“It was fortunate that the Commodore was not educated; for had he been, he would have been a god.”

-New York Sun, April, 1878

You know I love 19th century American Capitalist history. You know I love the epic story of Cornelius Vanderbilt too. The aforementioned quote comes from Part Three of The First Tycoon (pg 333). We should all thank our respective gods that Vanderbilt wasn’t an Ivy League economist.

Counter to popular Marxist beliefs in this country, the capitalists built the steamships and rails. They blew themselves up trying to make money plenty of other ways too – and they liked it. That’s the only way to learn and evolve – having a very real chance that you can fail.

Yesterday, Janet Yellen failed to convince me that she isn’t the ideologue that her partner in pulverizing America’s poor was. I don’t think she’s going to persuade anyone who doesn’t get paid by QE either. That’s at least 80% of the country, fyi.

Back to the Global Macro Grind…

No worries about the long-term in this country. When I am long dead, maybe my son, daughters, or theirs will have an opportunity to live an American life that doesn’t included an un-elected academic droning on like Charlie Brown’s teacher about how the Fed hasn’t perpetuated all-time highs in asset price inflation.

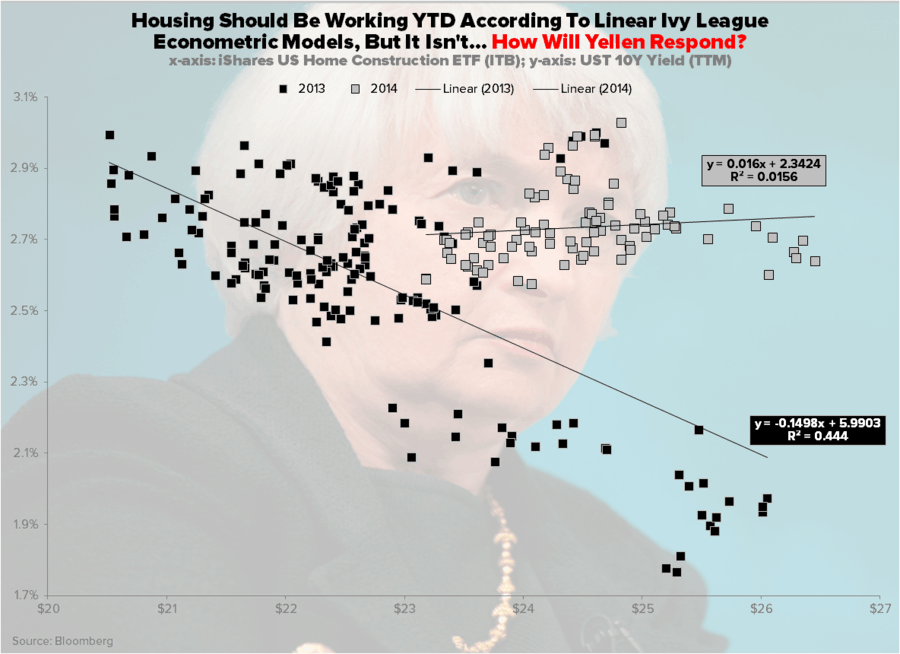

Cost of living in this country is bubbling up to all-time highs. And instead of talking about that yesterday, Yellen was more concerned about what we have been signaling now for months – a redo of a US #HousingSlowdown.

“So” (in classic groupthink lingo, she prefaced every Keynesian comment she made yesterday with that), instead of following the money, follow how her Policy To Inflate Housing Prices plays out from here:

- She starts to talk down Housing’s recovery and, in doing so, rhetorically un-tapers…

- As she un-tapers the hybrid tightening (tapering), the currency and bond markets look more and more right…

- US Dollar Down, Rates Down = Moar Commodity #InflationAcceleraring, and Moar Real #ConsumerSlowing

That’s right. As the cost of living ramps, 80-90% of this country has less dollars to spend. Inflation is real-time, whereas your wages (if you are lucky) adjust on a 1yr lag… and things like rent inflate on a 12-18 month lag to home price appreciation (US Home Prices were +12-13% nationally last year).

“So”, if you are in the 30% (and climbing) of Americans who rent (that’s 1/3 of the cost of living for the median US Consumer – see our Q2 Macro Themes slide deck on the math), Yellen’s narrative on how 0% “is good for housing” is really good for you, right? Yeah, a really good kick in the teeth.

David Einhorn challenged Yellen’s god (Bernanke) on this at a dinner recently (see yesterday’s Bloomberg story: “Einhorn Finds Dinner Chat With Bernanke Frightening”), “so”, take his word for it if you can’t take mine.

Einhorn is obviously a lot smarter than I, but he and the Thunder Bay Bear have a few things in common:

- We were raised in the 1970s (Nixon/Carter bipartisan support to Burn The Buck – i.e. The Policy To Inflate)

- We both learned linear Keynesian economics at Ivy League schools (Cornell and Yale)

- We both learned, as young hedge fund managers in 2000-2001, what Fed bubbles that pop look like when they are popping

“So”, call our paths experience… or something like that. But don’t call us the guys who were buying-the-damn-bubble-stocks on January 1st, 2014. By the way, Twitter (TWTR) is up +3% this morning. “So”, if you bought it JAN 1, you’re down 50%, and only need to be up another +98% from here to breakeven.

In hedgie land (the difference between a hedgie like Einhorn and a Hedgeye is that he runs money and I run my mouth), we call blowing up in names like Zooolilly (ZU) or Fireye (FEYE) or YELP! “drawdown risk.” For the high-multiple momentum bulls, that risk is #on.

“So”, the real reason why Yellen wouldn’t call anything a bubble yesterday – or why Bernanke didn’t call the all-time highs in Housing (2006-2007), Oil (2008), Gold (2011), Food (2012), Bonds (2012), or Junk (2014 – I think Janet called that “high yield”) bubbles, is that they are bubbles.

The only way to prevent a bubble from popping is to: A) not call it one and B) rhetorically signal why you should buy moarrr of it. Or so the Fed thinks. “So”, I think you should take your time observing this gong show and challenge The Fed’s ideological god by shorting the bubbles that start to pop, with impunity.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.56-2.65%

SPX 1

RUT 1101-1121

VIX 12.83-14.52

USD 79.01-79.59

EUR/USD 1.38-1.39

Pound 1.68-1.70

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer