Last night’s 5% pullback in the Shanghai Composite was a jolt to the system of bubble watchers like myself who have been following the trajectory of a market that appears to have come too far too fast in recent weeks -driven by a cocktail of optimistic first-time investors, easy credit and raw momentum. 5% does not a correction make however, so the price action in the next two sessions will provide us with a critical signal.

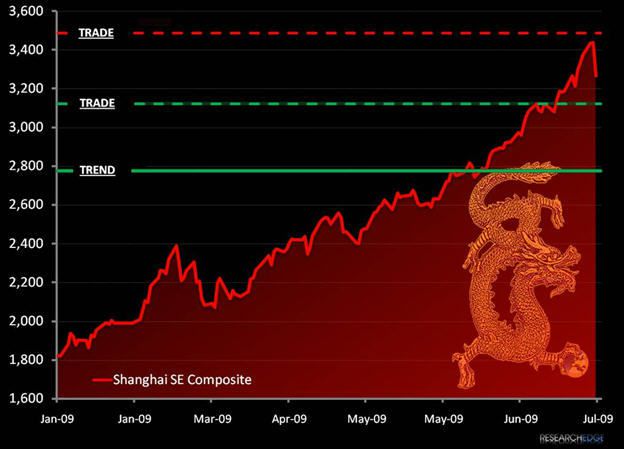

Currently, the quantitative model that Keith uses as part of our portfolio process has identified a SSEC index TRADE resistance level at 3,488 and a TRADE support level at 3,123. On a longer duration, 2776 is setting up as a TREND support line.

In the here and now, Chinese equities are not being driven by fundamentals and only two forces are poised to force a reckoning:

- The IPO Calendar: In the wake of the 12 billion share State Construction initial offering there are a slew of additional companies lined up to begin trading now that the 9 month new issue moratorium has ended. Presumably, even with the billions of dollars that Chinese households have in savings accounts, the impact of increased supply will be felt eventually.

- Credit: Last night saw a 57 basis point spike in 1 month repo rates to 2.23% on speculation of tightening by the central bank. The trend in short term rates in recent weeks has been pronounced as more stock and commodity speculators enter the short term money markets (see chart below).

On this second point, Ken Fisher was quoted today saying that Chinese regulators have “zero incentive” to curb lending since the nation’s economy is “going gangbusters compared to the rest of the world, so why would they try to kick that”. Now I know that Ken has been doing this for longer than I have, but to my mind the decision by the central bank to keep the loosening policy in play doesn’t necessarily mean that they won’t try to curb speculative excess. Beijing doesn’t want to have volatile stock market fluctuations create discord among the new retail investors flocking to the markets so, I think that it is entirely possible that they could take steps to reign in margin lending and proprietary speculation by banks ( a growing factor in the equity markets there –see chart below) without impacting the access to credit for consumer spending on durable goods and industrial expansion.

Andrew Barber

Director