SUMMARY: The establishment report was strong, the household report was weak and earnings growth was middling as the collective two-day takeaway is that growth probably isn’t as bad as yesterday’s GDP report or as strong as today’s headline NFP or Unemployment rate would suggest. The muddle continues.

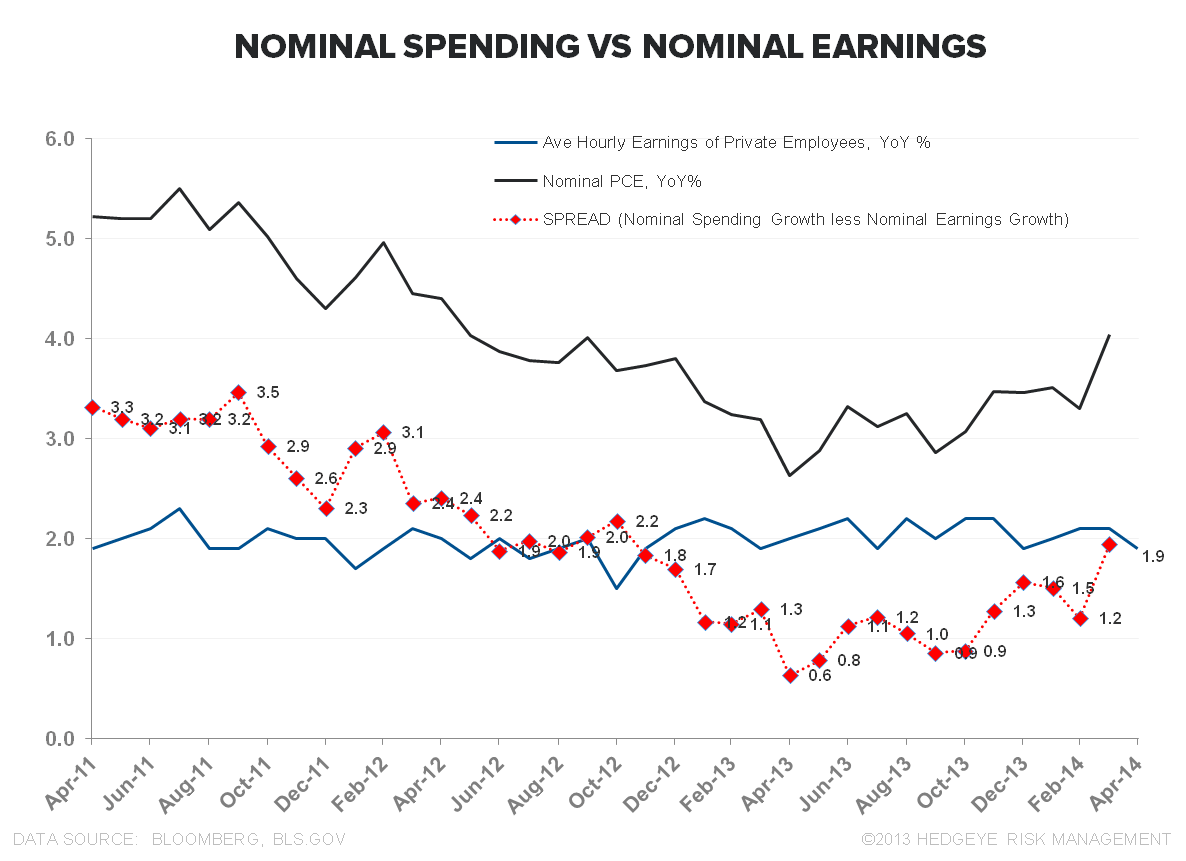

Neither the dollar nor rates are buying into the headline strength and with inflation accelerating (real-time billion prices project says 2.5% inflation, 1950's style survey Core PCE says <1%), housing decelerating, the wealth effect ebbing, income growth not enough to sustainably support the current level of household spending, and consensus growth estimates still too high, we think the call is to stick with the YTD playbook.

See this morning’s EARLY LOOK for the strategy breakdown.

SINCE THE TROUGH: Here’s the current tally across the various payroll/labor measures since the February 2010 NFP employment trough. We eclipsed the January 2008 peak in Private employment last month and, at present, are 113K below the prior peak in total NFP employment.

- NFP: +8.6MM

- Private: +9.2MM

- Household Survey: +7.1MM

- Labor Usage/Job equivalents (Total employed * Hours/wk): +11MM

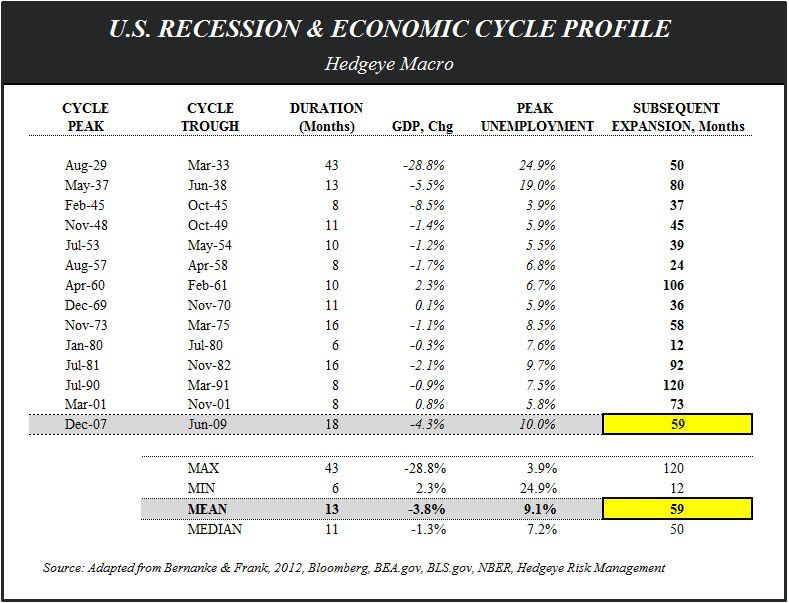

THE TELL-TALE HEART: Duration of Current Expansion: At 59 months as of April, the current expansion sits exactly at the mean duration of expansions over the last century.

As we highlighted previously (GREEN SCREEN MACRO) balance sheets recessions are defined by slower recoveries with lower amplitude (& likely longer periods), but the fed, in weighing their policy course, has to be considering the ticking clock (or beating heart to maintain the analogy) and their capacity for dealing with another cyclical downturn.

HOURLY EARNINGS: Average private hourly earnings growth decelerated -20bps sequentially to +1.9%. Sub-2% wage growth belies the optical strength in the NFP figure and is not enough to support the current level of household spending.

The upside for consumption will remain constrained as share of wallet for other discretionary purchasing remains pressured by rising food and energy inflation and soft real wage growth.

WHAT IF? The below don’t provide much in the way of practical application, but they do provide some context along with the entertainment value.

- What if the Labor Force Participation Rate (LFPR) had remained the same MoM – what would the April Unemployment rate have been?

If population growth is taken as given and YoY growth in total employed as measured by the household survey (where YoY growth has been rather consistent despite the volatility in the absolute MoM figures) grew at the 3M average of 1.39%, a static participation rate would equate to a 6.85% Unemployment rate for April

- What if the post-recession employment distribution = pre-recession employment distribution?

The idea that the employment recovery has been largely illusory because we’ve only added low wage and part-time jobs has garnered continued attention.

Yes, the distribution of employment by industry has shifted, but not tremendously, and while structural unemployment will remain a Trend issue (for a host of reasons), such a shift is a necessary disruption for an economy in selective, secular transition (more energy, more medical, more tech, etc).

In the scenario analysis below we show actual aggregate earnings (indexed) since the February 2010 employment trough vs. implied aggregate earnings had payroll gains since the trough occurred at the pre-recession employment distribution. As can be seen, at a cumulative delta of ~25bps, the difference isn’t particularly stark. It's a good narrative though.

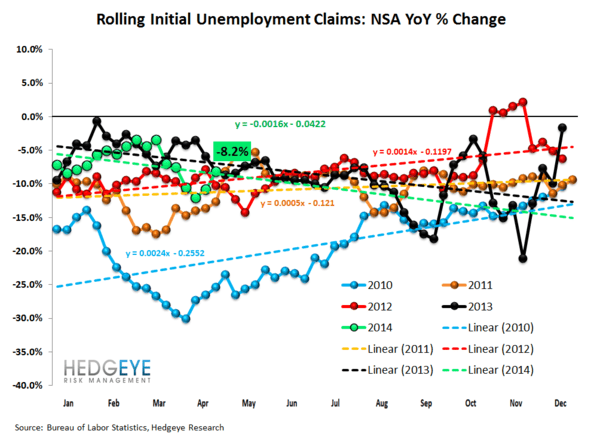

INITIAL JOBLESS CLAIMS: The accelerating improvement in initial jobless claims over the last six weeks was supportive of NFP strength in April as seasonally-adjusted claims were ~15K lower in April (during the employment survey period) and ~40K lower than April of last year.

Notably, after 5 weeks of accelerating improvement, non-seasonally adjusted jobless claims, which we consider a more accurate representation of the underlying labor market trend, were up 5.1% in the latest week - compared with down 8.3% in the prior week.

The 4-week rolling average, the better measure, showed a decelerating rate of improvement, moving to -8.2% from -10.9% on a y/y basis.

Source: Hedgeye Financials

State & Local Government Employment: State & local government employment growth accelerated for a fourth straight month in April. At ~17% of both NFP employment and aggregate wage/salary income, the ongoing improvement in state fiscal positions should continue to support both job and government expenditure growth.

Household Survey: The Unemployment rate posted its largest sequential decline (-0.4%) since December 2010 as the labor force declined by -806K (-733K Unemployed + -73K Employed) and the LFPR returned to recent trough (down 37bps to 62.81%) trough levels.

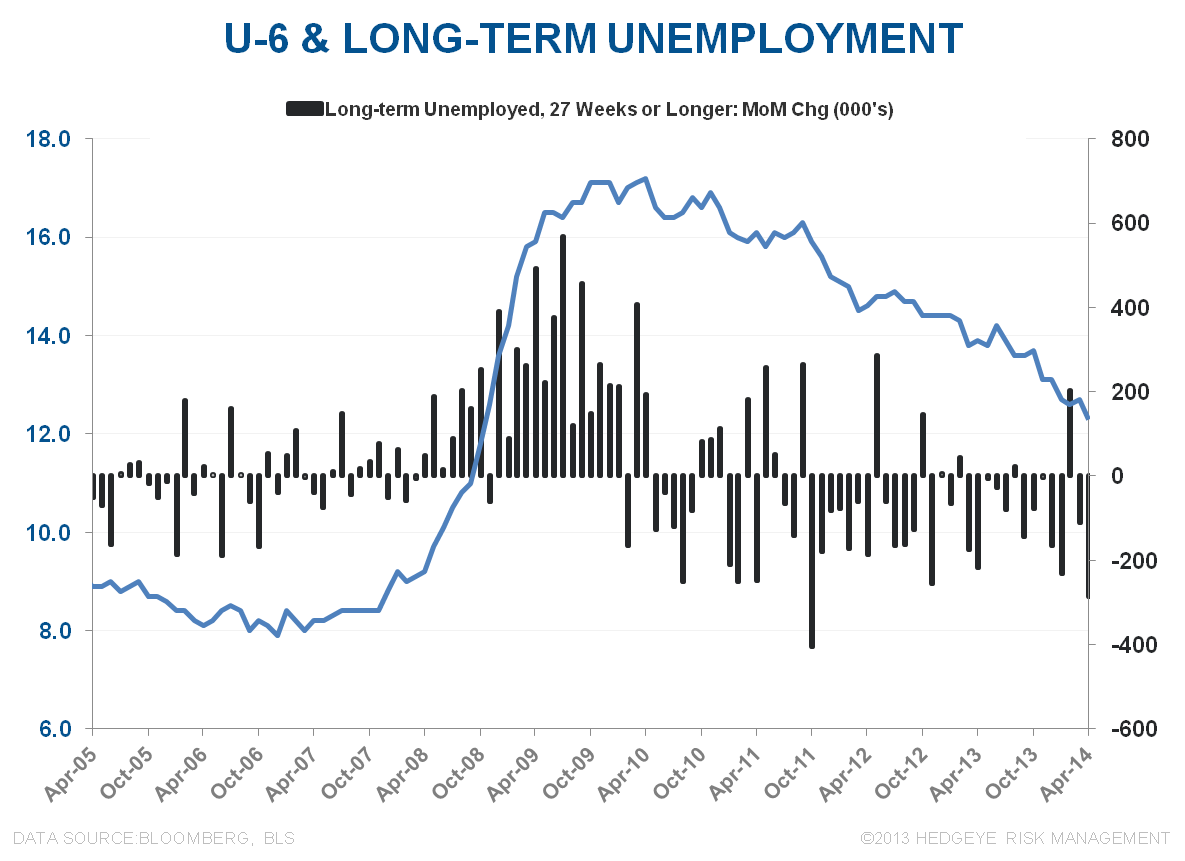

The U-6 rate (12.3%) followed the U-3 rate lower (positive, on balance), declining -40bps sequentially while employment growth decelerated across all age cohorts except 55-64 year olds to start 2Q14

Enjoy the Weekend,

Christian B. Drake

@HedgeyeUSA