A couple of weeks ago, we highlighted how Hedgeye restaurants analyst Howard Penney nailed his short call on Panera Bread.

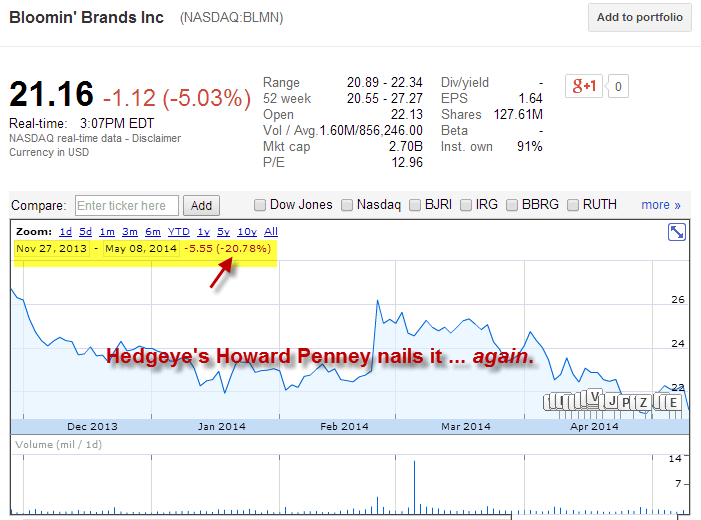

He's doing it again today with Bloomin' Brands (BLMN) which he added as a Best Ideas SHORT back on 11/27/13.

Not bad eh?

During his appearance on HedgeyeTV this past April 7, Penney discussed BLMN as one of his favorite short ideas. Here's the video and performance of the stock since then.

It pays to watch HedgeyeTV.