European Central Bank President Mario Draghi made some noise in this morning’s ECB conference call (and it wasn’t by keeping the main and deposit rates unchanged) – he strongly hinted that the ECB could cut the main rate in its next meeting in June, citing:

- “The strengthening of the exchange rate with low inflation is a serious concern.”

- “ECB is not resigned to have inflation too low for a long amount of time.”

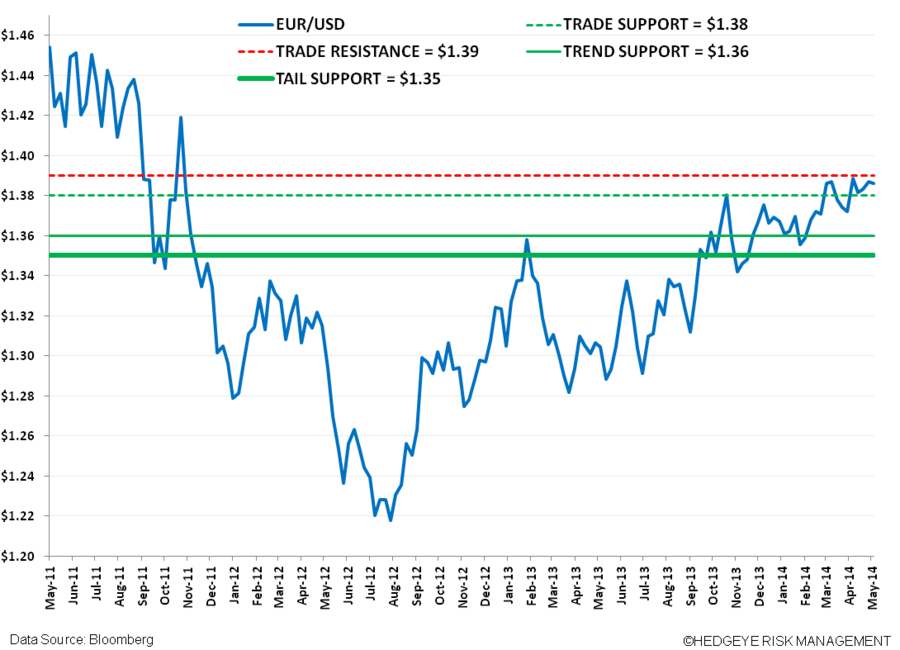

The EUR/USD (up ~ +0.5% heading into the Draghi comments) backed off hard following them.

The cross is now flirting with a breakdown at our immediate term TRADE line of support @ $1.38 – we’d interpret that a breach of TREND support in the Euro and an associated breakout in the dollar would be cause for us to consider shifting our current positioning, but that’s not the case currently. The USD is still broken in our model, so we’ll let the trade breathe for a bit here. The EUR/USD remains above our intermediate term TREND and longer term TAIL lines of support.

Today’s shift in tone demonstrates that Draghi is focused on weakening the Euro and stoking inflation.

This position inflects from more recent meetings that focused on how the Bank was managing a “prolonged period of low inflation” that it believed would grind higher to its 2.0% target rate over the longer term. It also deviates from recent focus on devising lending programs to support the flow of credit to the “real” economy.

The June meeting will also include updated GDP and inflation projection from the ECB’s staff. This data, which will likely lean light on GDP and inflation vs. previous projections in March, could further support a decision to cut the main interest rate.

For reference, here are the March projections:

- GDP Staff Projections: 1.2% in 2014; 1.5% in 2015; 1.8% in 2016

- CPI Staff Projections: 1.0% in 2014; 1.3% in 2015, 1.5% in 2016

Draghi said today that there are downward risks to the region’s growth based on 1) a weakening global demand; 2) geopolitical risks; and 3) the (high) exchange rate.

Nothing like a rate cut to influence what he most directly can: the exchange rate (point #3).

* * * * * *

Editor's Note: This research note was originally provided to subscribers on May 8, 2014 at 10:37 a.m. EST by Hedgeye Macro analyst Matt Hedrick.