CAFÉ, TIP, etc.)

- Buy Slow-Growth Yield Chasing (XLU, TLT, BND, etc.)

- Buy late cycle companies that can jam customers with pricing (VNQ, XLI, etc.)

If you are a Global Investor, this gets a lot easier – mainly because you can not only be long US #InflationAccelerating but you can buy countries who are doing the right thing from a protecting-the-purchasing-power-of-the-people (read: #StrongCurrency) perspective.

At the top of that list is the UK:

- The British Pound continues to pound the pig that is the US Dollar (GBP +10% vs USD in the last 6 months)

- UK GDP Growth for Q114 was reported +3.1% y/y this morning – a fresh new #GrowthAccelerating high

Newsflash: the UK had the “weather” too. They just don’t have to blame the weather in order to CTA (substitute T for Y) on why almost every one of them (consensus economists from Old Wall and Washington) had their Q114 US growth forecast dead wrong.

Sadly, tomorrow the United States of America will report a GDP growth rate for the 1st quarter that is maybe 1/2 of what the United Kingdom just did. Sure, you’ll have month-end markups in the US stock market … and the Fed will release their 2nd or 3rd coming of Christ…

But once that storytelling is done with, Americans will go back to eating it – the Policy to Inflate, that is. And if we don’t have the courage to kill this broken and un-elected US economic policy, The Monster of a devalued currency might just eat us too.

Our immediate-term Global Macro Risk Ranges are now as follows:

Nasdaq 4006-4143

USD 79.21-79.99

Pound 1.67-1.69

Natural Gas 4.55-4.81

Gold 1280-1310

Corn 5.05-5.19

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer