Going into Q2, I was having difficulty seeing how PNRA would achieve the high end of its $0.62-$0.64 EPS guidance range. Well today, PNRA reported $0.69 per share excluding $0.04 of one-time charges. On the high quality side, PNRA’s company same-store sales came in at -0.7%, which was better than my expectations, particularly considering the 6.5% comparison from 2Q08. PNRA’s same-store sales improved rather significantly throughout the quarter, posting -1.9% in April, -1.6% in May and +1.6% in June. The favorable June sales trends continued into July and even improved, running up 2.8% for the first 27 days of Q3.

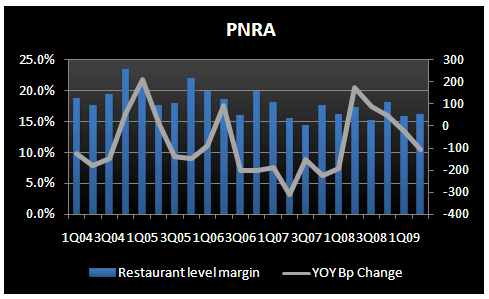

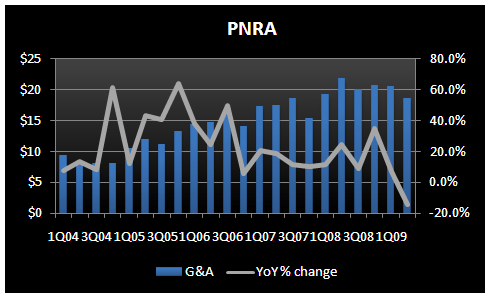

On the low quality side, however, G&A expenses declined nearly 15% YOY, marking the first time this expense has decreased on a YOY basis in at least 5 years, never mind the magnitude of the decline! This significant cut to G&A costs accounted for $0.04 per share relative to what I was modeling. Management stated that it is not cutting G&A, but rather the quarterly decline can be attributed to the general lumpiness of projecting G&A costs as a result of timing differences for overhead expenses. Specifically, management said that bonus accruals were lower in 2Q because relative to certain performance metrics, the company had underperformed relative to Q1. Given that restaurant margins declined 110 bps YOY in the quarter (before the one-time charge related to the roll out of new china), the timing of such a significant reduction to G&A expense does not seem coincidental. Instead, it seems that management needed to cut G&A to save operating margins.

Even with PNRA maintaining such impressive top-line numbers, it is going to become increasingly more difficult for the company to maintain margins. Unlike most restaurant companies, PNRA is still growing. I am forecasting 4% company unit growth in 2009, which means that PNRA is still incurring growth related costs. And, these costs are only heading higher next year because management stated today that it expects to increase its company-owned unit growth by 50% in 2010. PNRA is only expecting modest cost inflation in 2010 as higher labor and occupancy costs are expected to be largely offset by lower food costs, but increased development costs will creep into the P&L as the company aggressively ratchets up its unit growth targets.