TODAY’S S&P 500 SET-UP – May 6, 2014

As we look at today's setup for the S&P 500, the range is 34 points or 1.52% downside to 1856 and 0.28% upside to 1890.

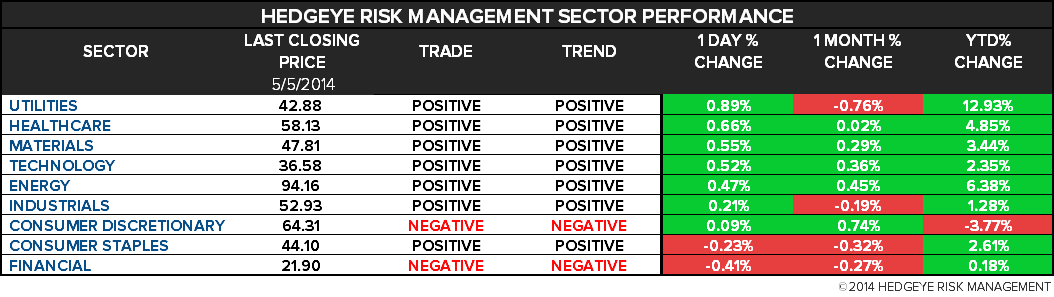

SECTOR PERFORMANCE

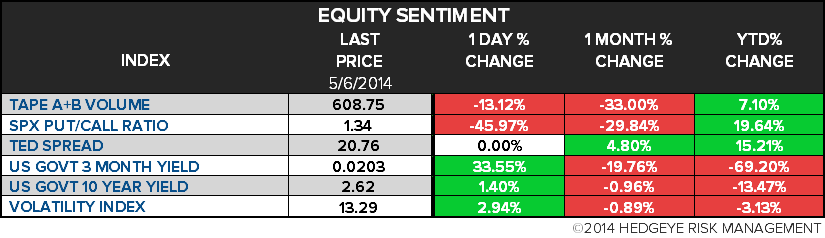

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.20 from 2.19

- VIX closed at 13.29 1 day percent change of 2.94%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:30am: Trade Balance, March, est. -$40b (prior -$42.3b)

- 8:55am: Redbook weekly sales

- 10am: IBD/TIPP Economic Optimism, May, est. 47.9 (prior 48)

- 11:30am: U.S. to sell $35b 4W bills

- Noon: DOE short-term energy outlook

- 1:00pm: U.S. to sell $29b 3Y notes

- 4:30pm: API inventories

- 7pm: Discussion with Fed in St. Louis

GOVERNMENT:

- Primaries today in Indiana, North Carolina, Ohio

- 9:30am: Attorney General Eric Holder delivers remarks at Correctional Workers Week Memorial Service

- 9:30am: Senate Armed Services Cmte hears from Joint Chiefs Chairman Martin Dempsey and services’ chiefs of staff on military pay

- 10am: Senate Finance Cmte holds hearing on highway trust fund

- 10am: Hillary Clinton speaks at Nat’l Council Behavioral Health

- 1pm: Statoil CEO Helge Lund discusses his strategy at CSIS

- 3pm: Senate Foreign Relations Cmte hears from Asst. Sec. of State Victoria Nuland on Russia

- 7pm: Federal Reserve Gov. Jeremy Stein speaks at dinner held by Money Marketeers of New York Univ.

- U.S. ELECTION WRAP: May Primaries; Buffett on Hillary

WHAT TO WATCH:

- French President Hollande says GE bid undervalues Alstom

- Barclays 1Q profit declines more than est. on fixed income

- Ukraine unrest intensifies as toll rises from East offensive

- Google to ask U.S. appeals court to throw out $30m Vringo jury verdict

- Samsung says will challenge Apple patent infringement verdict

- AstraZeneca chairman asks Cameron to stay bid-neutral: FT

- Pfizer CEO willing to walk away from AstraZeneca bid: WSJ

- Investors pushing U.S. banks for cash returns, special divs.

- Credit Suisse put business probed by U.S. into separate unit

- Fiat said to start Alfa Romeo model expansion with own funds

- Sprint matches T-Mobile’s prepaid plan in Son’s price war

- Coke, Pepsi to remove vegetable oil derivative from drinks

- N.D. Sen. Hoeven says 3 votes short of Keystone cloture

- Senate Foreign Relations Cmte meets on Russia, Ukraine

- Fed Gov. Jeremy Stein speaks at 7pm NYU dinner

AM EARNS:

- Akorn (AKRX) 6:00am, $0.15

- AMETEK (AME) 7am, $0.56 - Preview

- Arcos Dorados Holdings (ARCO) 8am, $0.02

- Ares Capital (ARCC) 8am, $0.39

- Arrow Electronics (ARW) 8am, $1.21

- BCE (BCE CN) 7am, C$0.76 - Preview

- Carrizo Oil & Gas (CRZO) 6:30am, $0.40

- CBOE Holdings (CBOE) 7:30am, $0.56

- Denbury Resources (DNR) 7:30am, $0.25

- Dentsply International (XRAY) 7am, $0.56

- Discovery Communications (DISCA) 7am, $0.71

- Emerson Electric Co (EMR) 6:30am, $0.81 -Preview

- FirstEnergy (FE) 8:30am, $0.42

- George Weston (WN CN) 8am, $0.76

- GNC Holdings (GNC) 8am, $0.76

- Henry Schein (HSIC) 7am, $1.13

- Hillshire Brands (HSH) 7:30am, $0.36

- HollyFrontier (HFC) 7am, $0.77

- Intl. Flavors & Fragrances (IFF) 7am, $1.25

- Isis Pharmaceuticals (ISIS) 8:30am, ($0.24)

- Magellan Midstream Partners LP (MMP) 8:30am, $0.68

- Mosaic (MOS) 7am, $0.59 - Preview

- NRG Energy (NRG) 6:49am, ($0.13)

- Nu Skin Enterprises (NUS) 7:30am, $0.94

- Office Depot (ODP) 7am, $0.03

- Quicksilver Resources (KWK) 7:30am, ($0.07)

- Radian Group (RDN) 7am, $0.22

- Rowan Cos Plc (RDC) 8:00am, $0.20

- Semafo (SMF CN) 8:23am, ($0.02)

- Towers Watson & Co (TW) 6:00am, $1.48

- Vantage Drilling Co (VTG) 7am, $0.08

- Vishay Intertechnology (VSH) 7:30am, $0.18

- Vulcan Materials (VMC) 8am, ($0.33)

- Western Refining (WNR) 6:00am, $0.40

- WestJet Airlines (WJA CN) 6:30am, C$0.63 -Preview

- Zoetis (ZTS) 7am, $0.37 - Preview

PM EARNS:

- Acadia Pharmaceuticals (ACAD) 4:01pm, ($0.13)

- Activision Blizzard (ATVI) 4:05pm, $0.10

- Agrium (AGU CN) 6:45pm, C$0.04 - Preview

- Allstate (ALL) 4:05pm, $1.20

- Electronic Arts (EA) 4:03pm, $0.11 - Preview

- FireEye (FEYE) 4:05pm, ($0.53)

- First Solar (FSLR) 4:05pm, $0.52

- FMC (FMC) 4:15pm, $0.95

- Forest Oil (FST) 4:22pm, ($0.02)

- Frontier Communications (FTR) 4:01pm, $0.06

- Groupon (GRPN) 4pm, ($0.03) - Preview

- Iamgold (IMG CN) 5:04pm, $0.02

- Liberty Global PLC (LBTYA) 5:40pm, ($0.08)

- Marathon Oil (MRO) 4:03pm, $0.72

- Matador Resources Co (MTDR) 4:05pm, $0.28

- Microchip Technology (MCHP) 4:15pm, $0.62

- Myriad Genetics (MYGN) 4:05pm, $0.45 - Preview

- Oneok (OKE) 4:05pm, $0.37

- Pioneer Natural Resources Co (PXD) 4:05pm, $1.06

- Prospect Capital (PSEC) 4pm, $0.32

- Qiagen NV (QGEN) 4pm, $0.22

- Sun Life Financial (SLF CN) 5:10pm, C$0.66 - Preview

- Trimble Navigation (TRMB) 4:02pm, $0.42

- TripAdvisor (TRIP) 4:02pm, $0.54

- Veresen (VSN CN) 4:22pm, C$0.05

- W&T Offshore (WTI) 5:20pm, $0.21

- Walt Disney (DIS) 4:15pm, $0.95 - Preview

- Whole Foods Market (WFM) 4:03pm, $0.41

- Zulily (ZU) 4:05pm, $0.00

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Rises as Russia and Europe Discuss Ukraine; WTI Advances

- El Nino Alert Signals Drought, Flood Risks for World’s Farmers

- Crop ETFs See 27% Surge in Assets on Weather Risks: Commodities

- Nickel Advances as Ukraine Fuels Concern Supply Might Run Short

- Corn to Soybeans Slip as U.S. Weather Outlook Favors Planting

- Gold Near Three-Week High as Ukraine Weighed With U.S. Economy

- Sugar Rises Amid El Nino Alert Update; Arabica Coffee Also Gains

- Nickel to Rally 20% Further Amid Indonesia Ban, Survey Shows

- G-7 ‘Determined’ to Cut Russian Energy Dependence, U.K. Says

- British Coins Pass Test in 800-Year-Old Rite as Osborne Watches

- Cushing Oil Storage Area May Empty in Weeks: Morgan Stanley

- Oseberg Crude Exports Said to Jump to Seven Cargoes in June

- Copper Supply Additions May Peak in 2014, Plunge 79% by 2020

- No Petroleum No Problem for Pipelines Backed by Private Equity

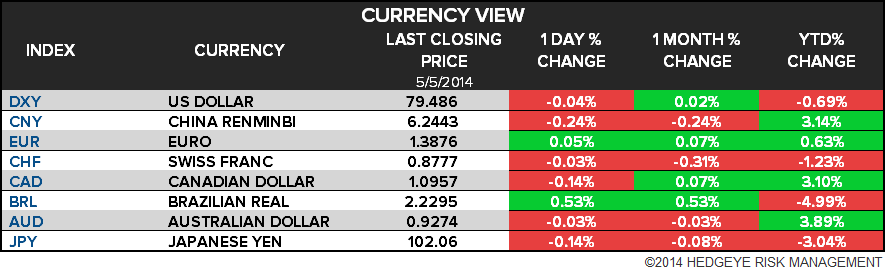

CURRENCIES

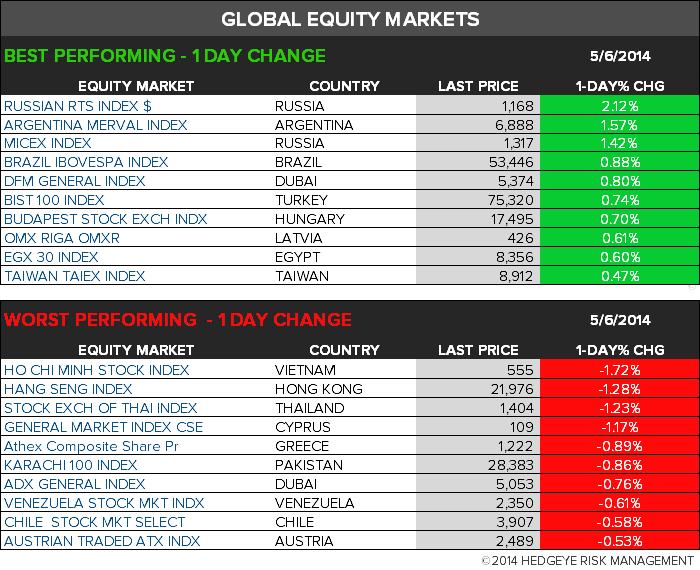

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team