Let’s be clear about what happened…Sheinhafel was fired. Too many people are saying that he ‘stepped down’. Not to rub this in his face, as we respect anyone that stays with one employer for 35 years. But the reality is that Target is in a world of hurt right now. Ultimately, this mess is his fault, and a regime change is appropriate. Importantly, anyone looking at this solely as a state of near-term affairs at TGT is missing the bigger picture. This emphasizes to us how critical it will be for a new CEO to right-size (take down) the earnings structure before it can build a company with respectable margins and return profile that is consistent with its Target banner.

Here are some of our thoughts.

- The company reports earnings in two weeks. This is about the time that the Board gets its preliminary Flash report on the state of financial affairs. No CEO was ever fired because ‘business is just too darn good’.

- Contrary to what the press is touting today, we don’t think he was fired because of the data breach – or even the ensuing weak store traffic. If anything short-term related, it’s probably because he set such egregious expectations with both the Board and the investment community for positive comp AND improving gross margin.

- But our rather strong view is that these are short-term events that most quality organizations could otherwise overcome. In this case, they exposed Target’s vast deficiencies throughout its business – arguably the worst e-commerce business in retail, it’s flawed p-fresh and Red Card initiatives, the lack of growth in its core US market, and the highly questionable strategy to look towards the Great White North as a means to find square footage growth.

- Some people might argue that a new ‘rock star’ CEO will come in, cut costs and take up margins. We mostly disagree. Yes, Target can afford the best of the best. But any great CEO worth their salt will come in, assess the challenges, and invest in the business such that it has the foundation to take the stock meaningfully higher over the period their options or RSUs vest. That means taking margins and earnings down before they can (hopefully) ultimately climb back up again.

- We’re not making any changes to our financial model today, but our strong inclination is to take down our EPS estimates – which are already 27% below consensus in the out-years of our model – a huge delta for a sleepy company like Target. We wouldn’t be surprised to see earnings fall below $3.00 while new management gets Target’s act in gear. This makes today’s 3% selloff all the more immaterial in the grand scheme of how much lower this stock can go.

HERE’S OUR NOTE FROM WHEN WE ADDED TGT TO OUR BEST IDEAS LIST AS A SHORT LAST WEEK

TGT – WHY WE THINK TARGET IS A SHORT

Conclusion: We’re short Target. We think that the model that management is selling to the Street leaves no room for error. Everything has to go right, and nothing can go wrong. We’re in the twilight of a department store margin cycle, margins are at peak, our proprietary survey shows that visitation at Target stores is down materially, and worse yet, the share appears to be going to Wal-Mart. We could make a case that target.com is one of the worst e-commerce businesses in retail, and it is certainly not making up for the shortfall in stores. Lastly, Canada expectations are extremely high, and our analysis of demographics around new Canadian stores leaves us with the view that management growth and profitability expectations are a pipe dream. In the end, we’re 27% below the consensus in year 3 of our model – which is a huge delta for this company. We get to downside to the high $40s ($13/14) if we’re right, but about $5/$6 upside if we’re wrong – that’s nearly 2.5 to 1. We’ll take that anyday on a sleepy mega cap retailer like Target.

Earlier this week, we published our 47-page deck on why we think Target is a short. We can’t print all the slides here, but here are five that we think are among the most notable.

1. The Macro Setup is not pretty. We just finished the fifth year of a margin expansion cycle for department stores. When we look back historically, we don’t think that there’s ever been a ‘year 6’. And by a country mile, we’re trading at peak valuations on these margins. The core of the TGT call goes far beyond this, but this is an extremely uninspiring backdrop.

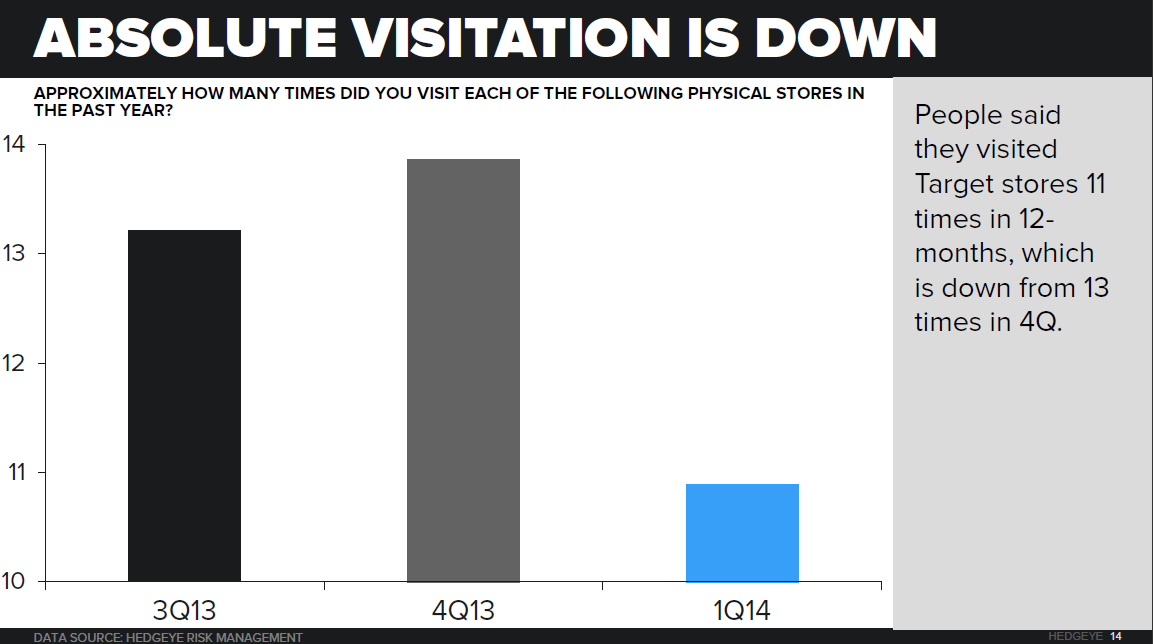

2. Visitation is down. We’re all tired of hearing about the Data Breach. But the reality is that the fallout is extremely notable. We just conducted our third Department Store consumer survey and we can gauge sequential changes in visitation intent on an absolute basis, and relative to other retailers. This shows how TGT went from 13 visits (TTM) in 3Q, to near 14 in 4Q (pre-Breach), to 11 today. That might not seem severe, but that’s 20% by our math.

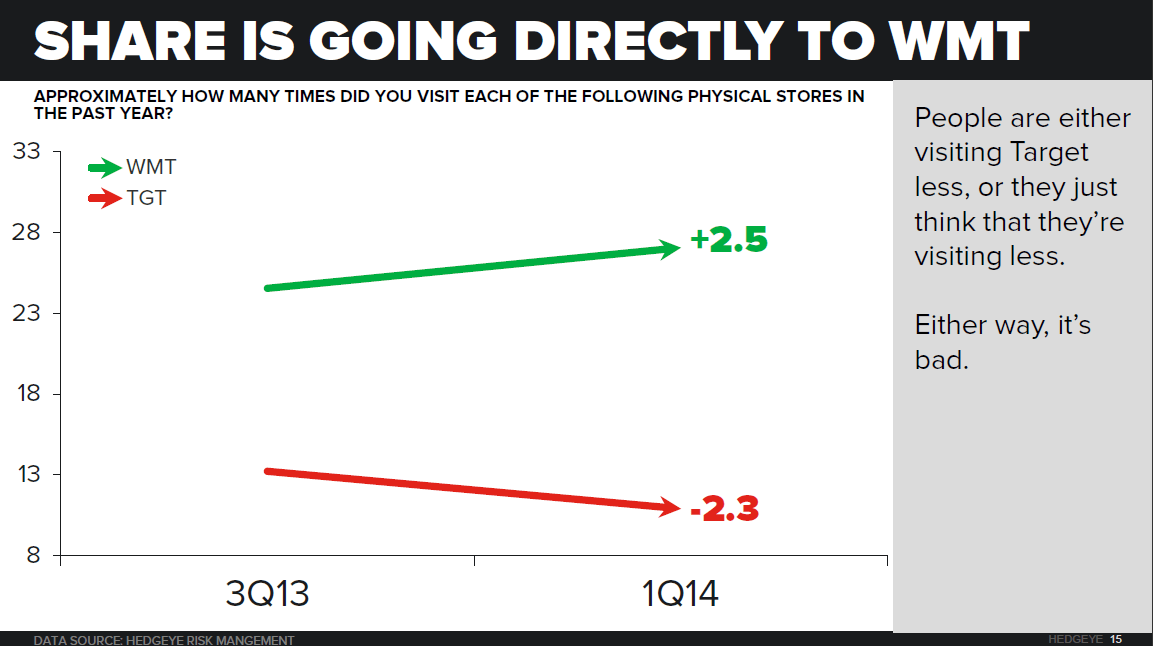

3. Share is going to Wal-Mart. Not exactly the retailer we’d want to lose share to if we were Target. When WMT takes share, it has a tendency to not give it back. We have a lot of research in our deck that shows how consumers rank them on price, discounts, and product quality. The trends are compelling.

4. Dot.Com can’t save TGT. When other retailers get into trouble with their stores, often e-commerce makes up the difference. Our analysis of target.com’s traffic trends suggest that dot.com is performing just as poorly as the stores – if not worse. Based on our research, we can make a case that Target has one of the worst e-commerce businesses in all of retail.

5. Canada can’t save Target, either. We pulled up the lats and longs for both Canada and US stores, and then analyzed demographics in a 20-minute driving radius. Canada lacks the density and income characteristics around its stores that Target enjoys in the US. That’s not to mention that there is a cannibalization issue given that 11% of target customers already shop in Target US stores. Consensus revenue estimates assume that Target Canada outstrips share of wallet levels Target has in the US. The company’s guidance assumes productivity levels above US levels. We think both are extremely unrealistic.

HERE’S OUR ‘3 KEY QUESTIONS’ NOTE FROM LAST MONTH FOR STEINHAFEL

APRIL 7

TGT: 3 KEY QUESTIONS

If we had five minutes or less with TGT’s CEO, here’s what we’d ask.

Here’s the deal…you have five minutes alone with the CEO of a company, leaving time for maybe three questions. If you value your time you’re likely to focus on the key critical uncertainties that exist in the market. And make no mistake, they exist for every company out there.

We’re going to explore these key questions one company at a time, and we’re going to start with Target – which we think is one of the better shorts in retail.

Here’s what we’d ask CEO Gregg Steinhafel if we had five minutes or less.

1. Who Are You Guiding? Who are you talking to with your guidance, Wall Street or Main Street? We’ve never had to ask this question before to a CEO. But the reality is that you’re saying that you are going to comp positive this year, AND Gross Margins will be up (in the US and in Canada). And all of this will happen while you are lowering prices to win back customers who left after the data breach. It seems like an impossible combination. That leads us back to the question – are you giving that guidance to Wall Street or Consumers? This is kind of like what Cruise Companies do during their peak booking season – they generally have positive comments because they’re talking to travel agents, not to Wall Street. If they say that bookings are weak, then agents will discount price more heavily. Similarly, is Target sending out this perplexing message to keep consumer opinion high, even if it means the potential to lower expectations with Wall Street later in the year.

2. Share Loss. Who do you think is gaining the most business from the customers who left? For argument’s sake, let’s assume that it’s Wal-Mart. Do you think that WMT is prepared to let that business go so easily? Will you match Wal-Mart if it comes down to price? In reality, the people that left did not leave because of price. They left because of trust. You might be able to buy back trust, but you’ll have to undercut Wal-Mart on price rather significantly. If that’s true, refer to question #1.

3. What does Target want to be? That sounds like a ridiculous question at face value. But the reality is that it used to be Wal-Mart vs Target – in share of market, share of mind and share of investment dollars. But as bad as Wal-Mart’s rap sometimes can be, it has over 10,000 stores under 71 banners in 27 countries. It has several formats – from Supercenters, to warehouse clubs, to neighborhood markets, and it is even beta-testing C-stores/gas stations. At least it’s trying to evolve. Target has just has one primary format in North America, with a token operation in India. The point is that Target used to be right there with WMT – but now it seems to be somewhere between WMT and Kohl’s. When you look out five to 10 years, what will Target look like?

Bonus Question (if he hung around an extra 2 minutes).

Do you think you fired your customer? JC Penney fired its customer. Ron Johnson said at the time that he did not. Lululemon fired its customer. Chip Wilson said at the time that he did not. Both of those retailers will likely take 2-3 years to get an acceptable portion of customers back. Do you think that you have fired your customer? Your guidance suggests that the answer is No. (Note: we’d give him all the credit in the world if he said Yes – because it would suggest he’s doing something about it).