BLMN remains on the Hedgeye Best Ideas list as a SHORT.

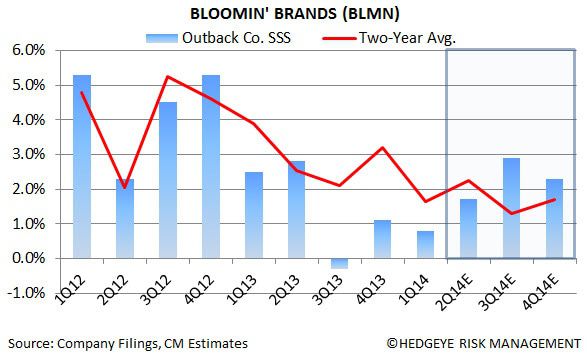

BLMN reported underwhelming numbers this morning, missing both top and bottom line estimates by 69 bps and 288 bps, respectively. Same-store sales across all four main concepts decelerated on a two-year basis in 1Q14, despite initiatives aimed at stemming this decline. Traffic trends remain anemic, although they continue to outpace the casual dining industry according to Knapp Track data. This is to be expected, as weekday lunch continues to rollout across Carrabbas and Outback restaurants. Management maintained full-year guidance of 1-2% comp growth for its core domestic brands and GAAP diluted EPS of at least $1.21 on a calendar basis. Trends will need to accelerate meaningfully throughout the rest of the year in order for BLMN to hit the numbers. The real disconnect, however, comes in FY15 with the street expecting 20% EPS growth on 7% EPS growth. These numbers are far too high and will be revised down, over time, as this becomes a realization.

We continue to believe the casual dining industry is in secular decline. In the new era of casual dining, companies with large, diverse portfolios are at a structural disadvantage to smaller, more nimble players. Darden is currently having issues operating its vast array of brands and we believe Bloomin’ is on a similar path. As it stands, Bloomin’ has some of the worst operating margins in the entire restaurant industry. Despite claims of significant efficiencies, its profit margins have essentially remained flat since the beginning of 2011.

Aside from taking issue with the structure of the company, we continue to question the strategic rationale behind the company’s capital allocation decisions. Management seems intent on maintaining its unit growth story, despite less than desirable results. Carrabbas, for example, should not be growing at all. Recognizing a problem and not immediately addressing it is a flawed strategy that will inevitably come back to haunt the company.

What We Liked:

- Outback Steakhouse same-store sales growth of +0.8%

- Interior remodel at Outback complete, exterior remodel underway

- Currently rolling out Saturday lunch at Bonefish Grill; new core menu coming in 3Q

- Brazil same-store sales and cash flow generation remain strong

- Maintained +2-4% commodity inflation outlook; majority of 2014 needs are locked

What We Didn’t Like:

- Two-year same-store sales decelerating across four core brands

- System-wide traffic decline of -1.6%

- Carrabba’s same-store sales decline of -1.8%; cited competitive pressure in the Italian segment

- Carrabba’s new menu (rolled out at the end of Feb.) “hasn’t driven incremental traffic”

- Bonefish same-store sales decline of -1.5%

- Weakness in Korea largely offset strength in Brazil

- U.S. restaurant margins were negatively impacted by a new menu launch and advertising costs

- Operating margins decreased to 8.4% from 8.9%

- Management refuses to halt new unit growth at Carrabbas

Howard Penney

Managing Director

Fred Masotta

Analyst