TODAY’S S&P 500 SET-UP – May 9, 2014

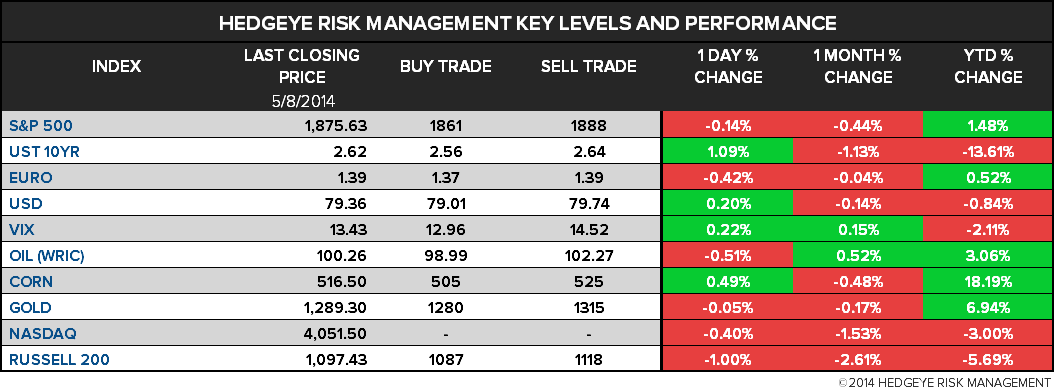

As we look at today's setup for the S&P 500, the range is 27 points or 0.78% downside to 1861 and 0.66% upside to 1888.

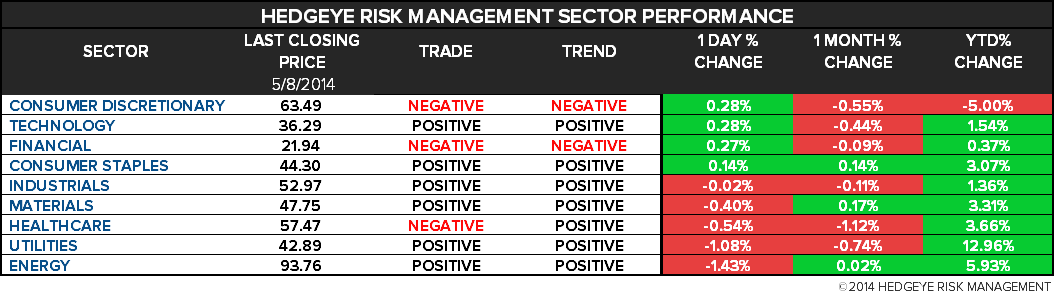

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.22 from 2.23

- VIX closed at 13.43 1 day percent change of 0.22%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: JOLTs Job Openings, March, est. 4.100m (prior 4.173m)

- 10am: Wholesale Inventories m/m, March, est. 0.5% (prior 0.5%)

- 11am: Fed to purchase $1.5b-$2b notes in 2020-2021 sector

- 1pm: Baker Hughes rig count

- 12pm: Fed’s Fisher speaks in New Orleans

- 8:10pm: Fed’s Kocherlakota speaks in St. Paul, Minn.

GOVERNMENT:

- 12:50pm: CFPB Director Richard Cordray speaks at Federal Reserve Bank of Chicago’s conf. on Bank Structure & Competition

- 12:55pm: President Obama speaks on energy efficiency in Calif.

- U.S. ELECTION WRAP: Benghazi Political Risk; Bitcoins for PACs

WHAT TO WATCH:

- Apple said near buying Beats Electronics for $3.2b

- Apple to move up iPhone 6 sales date by a mo.: Eco. Daily News

- Omnicom, Publicis abandon $35b plan for advertising merger

- Mitsubishi UFJ said to weigh offer for BNY corporate trust unit

- Key Senate Democrats said to reject Fannie Mae overhaul measure

- Marchionne to locate Fiat Chrysler headquarters in London

- Winklevoss twins seek Nasdaq listing for Bitcoin exchange fund

- RadioShack will close fewer stores as it contends with lenders

- Twitter COO Rowghani sells part of stake as IPO lockup expires

- U.S. administration reviewing ban on crude oil exports: FT

- Telefonica earnings miss estimates as demand in Spain falls

- Vestas beats ests., posts unexpected 2nd straight qtrly profit

- Man Group assets increase 1.7% to $55b on GLG gain

- China’s inflation decelerates to slowest pace in 18 months

- U.S. Retail Sales, Yellen, BOE, Japan GDP: Wk Ahead May 10-17

EARNINGS:

- Bloomin’ Brands (BLMN) 7am, $0.47

- Broadridge Financial (BR) 7am, $0.25

- Chiquita Brands (CQB) 8:01am, $0.14

- EchoStar (SATS) 8am, $0.03

- Enerplus (ERF CN) 6am, C$0.26

- EW Scripps (SSP) 7:30am, $(0.12)

- Hilton Worldwide (HLT) 6am, $0.09

- HMS (HMSY) 7:30am, $0.16

- Horizon Pharma (HZNP) 6:30am, $(0.02)

- Magnum Hunter Resources (MHR) 7am, $(0.14)

- NorthStar Realty Finance (NRF) 7:30am, $0.23

- Ralph Lauren (RL) 8:01am, $1.63 - Preview

- Sirona Dental Systems (SIRO) 7am, $0.78

- Stratasys (SSYS) 5am, $0.40

- TMX (X CN) 6am, C$1.04

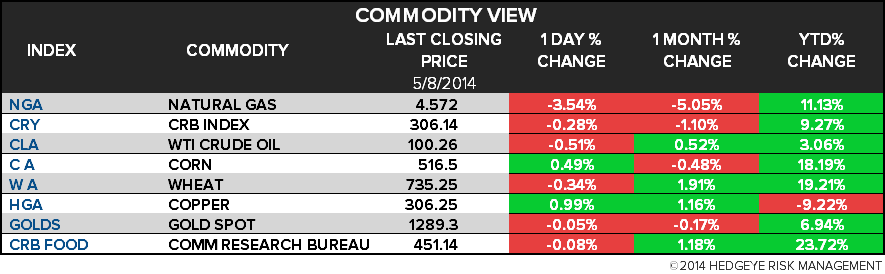

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Nickel Set for Biggest Weekly Gain Since 2010 on Supply Concern

- WTI Heads for Weekly Gain as Crude Stockpiles Drop; Brent Rises

- Biggest Iron Ore Bounty Locked in Spat Eases Glut: Commodities

- Wheat Extends Drop Before USDA Report on Global Supply Outlook

- Gold Heads for Second Weekly Drop on Ukraine to Stimulus Outlook

- Record Beef, Pork Prices Mean Pricey Barbecues: Chart of the Day

- Palm Imports by India Seen Rising First Time in Four Months

- Iron Ore Slumps to Lowest Since 2012 as Global Surplus Deepens

- Russia’s Exports Unhindered by Putin’s Incursion Into Ukraine

- Tumble in Fuel Sales Adds to Evidence of China Slowdown: Energy

- Norway Sees Stable Russia Gas Supply to EU Beyond Ukraine Crisis

- Oil Producer Pleas Snubbed by Norway as Offshore Costs Surge

- Russian Gas Bypass Forces Ukraine to Develop Domestic Resources

- Cocoa Extends Drop in London on West Africa Crops; Sugar Rises

CURRENCIES

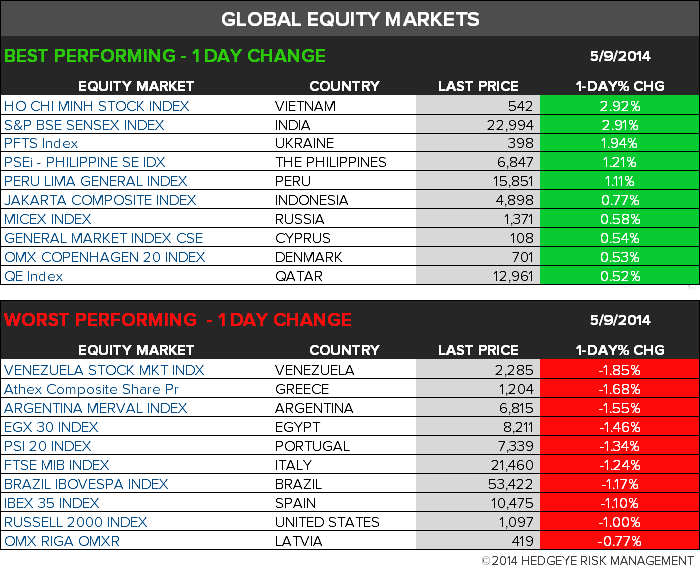

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team