Below are Hedgeye analysts' latest updates on our EIGHT current high-conviction investing ideas and CEO Keith McCullough's updated levels for each.

We also feature three research notes from earlier this week which offer valuable insight into the market and economy.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

DRI – On April 30, Darden announced that Chief Restaurant Operations Officer, Dave Pickens, will retire effective May 23. DRI will not replace Pickens and plans to eliminate the position altogether. Pickens, a career DRI employee, got a one sentence send off from the company and not even a “thank you” from CEO Clarence Otis in the SEC Filing.

This move is, in our opinion, very telling as it suggests a very tense environment down at the company’s lavish corporate headquarters in Orlando. We continue to believe the activists will get their way and, for that reason, favor DRI as a strong long-term investment.

HCA – HCA Holdings put up a good number for 1Q14 even without the benefit of the ACA. The best part of the quarter in our view was the comment that births had increased 2% overall and commercially insured deliveries had increased 4%. We think we have a really good model to forecast birth trends and a decent one for surgical trends. If we get those two things right we think HCA’s stock price could get into the $70s in the next year or so.

HOLX – The title of our note reviewing Hologic’s earnings report was “Credibility Counts.” Predictability counts too and we did a good job of seeing the upside in numbers but most importantly the upside in Breast Health that came from having the best 3D mammography placement quarter yet.

There is still a lot of research ahead of us with HOLX. The most critical is to figure out what radiologists will be paid in 2015 to run a 3D mammography. Right now, there isn’t any incremental payment, which has been a headwind to system sales. SO far HOLX has converted 6% of the facilities in the US, but with an extra payment to cover the cost of the equipment, we should see adoption accelerate meaningfully.

What you might not know is how the government indirectly sets prices for medical procedures like 3D mammography and how unbelievably obscure and political the whole process is. The price setting process is deeply political between advocacy groups and manufacturers on one side, and academics and CMS (the government) on the other.

Advocacy groups want a high price to drive adoption and access and the manufacturers want to sell product, while the academics think there is too much screening, or the wrong kind of screening, and CMS has spending restrictions. The lower the reimbursement, the less equipment gets sold, and CMS spends less both in the near term and longer term.

While there is indeed a process to define a price, the result can be manipulated easily. There is no formula. guess that’s why we have yet to find anyone with a firm answer to our question or guidance on how we can get an answer on our own. Whatever CMS sets the price for 3D mammography will be the baseline price for every other insurance company to set their price.

LM – The intermediate term revamping of Legg Mason continued this week with an inline quarter for the period ending March 30th which closed out the firm’s fiscal 2014 period. We are not judging the merits of our recommendation of LM shares on short term quarterly numbers as we believe the value in LM stock is the ongoing turn around after a long period of underperformance. When zooming out from a multi-year view, the LM story is clearly improving which will unwind this long standing negativity now that the firm’s important fixed income business (which is 52% of assets under management and 37% of revenues) is on firmer footing. Legg booked a fixed income inflow in its annual period ending this quarter, the first inflow in over 5 years, which is proof that the firm is on the road to starting to rebuild its asset base. With the run in equities starting to stall out and institutional pension funds starting to increase their bond exposure, we view Legg as a defensive investment in the current well valued stock market.

LO – Lorillard was up a monster +8.5% on the week (vs +1.7% average for MO, PM, RAI), fueled by rumors throughout much of the week that RAI is interested in acquiring LO. Despite the rumor helping our Best Idea Long Call, we think a hypothetical deal (especially an imminent one) is challenged:

- Our main flag is that a combined RAI + LO would own ~ 67% of U.S. menthol market, which we believe should trigger anti-trust flags.

- Big tobacco is already a highly concentrated industry in the U.S. across the big three – MO has a leading ~51% of market share; a combined RAI + LO would equate to ~ 42% share.

RAI could look to divest such menthol brands as Kool, Winston and Salem, which could serve to change the consideration of the FTC/DOJ, however that’s far from a given. Additionally, we think the recent announcement that Susan Cameron will replace Daan Delen on May 1 could also be fueling speculation that she wants to come out of the box “strong” – which is drumming up rumors about this deal.

We maintain our bullish stance on LO supported by 1.) Its leading share and profitability of its core menthol business, 2.) Our belief in the limited menthol regulatory risk over the longer term (substantiated by a Washington, D.C. tobacco expert), and 3.) The upside growth in its blu e-cigarette business that commands leading share in the U.S.

As part of the Best Idea’s thesis we have not factored in a RAI + LO deal, nor has there’s been any comment from either LO or RAI to suggest this is more than just a rumor.

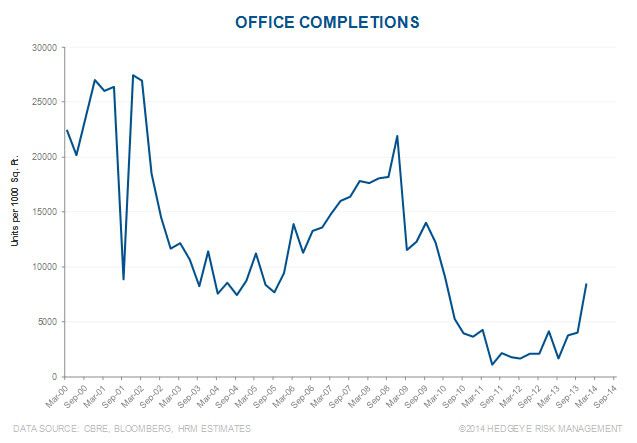

OC – The office market is beginning to show an increase in activity. Office completions in the second graph below displayed a sharp uptick for Q4 2013. Furthermore, heavy construction and machinery companies noted an increase in construction activity in Q1 earning calls. Caterpillar’s Construction Industries segment had sales over 17% Year-over-Year. Crane and aerial work platform companies Manitowoc and Terex noted pickups in their book-to-bill ratio – a positive sign as these booking and sales pass through to companies like Owens Corning.

RH – Last fall Restoration Hardware made the decision to cut its fall Source Book. We’ve discussed the potential implications of this strategy ad nauseum, but the numbers speak for themselves. The company realized an estimated $38mm in cost savings related to this shift in strategy in FY2013, and realized revenue growth of 32% in the 2nd half of the year.

The one drawback in this new strategy, as it relates to 2014, is the timing of the new product assortment release across the company’s three main channels – stores, dot.com, and Source Book. 1Q is almost closed and the company is up against a 41% comp in the first quarter of last year with no newness to help drive the comp. Revenue estimates are conservative for the quarter as a result growth is heavily weighted towards the back half of the year to coincide with RH’s 2014 new product launch. Which makes sense to us. We’ve gotten glimpses of the company’s assortment in categories like Outdoor, Baby&Child, as well as Rugs, but the full breadth of the assortment has yet to be released. That changes next week when the 2014 Source Books start arriving in homes which coincides with the launch of the full line up on the company’s website and stores (the stuff that will actually fit). For the full year we are modeling revenue growth of 25% compared to the Street at 20%.

ZQK – This week Quiksilver CEO Any Mooney had an appearance on a major financial network. CEOs appear on TV all the time. But there were two things that stand out to us. 1) Mooney is solitary and reclusive. He never struts his stuff on TV. This was highly unusual for him to do. 2) His appearance was on the last day of the quarter. His tone was upbeat, and consistent with our positive view on the stock. If it turns out that business trends are not positive, we cannot imagine that he would have delivered that message on the last day of the quarter. That would otherwise be a major liability – one that we think he’s smart enough to avoid.

* * * * * * *

Click on each title below to unlock the institutional content.

Why We Think Target Is a Short

Retail Sector Head Brian McGough explains why Target has more to worry about than just the data breach.

Panera Bread: Much Noise, Little Clarity

Managing Director Howard Penney breaks down his reasons for keeping Panera on the Hedgeye Best Ideas list as a SHORT.

ICI Fund Flow Survey: Below Average for Stocks, Better Than Average for Bonds

Financials analyst Jonathan Casteleyn takes a granular look at the most recent data which showed a rebound in both equity and fixed income flows, albeit to just running year-to-date averages.