TODAY’S S&P 500 SET-UP – May 5, 2014

As we look at today's setup for the S&P 500, the range is 28 points or 1.12% downside to 1860 and 0.36% upside to 1888.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.16 from 2.16

- VIX closed at 12.91 1 day percent change of -2.57%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:45am: Markit US Svcs PMI, April final, est. 54.5 (pr 54.2)

- 10am: ISM Non-Manufacturing, April., est. 54.0 (prior 53.1)

- 11am: U.S. announces plans for 4W bill auction

GOVERNMENT:

- Democrats should boycott Benghazi select panel, Schiff says

- Clinton sidesteps 2016 plans in accepting Illinois Lincoln award

- House, Senate in session

- Obama will host Djibouti President Ismail Omar Guelleh

- 9:30am: Supreme Court releases list of cases it plans to consider; may issue opinions at 10am

WHAT TO WATCH:

- China manufacturing gauge signals deeper slowdown risk

- Buffett says likely to join with Lemann’s 3G on another deal

- AstraZeneca rejects Pfizer, which may eye sweetened offer

- Fed’s Fisher: Economy strengthening as private payrolls rise

- EU reduces euro-area growth forecast as inflation seen slower

- Ukraine unrest flares across country as Kiev’s control slips

- Citigroup wins custody deal from world’s biggest sovereign fund

- ‘Spider-Man’ leads N.A. box office, tho sales miss some est.

- U.S. pump price hits 14-mo. high of $3.72: Lundberg survey

- LightSquared makes closing arguments in bankruptcy exit hearing

- Siemens said near deal to sell airport unit to Wilbur Ross

- Twitter lock-up expires as shrs drop 47% from high

- Swatch objects to authorities over Apple’s use of iWatch label

- Nokia joins Musk to Google in investing in intelligent cars

- Alibaba founders seek control with partnership alternative

- B/E Aerospace puts itself up for sale, cancels investor mtg

- Ackman, Einhorn speak at Sohn Investment Conference

- Yellen Testimony, ECB, Bank of England: Wk Ahead May 5-10

AM EARNS:

- Auxilium Pharmaceuticals (AUXL) 7am, $(0.22)

- BroadSoft (BSFT) 7am, $0.11

- Brookfield Infrastructure (BIP) 7:30am, $0.38

- Hecla Mining (HL) 8am, $0.00

- Occidental Petroleum (OXY) 7am, $1.70 - Preview

- Orbitz Worldwide (OWW) 8:08am, ($0.03)

- Pfizer (PFE) 7am, $0.55 - Preview

- Realogy (RLGY) 6:35am, $(0.19)

- Sysco (SYY) 8am, $0.40

- Tyson Foods (TSN) 7:30am, $0.63

- Westlake Chemical (WLK) 6am, $1.13

PM EARNS:

- Alleghany (Y) 4:07pm, $8.16

- American Intl Group (AIG) 4pm, $1.07

- Anadarko Petroleum (APC) 4pm, $1.15

- CareFusion (CFN) 4:02pm, $0.62

- EOG Resources (EOG) 5:11pm, $1.19

- Genpact (G) 4pm, $0.23

- Integrated Device Technology (IDTI) 4:01pm, $0.13

- Mindray Medical Intl (MR) 5pm, $0.38

- Oasis Petroleum (OAS) 4:15pm, $0.63

- Tenet Healthcare (THC) 4:30pm, $(0.15)

- Vivus (VVUS) 4pm, $(0.34) - Preview

- Vornado Realty Trust (VNO) 4:52pm, $0.53

- YY (YY) 4:01pm, $0.49

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Wheat Rises to Highest in Year as Ukraine Boosts Supply Concern

- Iron Ore Seen Slumping Below $100 as Surge in Supply Widens Glut

- Hedge Funds Reduce Gold Bets to Lowest in 11 Weeks: Commodities

- Gold Extends Climb to Three-Week High as Ukraine Spurs Demand

- Brent Rises to Near 6-Day High as Ukraine Offsets China Slowing

- Copper Declines as China Manufacturing Gauge Misses Estimates

- Platinum Mines’ Union Bypass May Disrupt Industry, AMCU Says

- Speculators Cut Bullish Oil Wagers on Record U.S. Supply: Energy

- ARA Gasoil Supplies Rose 4.5% in Week to April 25, Genscape Says

- Palm Oil Output in Indonesia Seen Hurt by Golden Agri on El Nino

- U.S. Gasoline Rises to 14-Month High, Lundberg Survey Shows

- Palm Oil Drops to Three-Week Low as Malaysian Output Seen Rising

- Competition Means New GrainCorp Bid May Win Approval, UBS Says

- Libya Crude Exports Dropped 36% in March, National Oil Says

CURRENCIES

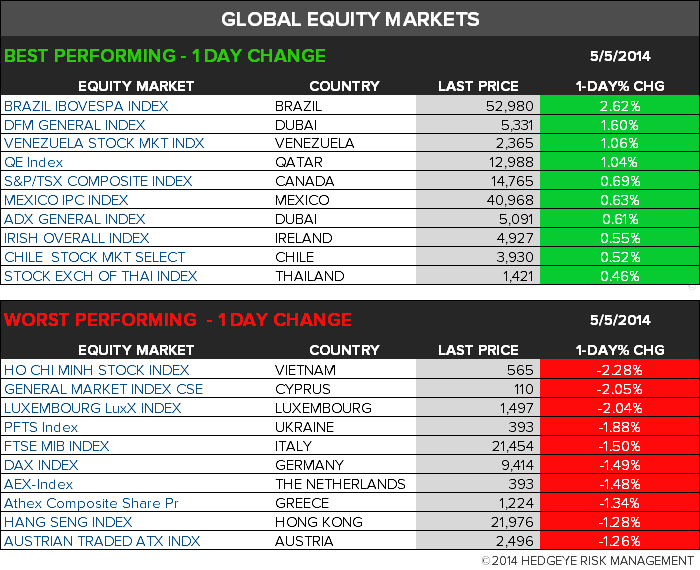

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team