HEDGEYETV

Controversial best-selling author James Rickards sits down with Hedgeye CEO Keith McCullough to discuss a number of important subjects in this wide ranging interview.

Here's a short excerpt from an institutional conference call that restaurants analyst Howard Penney held with YUM CFO Pat Grismer earlier this week.

Hedgeye CEO Keith McCullough takes a look at key market and economic issues investors should be focusing on right now but aren't.

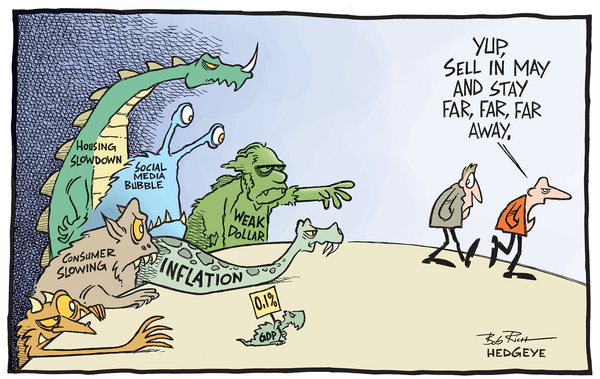

CARTOONs

Buy in May and pray or just go away?

The next crisis will be a crisis of confidence in central planning.

CHART

POLL

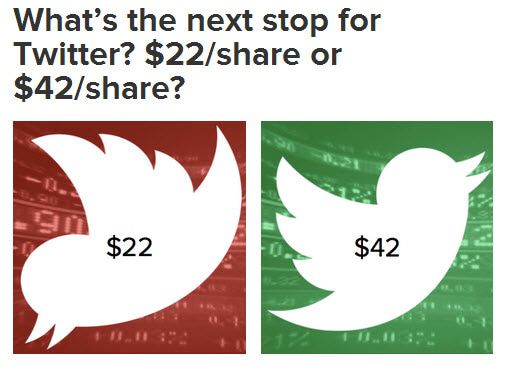

Twitter shares got royally shellacked on Tuesday falling almost 18% after its IPO lock-up period ended. Shares finished trading around $32. Click here to view the poll and results.

HEDGEYE.COM

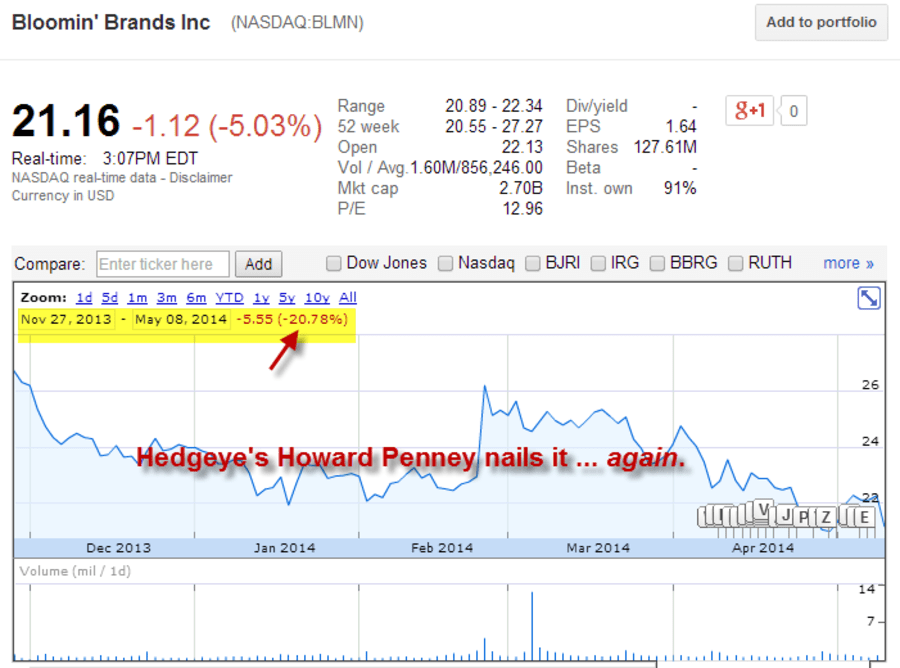

Penney Nails Another 'Best Idea' Short | $BLMN

A couple of weeks ago, we highlighted how Hedgeye restaurants analyst Howard Penney nailed his short call on Panera Bread. He did it again with Bloomin' Brands (BLMN) which he added as a Best Ideas SHORT back on 11/27/13. Click here to continue reading.

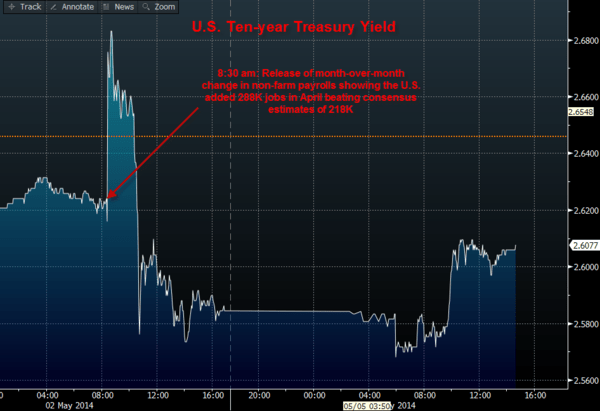

Did the 10-Year U.S. Treasury Go Over The Waterfall?

In a research note CEO Keith McCullough originally wrote before the market opened on Monday, he asked, "So, did the 10-year US Treasury Yield just go over the waterfall of interconnected risk?" Click here to read more.

When It Comes To Twitter, We Tried To Warn You | $TWTR

Twitter stock tumbled over -14% on Tuesday as the lock-up period for early investors has expired, but that doesn’t surprise Hedgeye Internet & Media analyst Hesham Shaaban. He has been the bear on $TWTR. Click here for more.